Kim retweetledi

UNITED STATES AND IRAN EXCHANGED FIRE IN THE PERSIAN GULF, WITH DRONES, MISSILES, AND NAVAL CLASHES SHAKING A FRAGILE FOUR-WEEK CEASEFIRE AND ESCALATING TENSIONS ACROSS THE REGION.

English

Kim

26.4K posts

@kimster_76

The world is not prepared for the truth.

Warren Buffett’s Berkshire Hathaway's cash balance just hit $397 billion. Buffett has now been a net seller of stocks for 14 consecutive quarters. He is not finding things worth buying. That is the message. From 1991 to 2020, Berkshire's cash pile grew slowly — a few billion here, a few billion there, building to roughly $130 billion by the time COVID hit. Then something changed. Over the past five years, the balance has gone from $130B to $397B. The acceleration is not a function of earnings. It is a function of selling. Berkshire has been a net seller of equities for 14 straight quarters — including a net $8.1 billion sold last quarter alone. Apple. Bank of America. Quarter after quarter, the portfolio shrinks and the cash pile grows. The conventional read is that Buffett is being cautious. The more precise read is that he cannot find a single acquisition or investment large enough, cheap enough, and safe enough to justify deploying $397 billion. A $10 billion deal barely moves the needle. A $50 billion acquisition — which would be one of the largest in corporate history — would still leave him with $347 billion in cash. Put alongside Paul Tudor Jones's comments this week on market valuations at 252% of GDP, Buffett's cash accumulation is the same signal expressed differently. The two most credible long term capital allocators alive are both saying the same thing—the market is not offering value at current prices. One is saying it in interviews. The other is saying it with $397 billion sitting in T-bills. When the most patient buyer in the history of capital markets cannot find anything worth buying, that is worth sitting with…

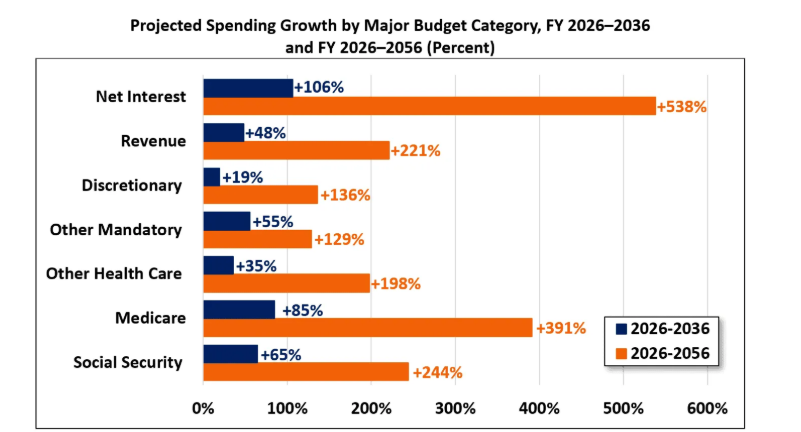

Correct. With one supremely important caveat: one of the parties must stop the hyperinflation that is coming.

Correct. With one supremely important caveat: one of the parties must stop the hyperinflation that is coming.