Sabitlenmiş Tweet

Marco

148 posts

Marco retweetledi

Marco retweetledi

@MaiusPartners It's an open question. The disciplined investor obviously presumes all HK AUM will be lost over time. That appears to leave investors with a Singaporean and Oceanian broker worth quite a lot more than 800musd.

English

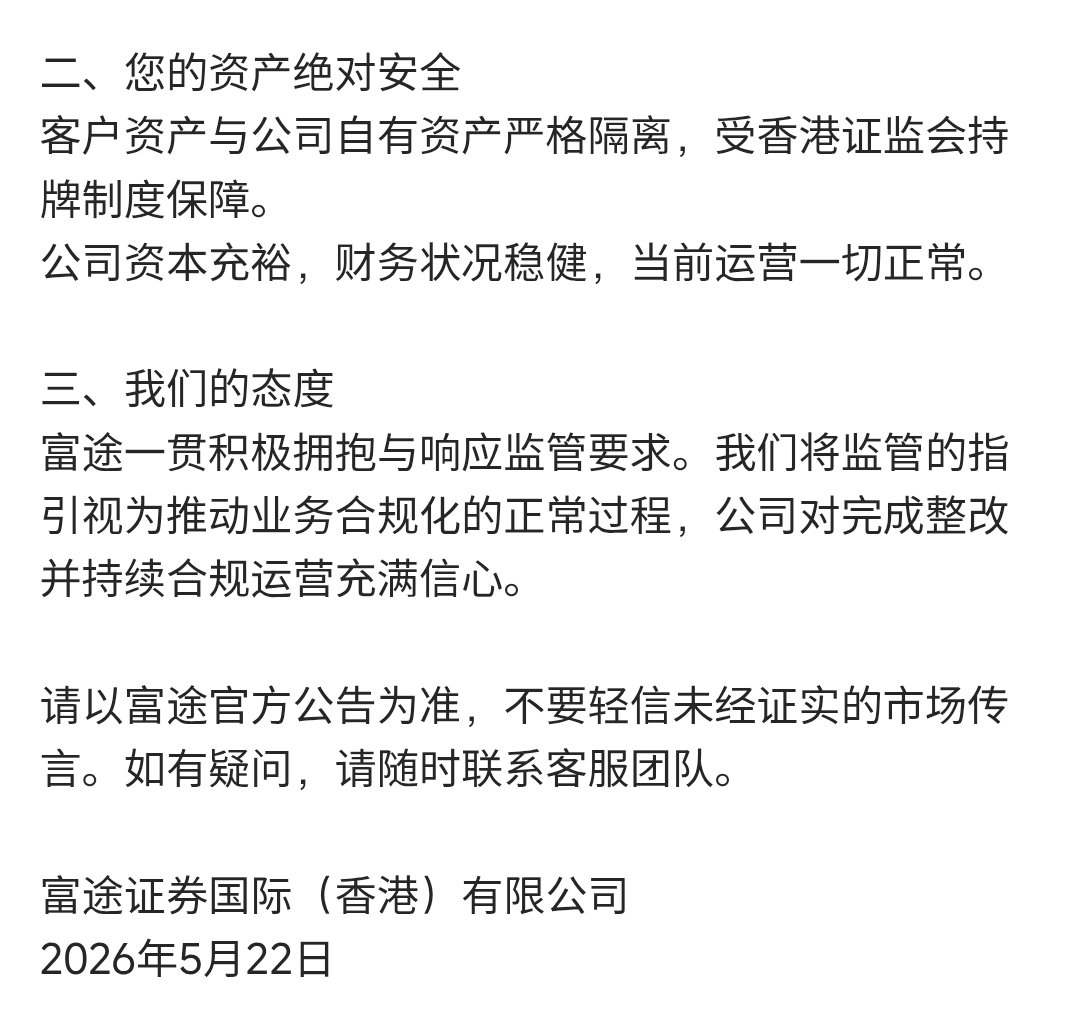

$TIGR giving off very scary vibes if for a remote second management believes CSRC rules are not applicable in Hong Kong.🤯

李老师不是你老师@whyyoutouzhele

针对中国证监会宣布罚没三家券商境内外非法所得 老虎证券选择硬刚 老虎证券COO表示,中国证监会的相关通知,不适用于香港实体。

English

Cannot agree more! And a 57M fine is nothing given how strong the balance sheet is, if China applied the law purely it could have been 500M-1B easily since it's a multiple on gross profit of all historical revenues from China.

