Sabitlenmiş Tweet

ML

468 posts

ML

@mtslau

Founder @Arttaca and Gravity Capital. In it to win it.

Cyberspace Katılım Temmuz 2009

130 Takip Edilen101 Takipçiler

No no no, let the SaaS-pocalypse continue for another 6-12 months. I haven't build up a position yet. $FIG

ML@mtslau

Planning to sell some puts on $FIG to get some cash while I slowly observe and add to my position. I am open to being wrong on Figma. Their numbers will be very important in keeping my interest in the company.

English

It looks like $IREN is getting ready to go higher soon. If not, I am also not very worried. The company is in a good place.

ML@mtslau

Great show of strength for the last 2 days. We now have a local higher high. Feels like we will stay above and turn resistance into support this time. Earnings tomorrow, let's see how it plays out. I'm not in a rush. Bullish. $IREN x.com/i/status/20489…

English

@DKThomp oh, so you think this is a coherent ideology?

P.S. we had DOJ, not FTC. and Jonathan Kanter didn't even block it, just delayed for 16 months while he outsourced "justice" to the UK / Europe.

English

When Lina Khan blocked the Figma-Adobe merger, and Figma later IPO'd‚—making lots of people very rich and even minting a few billionaires in the process—the left praised Khan's policies for creating all that value. Khan herself called it "a win" for investors.

But now we're also hearing that wealth is inherently unethical and extractive.

So, I guess I'm confused.

Is it inherently evil to create billions of dollars of value as part of an enterprise in which you retain equity ownership? Or is it ... sometimes good? Or is it mostly only good when it's downstream of anti-monopoly measures?

English

No software, no sales team. Such visionary leadership $iren

Berlinergy@Berlinergy

$IREN Dan Roberts today: „you don’t need a sales team in this market .. particularly when you’ve got Nvidia..” 🔥

English

@AlbertBundy33 Can go below 60, but that's just people trading the stock and not looking into the mid-long time frames. Can read Jim's post if you're worried.

x.com/i/status/20525…

Jim Liu@jiahanjimliu

$IREN: First look at Q3 FY 2026 Earnings Quick note - why is IREN giving back all it's gains from $72 -> $60? 1. CRWV had bad cost numbers and whole Neocloud sector is following it's 10% dump. 2. Reason I explain in takeaway 3. Takeaway 1 - Nvidia Contract Economics Nvidia 3.4B/5-year 60MW GPU compute contract with IREN for internal research usage. - This is at 11.3m/MW which is 16% increase from 9.7m/MW MSFT contract. This is very meaningful top line increase given this is for air-cooled which means B300s. Much more profitable than MSFT contract and the topline IREN needs. Takeaway 2 - Why is IREN Expanding Slower than Expected Each GPU generation has greatly improve performance and economics. IREN has a "good" bias from the bitcoin mining days where it was a late move in order to have a fleet that was heavily skewed towards newer ASICs. Technology moves very very fast in the beginning and AI GPUs are still considered early, IREN is trying to time where most of it's fleet is mid-stage GPU aka Vera Rubin or newer. Hence it's SW1 buildout is pushed out to 2027 so that it will be all Vera Rubins. Yes, IREN is still scaling out it's DC buildout teams as this is all external and not contracted out like CRWV/NBIS. CRWV/NBIS for 2026/2027 capacity relies on 3rd parties and NBIS greenfield sites starts 2028. This is why IREN is full funded already for 2026 based on operational cashflow, existing cash on hand and has the Nvidia investment coming in later while NBIS still has 2026 funding needs even after the large convertible and Nvidia investment. Less aggressive but also less capital intensive. CRWV/NBIS is your investment if you want to expand as fast as possible. IREN cares about unit economics and having a VR200 and newer generation fleet. IREN selects customer based on ability to get financing at best interest rate and has better rate on their convertibles than both NBIS's convertible and CRWV's corporate. Given corporate debt is apple or oranges but 9% on CRWV is meaningful enough to compare to IREN's 0% and 1.5% converibles and 6% GPU debt financing. Takeaway 3 - Nvidia Option to Invest Instead of Immediate Investment Market sees this the reason to sell $IREN back down from $72 -> $60. Whereas $CRWV and $NBIS got the money immeidately for shares at market price because they have 2026 unfunded needs, $IREN is fully funded for 2026 and would rather sell at above the market price. The way to negotiate this is to have the shares sold in the future at a premium at which the negotiations happen. Nvidia negotiations were happening today, they were happening when IREN was in the 40s so 70 is a significant premium. YtD relatively IREN at 70 is equivalent to $NBIS issuing shares to NVDA at 140. IREN does not need the 2.1B in 2026, why dilute at $40? IREN will need cash in 2027 where it's buildout is going to accelerate so IREN is it then. The important part is getting priority on Nvidia's delivery schedule. Nvidia does benefit by having the right to buy IREN stock through 2031 at $70 but everyone, everyone is paying alot to secure HBM which is on-chip with the GPU. This $70 call option for Nvidia is good for 600k GPUs. Full Points - 3.7B 2026 ARR runrate and 3.1B ARR already contracted. This means the Mackenzie GPUs are contracted! All the Prince George GPUs are contracted. - New site in not only EU but APAC! Australia confirmed. - 2.6B cash on hand. People can stop talking about the ATM for current liabilities out now. ATM is for future growth/deals/acquisitions. - Will provide 3.4B of AI Cloud compute to Nvidia. Not counted in the 3.7B ARR so likely 2027. IREN is selling GPU compute to Nvidia internal teams! - IREN secures 600k GPUs of Nvidia GPUs as part of partnership. Nvidia has right to buy $IREN at $70 as it delivers the GPUs to IREN, full $2.1B investment option upon delivery of 600k GPUs. - 480MW by 2026, 1.21GW by 2027, 5GW by 2030. Nvidia GPU secured, power long secured, deals will come. - H1 handoff in Q3 CY 2026 is kind of disappointing. Handoff will likely be early Q3 as burn-in already happening now. H2-4 will be handed off by this year is the important part. There must have been some snag in H1. - Rest of Childress will be split among 100MW IT of liquid cooled H5-6 (likely extension for MSFT) and 250MW retrofit of air-cooled capacity. - @FransBakker9812 spot on - First SW1 200MW IT will be in 2027 and be for VR. - AI Revenue 33.6m is lower than expected as commissioning GPUs slower than expected. Will expect this to speed up as IREN ramps up their in-house team.

