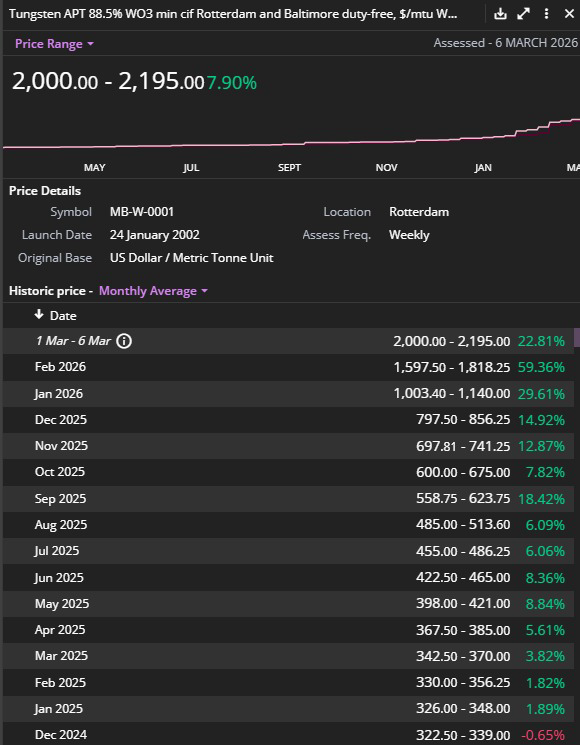

On the contrary on what I read here, there was never a #Tungsten deficit. China has consistently overproduced Tungsten for at least a decade. All these overproduction mainly stem from illegal mining. I’ve spent a good month or 2 on the entire supply chain and found that no numbers match, or even made any sense. They were substantially different. It’s safe to say that any modelling on Tungsten supply/demand is made redundant and doesn’t paint the full picture. Knowing how mining in #China operates, I quickly realised that it’s another textbook case – people playing the system according to the rules. My first-hand experience was actually #Vanadium back in 2017, where I watched the whole thing unfolded. Illegal mining was rampant across the country. The data I’ve gathered showed the overproduction gap had shrunk significantly over the past decade. As an average, I found the 30% gap slowly declined to less than 10%. The biggest gap closing was when Ministry of Natural Resources of China decided to revamp the Tungsten quota in early 2020s. It will only be a matter of time before the gap is closed entirely. In fact, on my previous post on the emerging market of Tungsten PCB drillbits, we’re no doubt going to see a global shortage of tungsten supplies in the coming years, or even in 2026. Lots of downstream that uses Tungsten are not being accounted for in any models. We’ve already seen a surge in Tungsten price, but I don’t think it’s not that irrational at all. If you look at the downstream of Tungsten, they’re either defense or high-tech industries, where they have low to 0 sensitivity to prices & they have the ability to absorb the flow-on costs. With that said, China has allowed the world to benefit immensely from the abundance of Tungsten supply. It came with a cost for China - Tungsten ore reserve dipped significantly since 2010s. I believe this is also the primary reason why they will place tougher restriction on limiting Tungsten production. The world felt it when China tightens their grip on Tungsten, and they've only exerted like 10% on what they could actually do. Price spiked, people who have done their studies were shocked to find out how China has such control over a metal that people rarely talk about, shortage narrative starting to appear all over investment communities. Tungsten has been readily available locally, and geopolitical situation was stable enough for China to not build any national strategic reserve for Tungsten. But as I said previously, it’s a reasonable scenario where China decides to build a strategic reserve. It seems to be trending towards that scenario as well – 13.5 days of inventory in December; no additional inventory for exports despite a surge in overseas RFQs ; pre-payments of all long-term(only 15 days) contracts ; fortnightly contract pricing adjustments etc etc. To finish off the post, I foresee 3 scenarios that may play out but none will help to alleviate the ongoing tightness of Tungsten supply. I’m ranking it on the perspective of of market supply – best= supply going back to equilibrium, worse = deficit. Best case – Quota to revert back to last year’s amount. This would add minimal supply to market. Neutral case – Quota to remains the same as last year. 0 additional supply in China. Worst case – A reform of how China MNR derives the production quota that will address & close most loopholes which permitted the existence of illegal mining. I cannot see how the future plays out, but I know this presents a window opportunity for investments into new Tungsten projects. If you’re either betting big on Tungsten or have got a quality project, I strongly suggest you do yourself a favour & fly to China to hear it straight from the horse’s mouth. See what I did there? It's the year of the horse 😉