mStable

2.2K posts

mStable

@mstable_

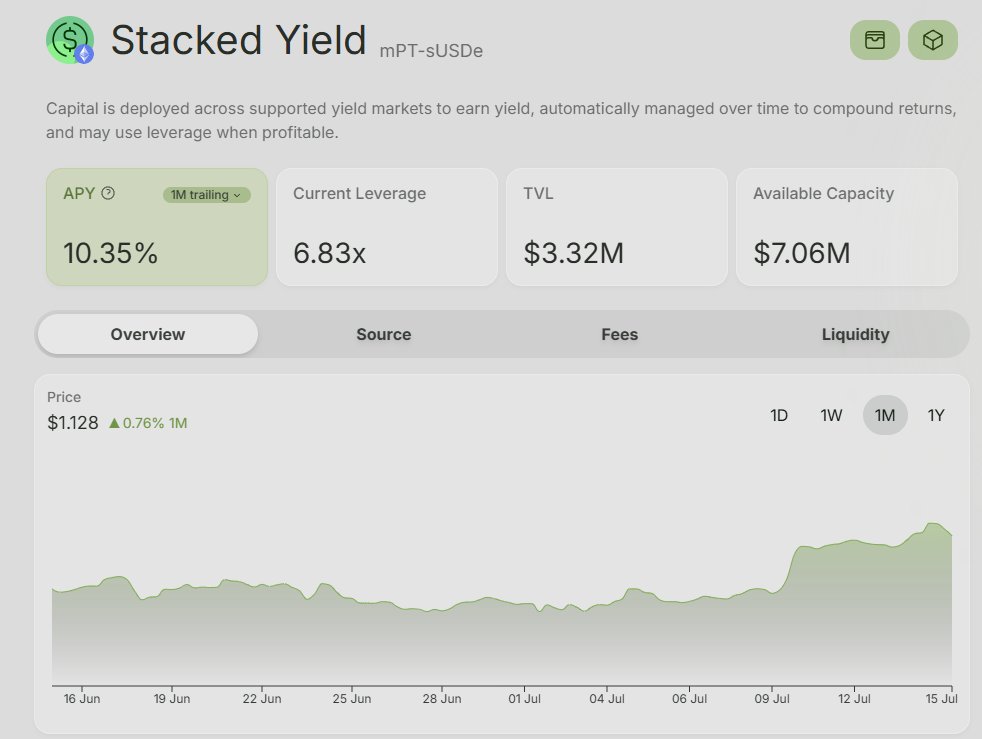

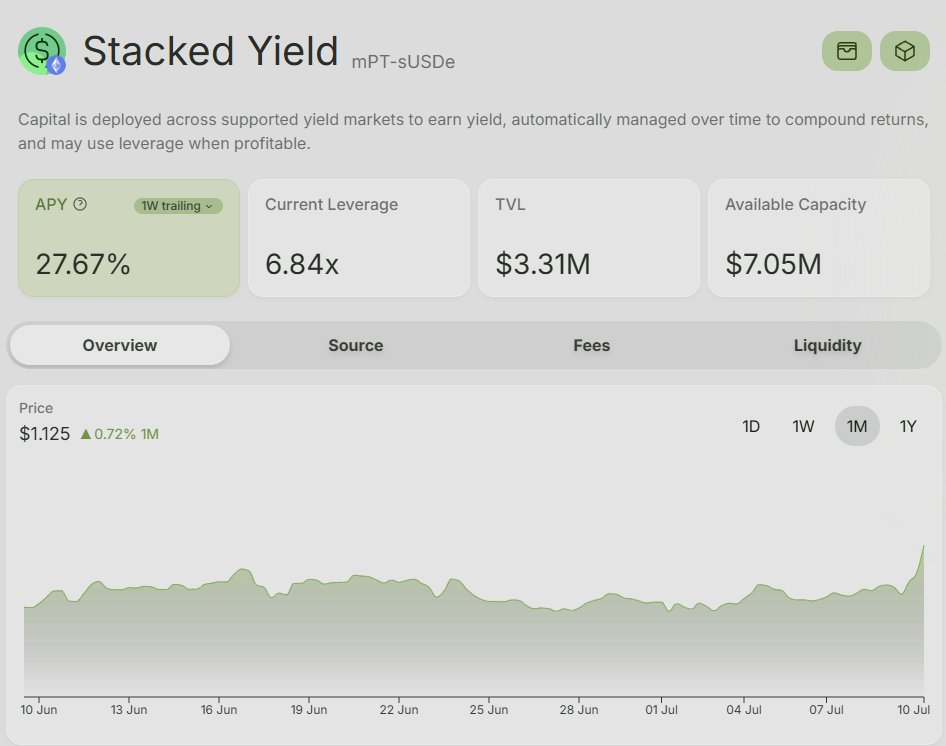

mStable efficiently stacks yield with Pendle

Here's what happened @ethena in June: • Partnered with @BlackRock with USDe now integrated into BlackRock Aladdin which houses $25t of AUM. • Partnered with @RobinhoodApp as the primary collateral in their new crypto earn product. • Partnered with @coinbase to grow onchain finance and savings products. • Coinbase Ventures made its first open-market investment into Ethena. • The USDe vault on Coinbase grew to nearly 200m in a few weeks. • @stablecoin_x began trading on Nasdaq Global Market under the ticker "USDE", giving public-market investors direct access to the Ethena ecosystem. • Published our plan for the next phase of USDe backing diversification, broadening real-world asset exposure beyond tokenized T-Bills. • Partnered with JanusHenderson to allocate and support distribution of their tokenized, high-quality liquid CLO funds. • Integrated JAAA, Janus Henderson's AAA CLO strategy, into USDe's backing through a partnership with @Centrifuge. • Integrated STAC, the Securitize Tokenized AAA CLO Fund, into USDe's backing through a partnership with @Securitize. • Expanded our partnership with @Anchorage to advance institutional investment lending. • @MercadoBitcoin, Brazil's largest exchange, listed USDe. • Became a founding member of the @Avax Payments Collective. • @kamino went live with Sentora's PYUSD/USDe vault.

Introducing Open USD: a stablecoin built for the internet economy, designed by the businesses growing it. joinopenstandard.com/blog/introduci…

