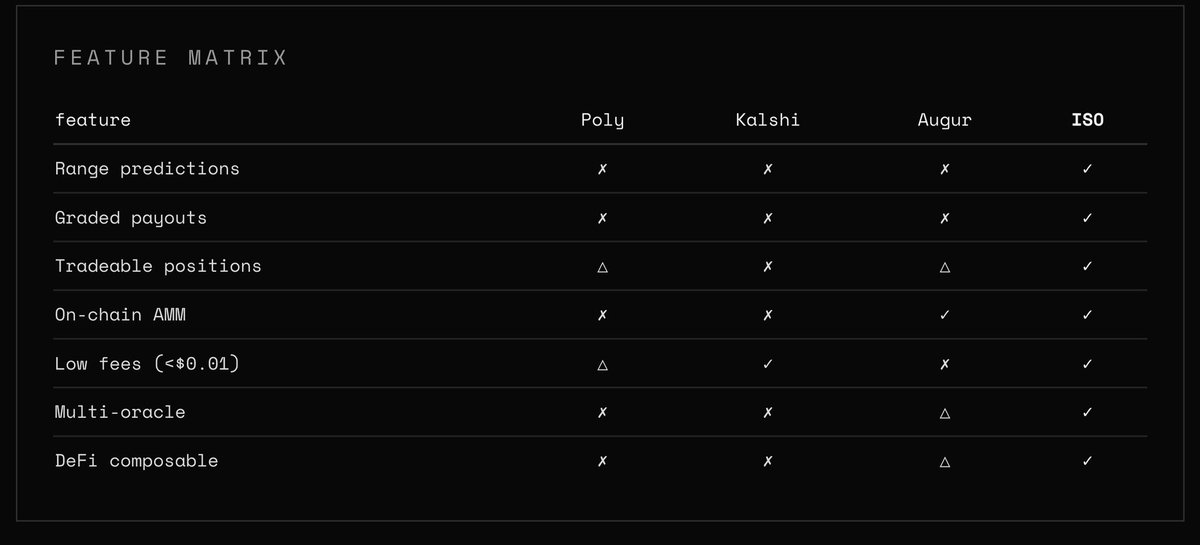

isometric@isometricmkts

While we are incredibly excited for mainnet, we've been thoroughly auditing the code internally prior to the devnet -> mainnet transition, namely the payout logic on a settled market to ensure payout match matches the Gaussian design that is intended.

We have completely reworked payout claiming after combing through it all day:

• function rewritten with correct args

• heavy bug fixes with tx simulation failing

• Portfolio button fixed as conditional Close/Claim based on market status

• Claim button now existent in Portfolio for all users

• Claiming now burns the positional NFT

If you participated in the ASTEROID market that closed last week, you can now go into Portfolio and click the claim button to claim your Gaussian payout based on your ranged estimate.

Image 1: Position now burns on close (as intended).

Image 2: Proper gaussian payout via the Claim button post-settlement; vault -> payout to wallet (solscan.io/tx/5aBxKhP8bAu…)

Users are encouraged to visit their Portfolio page and claim their Gaussian payout for the settled ASTEROID market (if participated in) to validate these fixes.

We needed to do this deep audit for a few reasons to ensure the payout math is proper on-chain once more as the payouts are the crux of this ecosystem, and they computed properly end-to-end.

We're going to walk through this thoroughly as we feel this needs to be explained.

This position on the ASTEROID market— we bought a position on this market predicting the ASTEROID market cap would land within $129M - $276M by April 23, 2026. We paid ~$8 USDC for this with LMSR rounding.

Market settled at $139M at expiration (end-of-day for April 23rd, 2026).

As most prediction markets are binary (yes/no, you get either 100% correctness or 0%)— Isometric uses a smoothed payout (how much of a Gaussian distribution centered on the settlement price falls within our traded range; this fraction times our cost = our payout).

The bell curve for settlement was centered at $139M (settlement price) with a spread of about $24.5M— most of its mass was roughly between $90M and $190M.

Our range was $129M to $276M. To find the frauction of the Gaussian inside [$129, $276] we measure the sigmas-from-center (z-score).

z_low = (129 - 139) / 24.5 = -0.408

z_high = (276 - 139) / 24.5 = +5.59

The lower edge of our range is 0.4 sigmas < settlement, upper edge is 5.6 sigmas > settlement.

The system then decides which fraction of a unit Gaussian lies below z:

Φ(-0.408) ≈ 0.342 (34.2% of the bell curve is below our lower edge)

Φ(+5.59) ≈ 1.000 (essentially 100% — way out in the tail)

With the fraction inside our range equating to 0.658 so 65.8% of the Gaussian centered at $139M falls within our $129-$276M range.

So therefore our payout would be:

payout = cost × fraction = $7.999994 × 0.658 = $5.267

Which matches the exact on-chain amount with proper rounding and it just properly worked via claim for the first time in history.

Settlement at $139M, our range started at $129M and goes to $276M, so:

• Settlement within our range (good)

• Only $10M above our lower edge

• Upper edge is far away from settlement

If we'd have been more narrow in our predicted and traded range and centered (around like 130-150m), our payout would've been higher as the Gaussian would've mostly fit within the range.

Missing it entirely, we would've had a near-zero payout, this is the "you were just blatantly wrong" case.

This is the core differentiator versus binary markets: baking in partial credit.

All-in-all, math matches design. Protocol paid fairly based on design.

Being roughly right gets you roughly paid rather than losing everything for being slightly wrong.

This was a critical test we needed to do to ensure everything worked on that side properly.

We've concluded internal audits from end-to-end and are now patching up a few frontend bugs— mainnet is coming soon!

We apologize for the delay(s); however, with a protocol as dense, novel and complex as Isometric, there must be meticulous care at each level prior to involving real money.