No Coupon At All

228 posts

look either you are using color-coded flags like this kid I just met or you don’t care about your career:

English

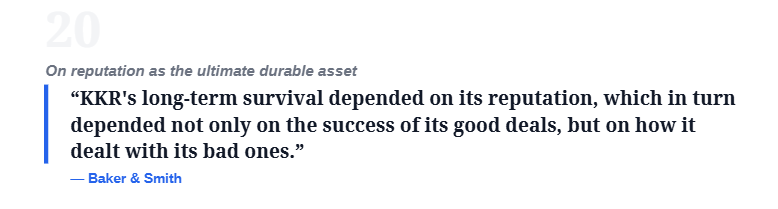

the reason why KKR survived 50 years in private equity:

The Icahnist@TheIcahnist

KKR Co-Founder on their early deals:

English

Here are a bunch of my thoughts on private equity. They won’t be popular. That’s fine.

I have been in investment banking or private equity for nearly 20 years, working with and for private equity firms. I’ve interviewed, met with, and interacted with hundreds of PE firms over the years. I’ve worked with good firms and bad firms, good people and bad people. I’ve seen what works and what doesn’t.

So that’s my background, but I’m still just one guy with incomplete information, biases, and all the other baggage that comes with being human. Take it with a grain of salt.

When I started in the space, private equity felt entrepreneurial. We called them “shops” (maybe that was just us?). They were hungry. They took risks. Success was not guaranteed.

I started my career excited about the prospect of joining, buying, fixing, growing, and selling companies. Since then the space has changed. That’s natural in any industry.

But PE has become commoditized. A systematic career ladder.

People don’t join PE because they love businesses or because they want to innovate. They join because it’s one of the safest, highest-paid tracks in America. If you make it into the system- the right schools, the right banks, the right funds, you’re set. Worst case, you fail and go do something else in finance. Best case, you become a Managing Director (MD) and make generational money.

That is not risk-taking. That’s joining a protected class.

The industry has been drifting. There are more firms than ever, more funds than ever, and more Patagonia vests being sold than ever before. Profits attract competition. That’s not new.

What used to be exciting and entrepreneurial is now systematic.

And people inside it are deeply defensive of this system. They don’t want change. Why would they? The system is working for them. It’s the rest of us who are just not appreciating how much value they actually create! (PE is not exactly known for its humility.)

But the system is good if you can get inside. Use other people’s money, take out debt, charge fees, and enjoy preferential tax treatment.

Still, there are signs of cracking - more recently, returns mimicking the S&P500 and longer hold periods are increasingly normal. Continuation funds are more common.

But the point is the system is asymmetric to the benefit of the private equity firms, the GPs.

Private equity general partners make money whether their investors do or not and sadly, whether they improve the companies they buy or not.

How? Fees.

Fees on capital raised, management fees levied on the companies, transaction fees, reimbursements, etc.

Keep in mind, these fees are disconnected from performance. Management fees are based on capital raised or charged to the companies for the pleasure of their ownership. On top of that, there can be other fees- transaction fees, deal fees, reimbursements, etc.

So right out of the gate, the firm is making money, whether they perform or not.

And when private equity does perform, they take a meaningful chunk of that value too. The classic 2&20 structure means they take a 2% fee on the capital raised and 20% of the earnings above a certain threshold (carried interest).

All together, ChatGPT reports private equity GPs collect 30-40% of the total economic value of any given deal (it actually caveats that it may be more like 40-50%).

Carried interest is designed to align incentives. It is payment for the firm's labor - not return on their own investment. The partners at a private equity firm may invest their own capital, but that is not what we’re talking about here. I’m just sharing the typical take home resulting from the structure. Lucrative.

On top of capturing a huge chunk of the economic value, believe it or not, much of the take home pay actually gets preferential tax treatment.

Carried interest is taxed at capital gains tax rates, not ordinary income.

But that makes sense since PE labor is creating real value, unlike teachers, plumbers, engineers, police officers, salesmen, warehouse workers, bakers, pastors, waitresses, lawncare workers, doctors, nurses, dog trainers, construction workers… you get the point.

To be fair, you can’t blame private equity for this - it’s the tax law. They’re just capitalizing on an opportunity, but again, it’s asymmetric.

Depending on the year, the private equity partner might pay a lower tax rate than the warehouse worker in the company his firm owns. It’s the Warren Buffett/secretary example.