But I'd also assume the same loud and uninformed herd to lead to some withdrawals, since the headline sounds concerning despite no impact on the business.

English

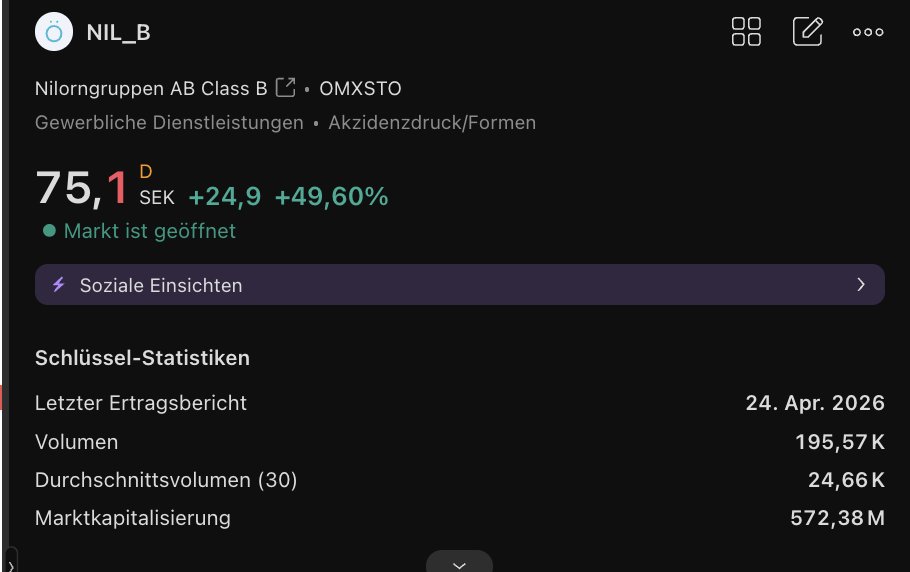

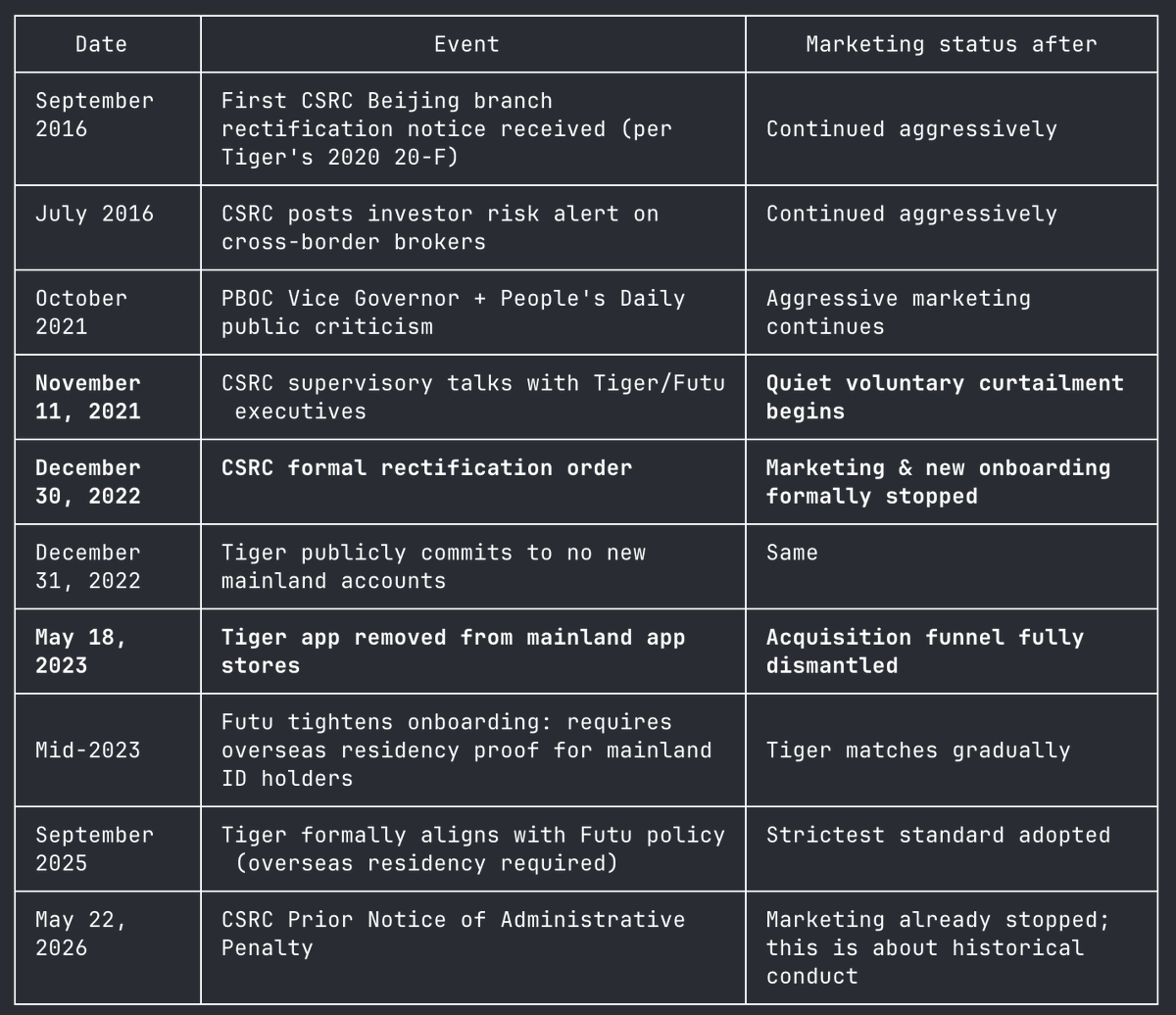

Älskar att alla pratar om kina-risken i $TIGR lagom till den gick ner med >50%. 2022 fick de sluta acceptera nya kunder från mainland, nu ska resten bort till 2028. 10% av kunderna kommer vara borta om 2 år. Böter var typ 1-1,5 kvartalsvinst. Kurs ner 37% som värst på det..

Svenska

Not involved in the stock, but at this point given the movement, you either double down or cut your loss depending on conviction. Pretty easy thought experiment to test one’s conviction: “Would you move your account to TIGR tomorrow knowing everything you know today”, and you have the answer on what the next trade is.

English

@alexeliasson I couldn't believe when I saw it, 300MM is a steal given how harsh the law is stipulated

English

Futu $FUTU got slapped with a fine equal to 20% of its annual net profits today. On top of that, its mainland client base will be wound down over the next two years.

I *might* be a buyer again at some point. I'll let all the details play out first.

English

Yeah also see it that way, but before 2022 $TIGR was a fully PRC company breaking a local law and with active marketing efforts - I'd assume the court will target all revenues arising from these customers.