Announcing Ethlabs: a non-profit R&D lab for Ethereum and ETH Our mission is to make Ethereum the settlement layer of the global economy. The internet became global because shared protocols created a common language between networks. Private systems remained useful, but bounded. Finance is approaching a similar moment. As value, assets, and markets become digital, the world needs shared settlement infrastructure. Ethereum is uniquely positioned to become that shared base layer, the neutral foundation on which users, institutions, and agents can transact without intermediation. What we believe: • We believe credible neutrality matters. Ten years of uptime and the lowest counterparty risk. Ground that cannot be pulled away by any one country, institution, company, or person. • We believe ETH matters. The most valuable, programmable store of value. A decade of broad distribution, deep liquidity in onchain markets, and maximally trustless asset on Ethereum. • We believe DeFi matters. Markets, liquidity, credit, exchange, and coordination, open to anyone. • We believe adoption matters. Principles do not change the world until people benefit from them. We sit between two worlds: real usage from the builders at the frontier, and the protocol that has to support it. We work with users, applications, wallets, L2s, infrastructure teams, institutions, ETH holders, core devs and researchers, then turn what they actually need into protocol work, shared standards, infrastructure, and shipped products. Ethlabs is independent but Ethereum is a shared project. We are one node in a much larger network of stewards. This is the multi-node future. We have spent the better part of the past decade contributing to Ethereum core research and development. We are opinionated and transparent. We move with urgency, learn in public, and course-correct when we’re wrong. We are building a lean, talent-dense team for people who want to do the most important work of their careers: join@ethlabs.org

JUST IN: Bitcoin is now down 32% this year. $ETH is down 45% this year