Private equity’s job is to generate returns. That is the job for which they labor. And yet their labor gets taxed at 15–20%, while your labor gets taxed at 25–37% plus state?

It just begs the question… why in the world are we subsidizing the labor of private equity?

Keep in mind, they’re not deploying their own capital. They’re not the ones who have the capital (they’re just in the process of collecting it). They’re not the ones who run the business.

PE buys companies with other people’s money. They charge management fees to the company they own. And when they sell, they collect carried interest taxed as capital gains-not ordinary income like the rest of us.

But they don’t just buy companies with other people’s money - they also use debt. Glorious, non-recourse, printed-from-thin-air debt.

This debt creates risk. Obviously. But if the PE firm drives a company into the ground, they can walk away. Move on to the next deal with no obligation.

Employees lose jobs. Customers lose a supplier. Banks lose their money. But the PE firm keeps their fees. They move on to the next deal.

Again, asymmetric potential losses relative to the potential gain.

Meanwhile, the small business owning pharmacist who takes out an SBA loan to build his own business has to personally guarantee his loan. If the business goes under, he’s making payments until the bank is whole.

A student making an investment in education, with hopes of earning a living (future returns) is stuck with his loan too, even post bankruptcy!

So the pharmacist and student have to pay back their loans, but a private equity bro can load a company with debt, run it into the ground, and walk away scot-free?

Make it make sense.

(By the way, when new debt is issued, money is created out of thin air. This dilutes the power of your dollar- but that’s a topic for another day.)

Inside portfolio companies, the dynamic is just as distorted. MDs suggest ideas. Everyone scrambles. FP&A burns weeks. CEOs chase ideas they know are dumb because saying no is dangerous. CFOs burn out. Operators are neutered.

I used to think the people in seats before me, who I replaced, were weak. Losers. Why did this guy make this decision? Do things this way? Now I realize they were just beaten down, neutered by spreadsheets and initiatives. They were playing to survive, trying to hang on until their company sold.

But PE folks are mostly people who have never run a business, much less worked inside one. They know debt, models, covenants, and exit multiples. And now their spreadsheets impact the most intimate parts of your daily life.

They’re buying everything: Dentists. ENT practices. Veterinary clinics. Auto shops. Gyms. Valve distributors. Engineering firms. Healthcare groups. Fast casual chains. Your lunch. Your teeth. Your cancer treatment.

Do you really want spreadsheet-driven finance firms deciding how much time your dentist spends with you? Or which treatment plan your oncologist uses? Or where the meat on your sandwich is from?

These are finance guys with spreadsheets. Again, these are people who have never been in a business much less run one, and you think that they have the tools and skill set and judgment and moral compass to drive businesses that impact not just your day-to-day life like where you have a sandwich, but your actual health? Your lifespan? Do you expect to live longer with private equity backed healthcare?

Take Jersey Mike’s. What do you expect now that PE owns it? Higher quality meats? Better trained employees?

No. You expect: prices to go up, quality to erode, employees to become less friendly, the store to be less clean, etc.

That’s not innovation. That’s a transfer of wealth from customers and workers to shareholders.

And that’s a core problem with private equity - there is no innovation. There’s no risk taking. How can you when you are going to sell as soon as you can? (but not before three years - gotta get that cap gains treatment ;))

Hopefully we’re wrong and we all love Jersey Mike’s even more in a few years but the point is - that’s not your expectation when you hear PE bought your favorite restaurant.

No one is excited when they hear private equity bought their favorite business. That tells you a lot.

Operationally, private equity often claims to take a long term view but when you know you’re going to sell in just a few years, that’s just not what happens in practice.

When you are thinking of selling your home, do you replace the roof? Nah, you just replace the shingles, put a bucket in the attic and hope the next buyer doesn’t notice too much.

That may be an extreme example, but it does happen. Regardless of whether that’s the norm or the exception, it’s impossible to be truly long-term oriented when the incentives are to maximize short-term gain.

Truth is, PE is optimizing for 3-7 years time horizons, not a 20-year competitive advantage.

There is no vision setting, no ideating ten years down the road, no innovation. There are just hard, cold initiatives designed to “optimize” and drive the profits higher.

What would I change?

Despite the above, I think private equity investing can be a force for good. Like I said, I’ve seen great firms, great deals, and great people. It can be done well.

