Mush614

838 posts

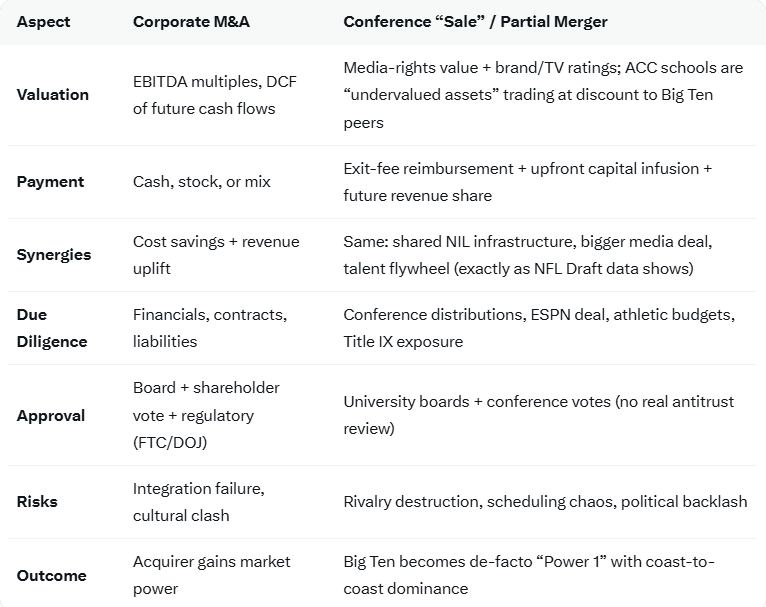

Should the Atlantic Coast Conference (ACC) consider selling themselves to the Big Ten? College athletics in 2026 is no longer an “amateur sport," it is a high-stakes, consolidating industry at the top end of D1 where the rules of corporate finance and M&A apply directly. In any consolidating industry, larger scale drives down per-unit costs. A 28-school Big Ten would spread fixed and semi-fixed expenses across far more members. Conferences function like businesses in any other industry. In the college athletics world of our economy, they compete for media revenue, talent, sponsors, and post-season championships. The data that was presented in the past couple of weeks from a board meeting of a school in the ACC indicated a schools budget being $250M+ FY2027 budget vs. stagnant ACC distributions of ~$44–45M today, projected to only reach $73M by 2036) plus the latest 2026 NFL Draft numbers (Big Ten + SEC = 60%+ of all picks, with the Big Ten surging to 68 total selections) show the classic “rich-get-richer” flywheel that precedes industry consolidation. 1. Economies of Scale - Massive Cost Efficiencies and Margin Expansion Media-rights leverage: One coast-to-coast footprint (California to Florida to New Jersey to the Midwest) creates a single, must-have inventory for networks. Current Big Ten deals already dwarf the ACC’s; a merged entity could renegotiate or extend at premium rates. NIL/revenue-share infrastructure: Shared compliance, scouting GM offices, transfer-portal analytics platforms, and athlete-compensation funds become dramatically cheaper per school. FSU is already spending Power-Two levels on football operations and revenue sharing; the ACC’s smaller pie forces every dollar to be squeezed from university subsidies instead of new revenue. Olympic/non-revenue sports: The Big Ten has a historic strength here. Adding ACC programs instantly deepens competition and Title IX compliance without the $4–5M annual cuts FSU trustees are already eyeing. Result: Operating margins improve, freeing cash for facilities, coaching, and recruiting instead of deficit spending. 2. Revenue Synergies - Immediate and Structural Uplift Classic M&A revenue synergy: ACC schools currently receive roughly $44–45M in conference distributions; Big Ten schools are already at $63M+. A partial merger would instantly move the 9 ACC schools into the $70M–$130M range projected for the Power Two by the mid-2030s. This is textbook horizontal integration: eliminate the “revenue gap” that is forcing FSU to run a $250M business on a $45M conference subsidy. 3. Market Power and Competitive Moat Brand valuation: ACC schools individual “enterprise value” (TV ratings, boosters, facilities) would accrete dramatically inside the Big Ten umbrella, just as USC/UCLA/Oregon/Washington saw their media payouts jump upon arrival. This is not “selling out” — it is applying standard M&A logic to an industry that is already consolidating whether the ACC likes it or not. The numbers FSU’s own AD presented to the Board of Trustees last week (spending like a Power-Two program while earning like a mid-major) are the exact warning sign that triggers a strategic review in any corporate boardroom. Consolidation is how lagging players become part of the winning conference. The alternative is slow bleed, continued subsidy pressure, and eventual irrelevance.

@Sanjit__T Did you talk about him at all before we picked him? I watch most your videos and this is the 1st time I hear about this guy. Most people are saying he’s the 5th or 6th S.

@Sanjit__T This is major reach ya goofball