@WuffettBarken @Rory_Johnston China will access its SPR. Once it exhausts it's SPR then what you are suggesting may happen.

English

Niccan

68 posts

Bessent to @kwelkernbc: “In essence, we are jujitsuing the Iranians. We are using their own oil against them.”

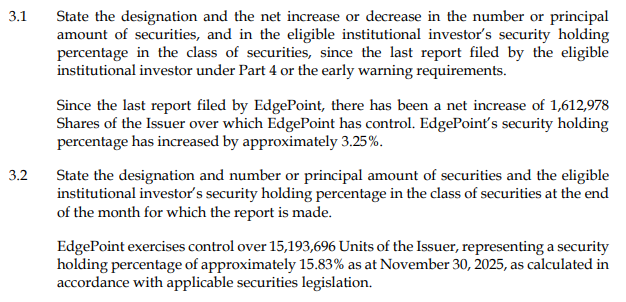

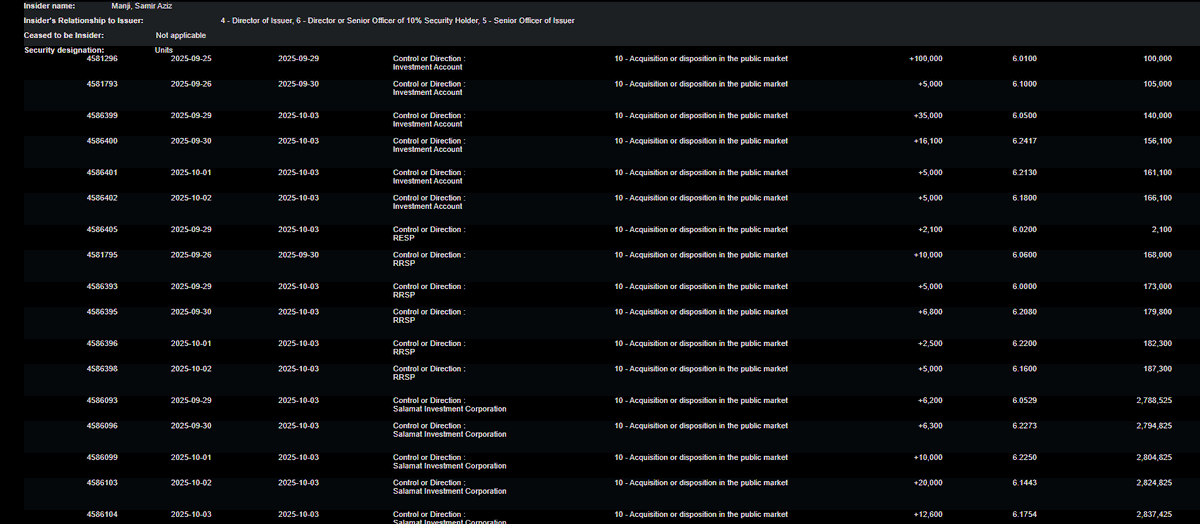

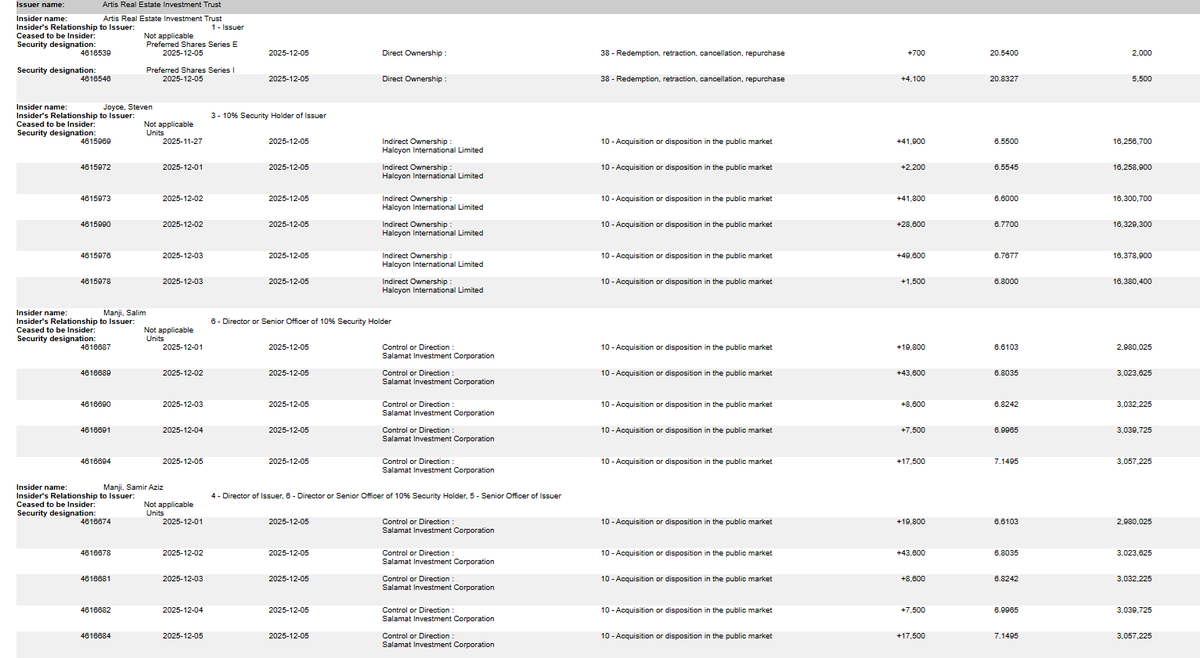

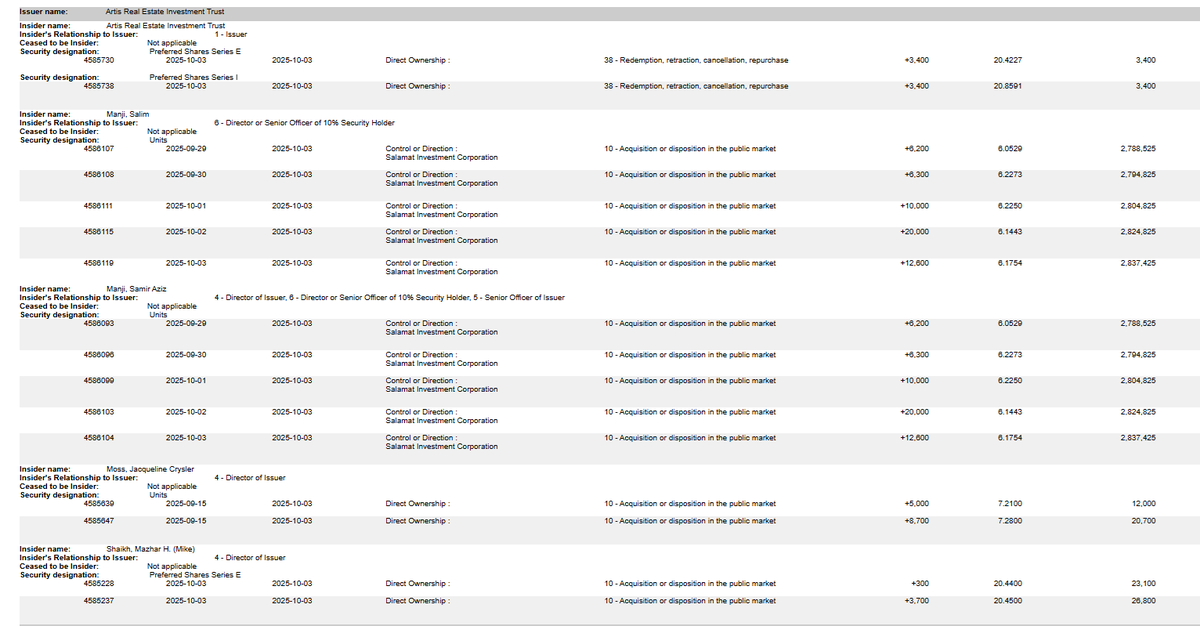

$AX.UN's CEO Samir Manji added $344,500 worth of common units on the pullback. Others insiders have added common and prefs as well. Seems like a vote of confidence on the forthcoming deal.

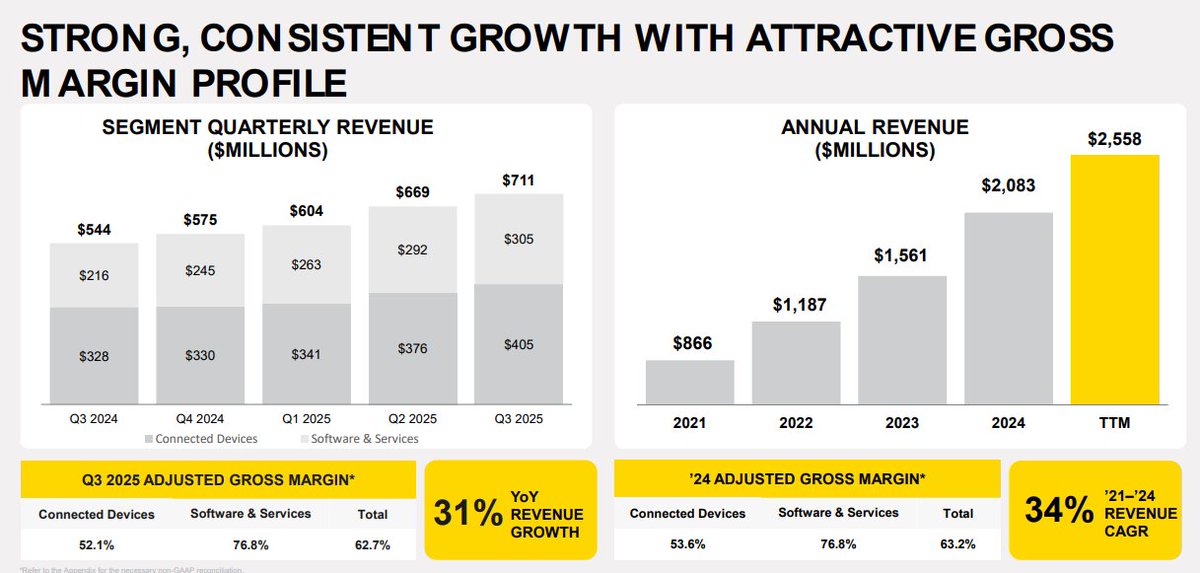

Evertz an AI winner🤔"...Evertz, in its multi-decade pursuit of solving the increasingly complex, high-bandwidth, and low-latency challenges of the professional media industry, has inadvertently engineered a suite of hardware, software, and intellectual property that positions it as a potential and credible contender in specialized segments of the AI infrastructure market." $ET.TO

Buy $AX.UN before the re-rate as a growth bank? Artis trading very cheaply today and out of favor. As a liquidation story you could likely make a lot of money recyling capital which is their go-forward plan. Samir Manji, Ben Rodney/RFA, both smart and highly aligned insiders here