Post 2022, there's been evidence that PRC nationals forged documents / didn't have the right substance abroad, but I feel this is harder for courts to prove the wrongdoing of TIGR :/

English

@marcotomasrodr @Zac_Pundi @Mystezi @NStepmum @GlobalStockPick @grok Right, but if a Mainland Chinese opens a brokerage account overseas, it’s not exactly their fault is it? Marketing on the mainland is another matter obviously

English

@Zac_Pundi @Mystezi @NStepmum @GlobalStockPick @grok Why can't TIGR / FUTU completely extricate themselves from Mainland China? Their business can be completely overseas. What leverage does the PRC gov have?

English

@MikeFritzell @Zac_Pundi @Mystezi @NStepmum @GlobalStockPick @grok Also this thread brings some interesting perspectives:

x.com/punk2898/statu…

Punk(2898 🙌💎)@punk2898

定格罚没 2992 亿人民币!可以说是第二个 Manus 了,还是那句话钱可以赚但是不能影响国家战略,目前国家战略很明显的好资产上港股、A股不能去美股 因为按照证券法,违法所得 ×(2 到 11 倍)(没收算1倍,罚款1~10倍)。所以定格处罚大概 2992 亿人民币,但是如果一倍大概 544 亿人民币 为什么说不会顶格处罚?🧐 一、理论上限 ≠ 能落地(警示作用) 富途市值约150–200亿美元(¥1100–1450亿)。10倍情景的¥2310亿直接超过市值——账面上是”判死刑”,现实中根本无从执行。 老虎同理,¥220亿(3倍)已超其市值。所以10倍、甚至3倍毛收入口径只是法条天花板,不是现实结果 二、境外主体执行难(逼急了跑路了) 被罚的核心是 Tiger(NZ)、富途(香港)、长桥(香港)——境外注册实体 证监会能开账面罚单、没收境内主体资产,但对境外实体的钱,实际收缴能力有限。“开出的罚单”和”收到的钱”会是两个数 所以最终大概在 200 亿左右 三、后续影响如何?利好的是币圈美股 1️⃣ Manus 只是开始,而且是国家战略不容置疑 2️⃣ 币圈的美股交易平台的天降福贵 3️⃣ 币安、OKX 这些交易所不知道是好消息还是坏消息,但是对 Hype 一定是好消息

