Sabitlenmiş Tweet

As I’ve said before, go back three years and look at who the big ADF traders were, especially the ones active on X. Almost all of them are gone. Sure, some may have just stopped posting, but in this game, when traders are doing well, they usually make sure everyone knows it.

The small cap game has shifted. It used to be about holding and building a position with size, riding moves into the close or even swinging. Now it’s more about hyper scalping 2–5% moves, over and over again. If your brain is wired for that style, you can still make a living, but that high win rate, martingale-type approach comes with a catch: eventually, a fat-tail loss can wipe out months of gains.

I’ve personally stepped away for now, closed my accounts and moved into Treasuries. I’ll come back if real EV returns to small caps, but with the rise of 24-hour trading and more widespread, AI-driven “China-style” manipulation, I don’t see that environment coming back anytime soon. What used to be a game where the top 95% could carve out a living now feels like it requires being in the top 99.999%.

At some point, traders need to take an honest look in the mirror. Too many stay in this game longer than they should…and yes, a lot of that comes down to gambling addiction. If you think that doesn’t apply to you, it’s worth questioning that assumption.

Life is short. You had a life before trading, and you’ll have one after it too. Think about the time, energy, and mental bandwidth spent trying to grind out an edge. That same effort could go into building something tangible, or investing in relationships and experiences that actually give something back.

small_caps_automated@SmallCapSmarts

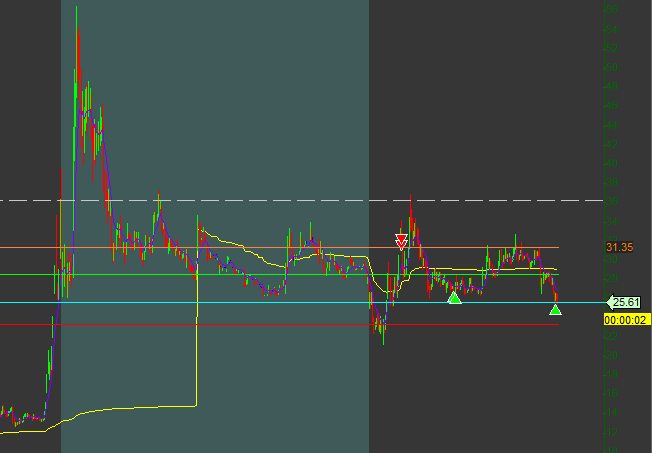

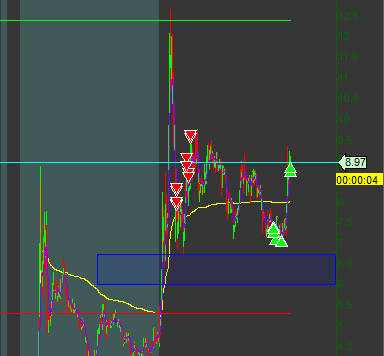

A very shitty week in small caps for me. Thankfully, I’ve cut size so much that I’m still up a decent amount YTD. What’s most concerning is that the broader market was weak, and that’s usually when I do well. Clearly there are other factors at play now. I have a theory. On top of the usual Chinese and domestic riggers, we’re also seeing a real scalping renaissance. Some htb brokers seem to have figured out that by offering near-zero commissions to hyperactive traders, they can still make plenty overall without relying on PFOF. Now every dip gets bought by both short scalpers covering and long scalpers chasing. Nothing fades anymore.

English