English

Say what you like, but $NVDA effectively put a bottom at 70 for $IREN (provided they can execute). And we know they can.

𝐀𝐠𝐫𝐢𝐩𝐩𝐚 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭𝐬@Agrippa_Inv

$IREN just announced a massive 5 GW partnership with none other than $NVDA.... I love how it references $IREN's "global" pipeline. $IREN is fast fast-tracking its path to becoming the next hyperscaler. It turns out that having gigawatts of grid-connected energy, while everybody else is severely power-constrained, is a real MOAT. $IREN shareholders have just been validated BIG TIME. We are just getting started! 📈

English

How interesting. 🤙🤙

Dustin@DustinHuntwn

$IREN Dan is releasing earnings on his birthday. Enough said😆

English

Great show of strength for the last 2 days. We now have a local higher high. Feels like we will stay above and turn resistance into support this time. Earnings tomorrow, let's see how it plays out. I'm not in a rush. Bullish. $IREN

x.com/i/status/20489…

ML@mtslau

We're still fighting. Will we turn resistance into support this week? That's what these next 4 days are about. And I'm not getting all this $IREN v $NBIS spat. If one is delusional, so is the other... x.com/i/status/20474…

English

yeah... you can only say that if you're technically 100% illiterate. just no question. it's worse. lidar is better in sun, fog, rain, at night, longer distance, etc. the "humans don't have lasers" analogy is hella stupid. yes, humans are also not superhuman level safe... point is to make the best product and that is based on lidar.

English

This feels immensely satisfying.

When I made my first posts about $OUST on X, I remember some people told me cameras will replace Lidar and I'm an idiot for investing in this company.

Who's got the last laugh? 🤭

@ousterlidar

TechCrunch@TechCrunch

Ouster’s new color lidar is coming to replace cameras techcrunch.com/2026/05/04/ous…

English

Planning to sell some puts on $FIG to get some cash while I slowly observe and add to my position. I am open to being wrong on Figma. Their numbers will be very important in keeping my interest in the company.

ML@mtslau

Let go of $BZAI and put that little bit of cash into $FIG. Looking back, I should not have bought $BZAI for "fun". I did dig into what they do and there's really nothing I can find on how their edge computing can be applied IRL, but it's just a tiny position so it's ok.

English

@moninvestor @daniel_koss @ousterlidar If you're in the Musk/Tesla camp, then you just need a camera sensor and a camera lens.

English

@daniel_koss @ousterlidar I feel like OUST new Lidar sensors are going to become a necessity for physical AI.

English

We're still fighting. Will we turn resistance into support this week? That's what these next 4 days are about. And I'm not getting all this $IREN v $NBIS spat. If one is delusional, so is the other...

x.com/i/status/20474…

ML@mtslau

We finally broke up and in a spectacular way. Hopefully we keep it above 50 tomorrow and the next week. For me, the next level is 58. This feels particularly great on a day when everything is down. $IREN x.com/i/status/20446…

English

Let go of $BZAI and put that little bit of cash into $FIG. Looking back, I should not have bought $BZAI for "fun". I did dig into what they do and there's really nothing I can find on how their edge computing can be applied IRL, but it's just a tiny position so it's ok.

ML@mtslau

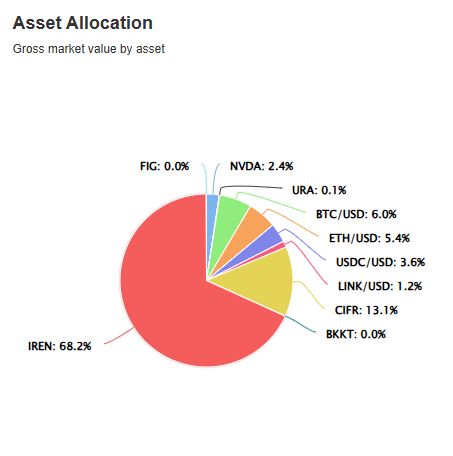

Haven't made any moves since the last update. We only sold $BTC in the 92-97k range and leave that in cash. I still don't have an idea on what to do with $ETH and $LINK. It's probably going to get uglier. BUT maybe BTC dominance will start falling, giving them a lift. 🤷🏻♂️

English

We stayed above 50, it's great! No war news this weekend and we can smoothly sail into May. $IREN

ML@mtslau

We finally broke up and in a spectacular way. Hopefully we keep it above 50 tomorrow and the next week. For me, the next level is 58. This feels particularly great on a day when everything is down. $IREN x.com/i/status/20446…

English