English

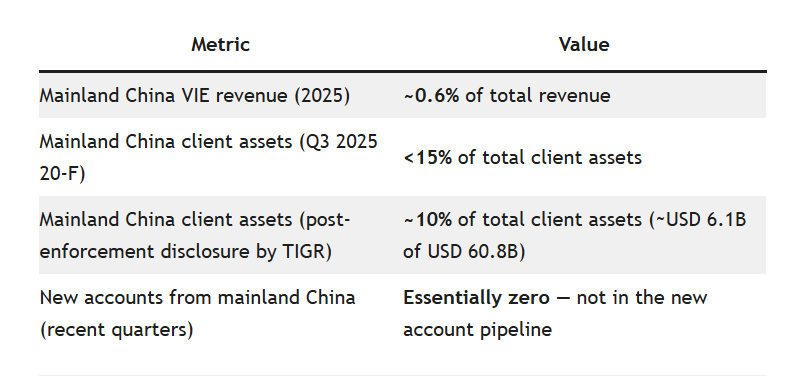

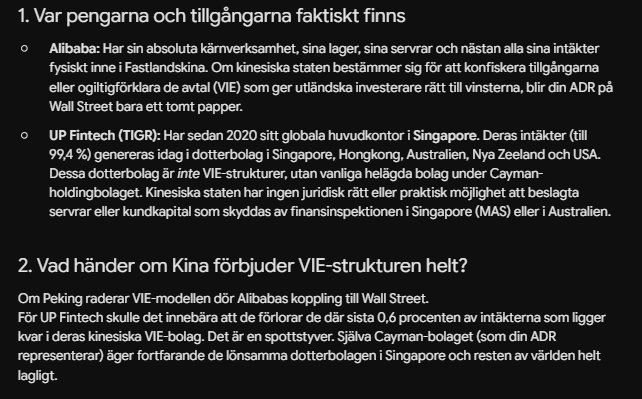

As of today, only 15% of assets are from Mainland Chinese, but the main issue here is the historical revenue. Before the 2022 crackdown and expansion to foreign markets, the majority of the revenue came from mainland Chinese who evaded the SAFE restrictions to acquire foreign assets (grey area at the time). On 2022, they complied with the regulation for new account openings but kept servicing the existent customer base, as that was apparently permitted at the time.

PRC law stipulates penalties that can reach 5-10x the gross revenue arising from these "illegal" activities (with previous cases usually falling at around 3x), even though TIGR is essentially a net-net as of today's price, this fine can reach or exceed the current cash and market cap, depending on the multiple they choose and what revenues they deem as illegal.

English

@MacroJason @imidaily Good points! Have you explored the Bulgarian market? Seems under-levered while rates are at ~3%.

I see lots of potential in cities like Varna, Plovdiv or Bansko despite the poor investment on infrastructure. Stable policies, lowest tax in EU, conservative/libertarian mindset.

English

Took a look - nice work! Some thoughts:

1. A lot of DM (developed market) investors fall into the trap of viewing real estate as one single asset class. They treat what they read about real estate in Western media / youtube as applicable to EMs. But there isn't a single real estate market - there are hundreds of real estate markets globally.

2. Related to above, many DM investors are obsessed with mortgages. They pass on solid EMs for the simple reason that mortgages are not offered. Failing to appreciate the benefits of owning in less leveraged markets 👉 grok.com/share/c2hhcmQt…

Many of those cash markets have outperformed leveraged up markets over the past few years. A fun illustration is that you would have been better off buying in 2021 in pre-war Kiev than many Western European markets like London.