PE would do well to recognize how others perceive them, address the criticisms, and adjust. You see some attempts at that lately (e.g., KKR’s employee equity program being emphasized and advertised), but PE is just not great at admitting mistakes. They seem (to me) to be in an especially defensive, insecure posture.

That may be because returns have diminished, holds are longer, and continuation funds have risen in prominence.

But there’s more to adjust than just perception.

Longer holds would help. Making firms stand behind the debt they use would help (at least require them to pay back the mgmt fees they’ve collected when a company defaults). Transparently connecting fees to performance would help. Ending preferential tax treatment for carry would help. Forcing PE bros to actually work inside operating businesses they control would help.

I think the industry is heading for a bifurcation. The mega-funds will keep getting bigger. They’re powerful and political and will dominate fundraising. At the other end, lower-middle-market firms will keep creating real value by taking small businesses to the next level. The middle will get squeezed. You already see it… middle market firms selling stakes in themselves to the big guys (just another PE deal).

The real bottleneck going forward won’t be capital or deals. It will be operators. Financial engineering has been competed away. Sourcing has been automated. Spreadsheets can be done with AI (or will be soon). What actually creates value now is people who know how to run, fix, and grow businesses.

That’s a good thing, I think. The emphasis isn’t even really on operators so much as it’s on creating real value. Maybe PE bros need to lose the deal sleds for boots and become operators themselves…

Which raises an uncomfortable question for private equity: if great managers will create more value in the future, why do they keep giving most of the economics to spreadsheet people?

I think for PE’s next chapter, you will see some corrections, and I think those will be great. I think time horizon will be forced longer. You’ll see fewer 3–5 year windows and more 5–7. I hope that goes to 7–10; maybe it will.

For my money, the lower middle market is the place to be for the foreseeable future in the PE ecosystem. There, it’s genuinely helpful to equip companies with new tools, sophistication, and access to capital that they may or may not have ever been exposed to.

“Launching” these smaller businesses to the next level is valuable to all of us so long as it doesn’t end up in the never-ending cycle of selling from PE firm to PE firm to continuation fund and so on…

Despite the dour assessment, private equity isn’t evil. It’s just a tool, a strategy. Or it’s supposed to be.

There are always good and bad firms, good and bad people and so on. Good ones exist for sure. But that is just not the dominant flavor anymore.

The GP captures upside through fees and carry while transferring downside to LPs, lenders, workers, and the state. This is a structural free option.

Private equity is the only industry where you can lose other people’s money, fire workers, default on debt and still become personally richer.

It has generated a commoditized wealth-extraction machine that increasingly shapes society without accountability.

And I don’t think anyone wants to live in a society run by spreadsheet aristocrats.

English

No Coupon At All retweetledi

Dan, if anything happens to you, it'll be from chlamydia, not the Mossad.

You’re not exactly Iran’s nuclear archive, bro.

The Mossad doesn’t take out guys whose biggest secret is “I faked being rich and caught gonorrhea in Tulum.”

You’re the final boss of STD Awareness Month, not a geopolitical threat.

Take your meds. Log off. Nobody’s watching you but the CDC.

English

No Coupon At All retweetledi

Brits: “ohh prices are a bit steep, not sure I can afford to put the boiler on even though I’m freezing”

Americans: “My driveway is a bit slippery, better activate my WALL OF BOILERS to heat it”

English

No Coupon At All retweetledi

*BIDEN HAS REQUESTED PELOSI TO REMAIN IN CONGRESS AS HEAD OF TRADING - CNBC

English

No Coupon At All retweetledi

What should a top bucket bonus for a second year Analyst look like these days? Hard to benchmark with everything I’m seeing

English

So my trip to Ocean City MD today. This is a middle class shore town. Paradise for the Poors

Spoke to a local friend. He said all summer it’s been an absolute ghost town. They are running the go cart track at 50% capacity

Bars empty. Said he’s never seen it like this in 30yrs

English

Early career years are intimidating—there's so much that feels out of your control.

Here are the career principles I wish I knew when I was starting out:

English

No Coupon At All retweetledi

English

@TheVixAndCoffee @SeanODowd15 @SBA_Matthias Wildly depends on bonus which varies a lot with the market. Base is around 150-160 though.

English

No Coupon At All retweetledi

you might want to think about intercepting some profits sometime soon…

DraftKings@DraftKings

Intercepted

English

No Coupon At All retweetledi

@JetsFan1966 The Chairman of the World Economic Forum is Klaus Schwab and he does not have any affiliation with CS&Co.

English