Memento vivere retweetledi

Memento vivere

129 posts

Memento vivere retweetledi

5 Euros

Ha tardado 2 semanas en llegar pero mer de la pena 100% os dejo el

Tutorial de cómo la pille abajo.

Camisetas de futbol@CyCPicks

La web que vamos a usar se llama OopBuy, m.oopbuy.com/pages/register… Tenéis un 15% de descuento en el primer envío por registraros con este link.

Español

A ver si Alejandro Estebaranz entra en $POOL y la puedo comprar más barata aún ☺️

Español

Memento vivere retweetledi

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

English

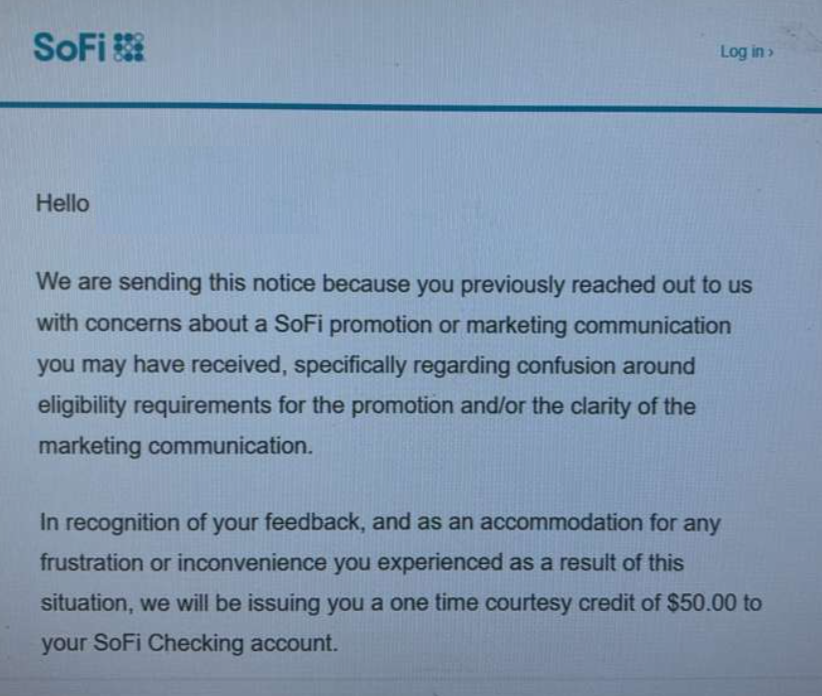

$SOFI is building a trusted brand.

Get your money right. Spend less than you make, invest the rest.

Finally a financial institution where you don't get shafted again and again with disgusting fees.

I like my @SoFi

4.5% APY up to $20k then 3.3%

1% recurrent invest match

2.2% cash back credit card

5% grocery smart card???

English

Memento vivere retweetledi

esse é o anúncio de gravidez mais da hora de todos os tempos

Português

Memento vivere retweetledi

Un amigo lleva más de 10 años pintando casas por toda Sevilla.

Es de esos que llegan pronto, dejan todo limpio y cobran lo justo. Nunca te da un presupuesto inflado. Ahora mismo necesita trabajo y chapuces. Lo que sea: habitaciones, pisos...

¿Alguien le puede echar una mano? RT

Español

Memento vivere retweetledi

If you won $10,000 today, which stock are you putting it all into?

English

¿Que compañía creéis que es la mejor para no perder dinero de aquí a 10 años?

Español

🚨 @Hut8Corp just dropped its biggest announcement of 2026 — Beacon Point is a monster deal 🚨

⚡ 15-year, $9.8B triple-net lease at Beacon Point — 352 MW IT capacity with high-investment-grade tenant — $25.1B if all renewal options exercised

⚡ Expected average annual NOI: $655M upon stabilization — cumulative $9.8B over base lease term

⚡ Total contracted capacity now 597 MW across River Bend + Beacon Point — aggregate base-term contract value of $16.8B — aggregate annual NOI of ~$1.1B

⚡ Designed to NVIDIA DSX reference architecture for gigawatt-scale AI factories — 57% larger than original design within the same land and utility footprint

⚡ 1,000 MW of utility capacity secured with AEP Texas — initial energization Q1 2027, first data hall delivery Q3 2027

⚡ Tier 1 execution partners: @nvidia (technology), Jacobs (EPCM lead), @Vertiv (critical infrastructure systems)

⚡ 7,545 MW of additional pipeline under diligence, exclusivity and development — Beacon Point is just the start

CEO @ashergenoot "This demonstrates that our development model — which pairs power-first underwriting with disciplined commercialization and institutional execution — is repeatable and extendable across our broader pipeline"

River Bend. Now Beacon Point. $16.8B in contracted revenue. $1.1B average annual NOI. 7,545 MW still in the pipeline.

$HUT isn't building a data center company — it's building the institutional infrastructure platform of the AI era

Is $HUT the most undervalued AI infrastructure platform in the public markets right now? 👇

$HUT @ashergenoot #AIInfrastructure #DataCenter #DigitalInfrastructure #NVIDIA

English

MCNALLIE KNOWS $SLNH GONNA STRIKE A BIG DEAL SOON!!!

McNallie Money@McnallieM

🚨 @Hut8Corp just dropped its biggest announcement of 2026 — Beacon Point is a monster deal 🚨 ⚡ 15-year, $9.8B triple-net lease at Beacon Point — 352 MW IT capacity with high-investment-grade tenant — $25.1B if all renewal options exercised ⚡ Expected average annual NOI: $655M upon stabilization — cumulative $9.8B over base lease term ⚡ Total contracted capacity now 597 MW across River Bend + Beacon Point — aggregate base-term contract value of $16.8B — aggregate annual NOI of ~$1.1B ⚡ Designed to NVIDIA DSX reference architecture for gigawatt-scale AI factories — 57% larger than original design within the same land and utility footprint ⚡ 1,000 MW of utility capacity secured with AEP Texas — initial energization Q1 2027, first data hall delivery Q3 2027 ⚡ Tier 1 execution partners: @nvidia (technology), Jacobs (EPCM lead), @Vertiv (critical infrastructure systems) ⚡ 7,545 MW of additional pipeline under diligence, exclusivity and development — Beacon Point is just the start CEO @ashergenoot "This demonstrates that our development model — which pairs power-first underwriting with disciplined commercialization and institutional execution — is repeatable and extendable across our broader pipeline" River Bend. Now Beacon Point. $16.8B in contracted revenue. $1.1B average annual NOI. 7,545 MW still in the pipeline. $HUT isn't building a data center company — it's building the institutional infrastructure platform of the AI era Is $HUT the most undervalued AI infrastructure platform in the public markets right now? 👇 $HUT @ashergenoot #AIInfrastructure #DataCenter #DigitalInfrastructure #NVIDIA

English

Memento vivere retweetledi

I think I'm going to allocate 5% of my portfolio to a basket of $SPGI, $MCO, $V, $MA and $BR. All of them have slide into double digit irrs for me with pretty reasonable assumptions. Huge moats, unfairly being sold off in the AI losers basket atm. Offsets a lot of my shorts well.

English

Memento vivere retweetledi

Esto es espectacular.

Endrick da entrevista en francés casi perfecto llevando tan solo 4 meses en Francia.

Miren la cara de la intérprete, que también le da clases.

Orgullo total de su alumno. Un crack el Bobby Charltom brasileño.

Español

Sigo creyendo en los próximos años de $FRPH, pero he vendido 1/4 de mi posición. Prefiero invertir ese dinero en aumentar mi posición en $SPGI

Español