Leverage can also be obtained in ways alternative to mortgages, e.g. by buying off-plan in cash markets 👉 x.com/MacroJason/sta…

3. It's incredibly hard to have an holistic view of global real estate markets across continents, as there are so many constantly moving parts (evolving local dynamics). Look forward to seeing FLIIP City Index develop - IMO the guys at @GlobalPropGuide also do a solid job 🫡

English

Most property investors don't buy where the best opportunity is.

They invest where their attention happens to be.

Where they live.

Where they have family.

Where they speak the language.

Where a broker is currently pitching them.

That is understandable, but it is also severely limiting.

If you could buy property in any city in the world, how would you know where to start?

For all you know, the best long-term opportunity might not be Lisbon, Dubai, Miami, Madrid, or London.

It might be some city you have barely thought about.

A city with low prices, decent yields, improving demographics, strong property rights, favorable tax treatment, manageable supply, good connectivity, and a currency that is not quietly murdering your returns.

So I have started building something I wish had existed when I started building my global real estate portfolio:

A data-based index of real estate markets in cities around the world, from the perspective of foreign investors.

I call it the Fundamentals for Long-term International Investment Property City Index.

Or, simply:

The FLIIP City Index.

The goal is simple:

To rank cities around the world

Not based on vibes.

Not based on which markets are fashionable.

Not based on where your cousin bought in 2017.

But based on cold, comparable, measurable fundamentals.

The current version looks at 41 metrics across seven categories:

1. Real estate fundamentals

2. Costs and taxes

3. Demand

4. Access

5. Governance

6. Macro conditions

7. Resilience

This is still a work in progress, and I want smart people to tear it apart so I can fix it.

Especially friends who have a lot of experience buying property across borders, like @MacroJason, @wander_investor, @TimurNegru, and @jeremysavory.

Try it out via the link in the first comment.

What am I missing?

Which scores seem off?

Which metrics are unnecessary?

Which ones are double-counting the same underlying thing?

Once we nail the methodology, I’ll add more cities, so tell me which cities you’d most like me to add.

English

It's interesting to see not only how detached the valuation is from the fundamentals, but also from the perception of the geopolitical environment.

At the time it was oversold due to the tariffs / delisting risk(?), now the US-China relationships seem better than even before Trump took office, but it seems that now nobody cares much.

English

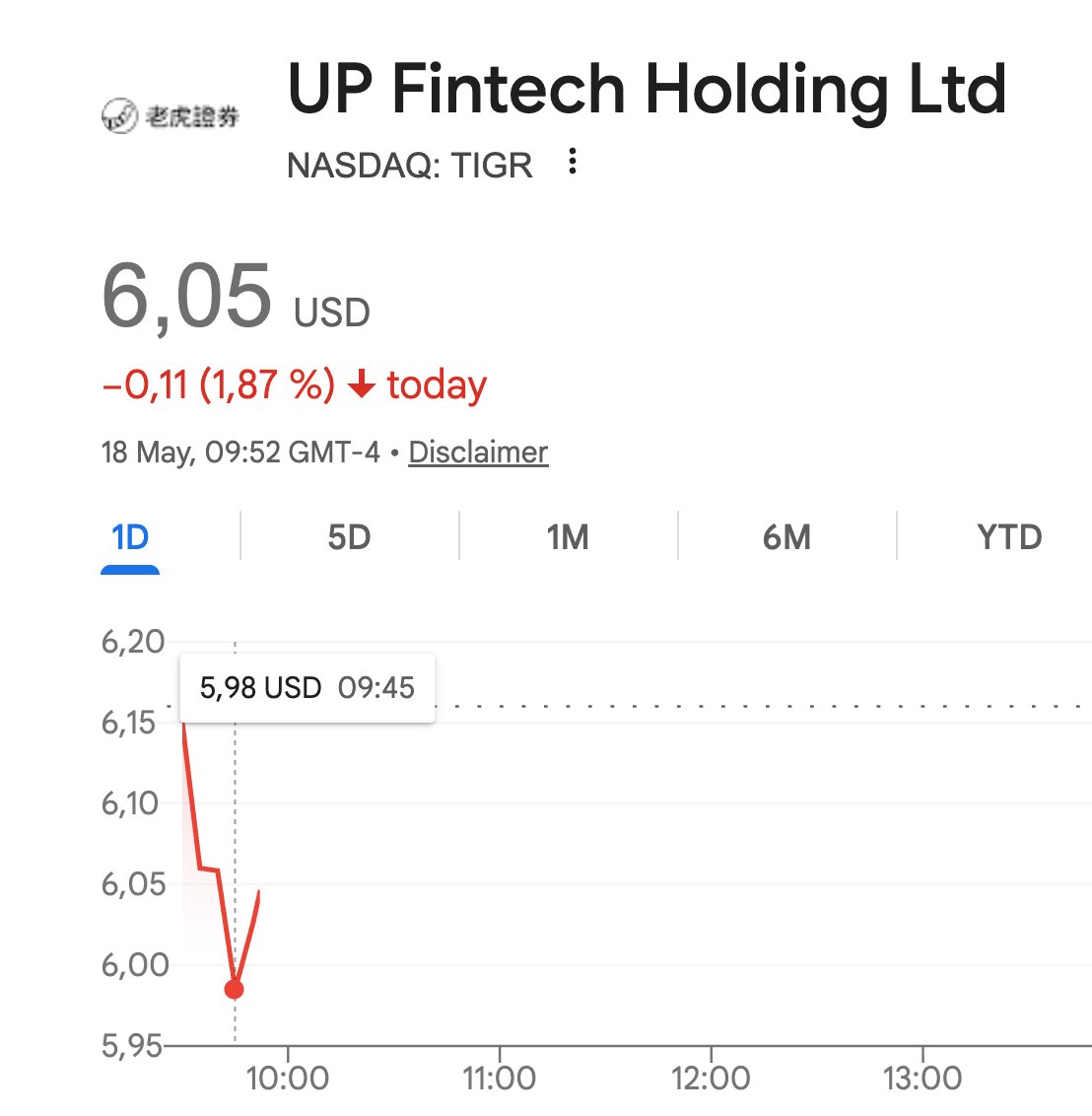

UP Fintech $TIGR dipped below $6 today. To me, this is the most mispriced stock in my investable universe right now and I cover it in a wide range of different write-ups.

Stock price is completely detached from fundamentals in my view, and while I do not know when the two will converge again, they will eventually.

English

@ResGloStocks @MomentumFinanc3 @xiep1987 Interesante pitch! Tendrías el link actualizado para Tianli? Muchas gracias de antemano!

Español

One of the repercussions brought by the China Nonferrous video in @MomentumFinanc3 was the contact with the Twitter user @xiep1987

He told us about his investment in Tianli Education $1773.hk

We initiated thread and coverage, but this time, with a PDF.

drive.google.com/file/d/17DukTV…

English

@ReneSellmann 2/2 $MEGP

x.com/marcotomasrodr…

Marco@marcotomasrodr

$MEGP operates vending machines in Europe, it has 2 segments: 50% Photo.ME (somewhat legacy segment, mainly passport pictures, stable), 50%-ish Wash.ME (laundromats, very strong growth +17% this year). It's a wonderful business, with the moat being the site contracts and field service network, upwards 32% ROIC, 6% dividend yield, 3% repurchases for 2026. Listed since 1962. Family owner-operators (36.5%). EV/EBI 8. Discount reasons: 1) Germany changed the regulation for passport pictures requiring in-office / certified pictures 2) The company considered going private but didn't get a good offer 3) A major shareholder did a private placement at a bit of a discount 4) The auditor once got delayed for reasons external to the company, but the stock got halted for a few weeks.

Let’s generate ideas to research further!

Pitch your favorite investment idea (in 3 sentences or less) 👇🏻

English

$MEGP operates vending machines in Europe, it has 2 segments: 50% Photo.ME (somewhat legacy segment, mainly passport pictures, stable), 50%-ish Wash.ME (laundromats, very strong growth +17% this year). It's a wonderful business, with the moat being the site contracts and field service network, upwards 32% ROIC, 6% dividend yield, 3% repurchases for 2026. Listed since 1962. Family owner-operators (36.5%). EV/EBI 8.

Discount reasons: 1) Germany changed the regulation for passport pictures requiring in-office / certified pictures 2) The company considered going private but didn't get a good offer 3) A major shareholder did a private placement at a bit of a discount 4) The auditor once got delayed for reasons external to the company, but the stock got halted for a few weeks.

English

@ReneSellmann Thank you! Just FYI, everything I buy ends up going down even more so please be careful with my pitches haha

Will add another for $MEGP, I also really like $KSPI and $HSBK but I know so far you didn't like EM so much.

English