yoma

2K posts

The young guys want trading advice, what am I suppose to say?

I guess learn chess + poker, read niederhoffer and robot james

English

yoma retweetledi

yoma retweetledi

"Crypto is the dumbest market in the world"

Scott Phillips (@ScottPh77711570) runs HyperTrend — $20M of his own capital, one losing year in six.

His edge? Picking the table big firms can't sit at.

"There's no second-best counterparty in crypto. You see crime, you run towards it — crime is the foundation of edge."

We cover:

- Why crypto still has edge in 2026 — even when your uncle is talking about Bitcoin at Thanksgiving

- The simple rules (buy 20-day highs, top-20 coins) that print through any market

- Why stacking trend + momentum + carry gets you there from a spreadsheet — no automation required

- Price-insensitive buyers (Saylor), price-insensitive sellers (North Korea) & why both are permanent alpha

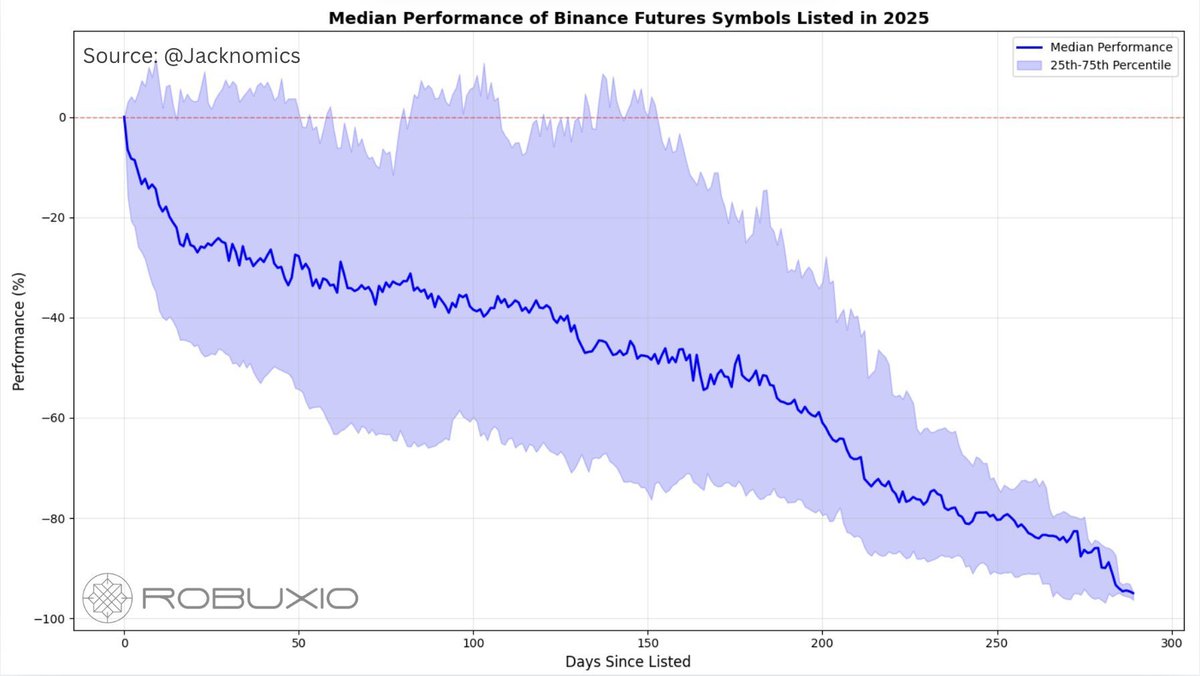

- The 90-day Binance listing short — an edge hiding in plain sight in market maker contracts

- Why most shit coins trend to zero — and how to trade the ones that don't

- Building a tokenized, permissionless DeFi hedge fund on hyperliquid — 2 & 20, fully on-chain

- Why the best quant firms are run by near-non-verbal autists with one translator

Thank you so much @ScottPh77711570 for coming on the pod!

Highlights:

01:04 Table selection and the math of competitive alpha

06:21 Why basic trend following yields outsized Sharpe in crypto

08:49 Why market inefficiency persists despite institutional inflows

14:58 Price insensitive buyers: Cults, VCs, and North Korean hackers

17:17 Factor analysis and the size-decay effect in shitcoins

25:40 The structural edge in mid-frequency crypto strategies

32:43 Tokenized DeFi vaults and on-chain hedge fund governance

40:43 Designing a robust portfolio: Equal weighting vs. MVO

44:21 Sourcing alpha from ghost chains and VC exit liquidity

49:58 Exploiting market maker contracts and post-listing drift

53:55 Operational alpha: Managing margin and manipulated funding rates

01:01:13 Shifting from quant to CEO

01:11:28 How to bridge the mentorship gap with elite traders

01:22:38 Building network triads: The secret to compounding social capital

01:29:23 Why 10x goals require total identity transformation

English

yoma retweetledi

CZ I held all the tokens listed on Binance last year

Please advise

CZ 🔶 BNB@cz_binance

I've seen many different trading strategies over the years, very few can beat the simple "buy and hold", which is what I do. Not financial advice.

English

English

@0xfdf @liquiditygoblin @macrocephalopod The shit we have that “works” will stop working soon, and we have to find new shit

This is why many kwants get offended at the ta crowd, as though idiots somehow dont have to navigate the same bullshit we do

/fin

English

Lets talk about building real nigga trading features

Things that are ungodly high Sharpe

1

Temu Robot James@ScottPh77711570

@firstlawofvol @systematicls @pedma7 @maruushae @izebel_eth The basic idea of modern kwanting is you would find as many of these things as you can yhat predict prices (weakly) and blend them into “one predictive number” and then size your positions so your portfolio wiggles the amount you want it to

English

yoma retweetledi

政府・与党 来年度の税制改正 暗号資産の所得 分離課税で調整

news.web.nhk/newsweb/na/na-… #nhk_news

日本語

【日本語意訳版】Lighter創業者Vlad氏Podcast インタビュー(2025.11.25):誰もが多様な資産にアクセスできるようにするーという意味での”金融の民主化”だけじゃなくて、 「小さな個人のユーザーが、無料 note.com/daifukufruits/…

日本語

yoma retweetledi

kwant fomo

it is better to do simple dumb things than to do "sophisticated" things badly.

English

Paradexの仕様をうまく突いて儲けたbotterの話、面白かった

出てくる損益曲線がえげつない

Armv7l@Armv7lFx

New article is out on how i drained 5 fig from Paradex (And abused their API), with more technical explanation, lot of footage. for those who wonder what i do on daily basis, and are curious and want to learn more, or get dopamine armv7l.substack.com/p/how-i-draine…

日本語

yoma retweetledi

my takeaway from these excellent CBB threads is that "table selection" remains deeply underrated

effective table selection (picking the best markets to deploy on) drives far higher long-run EV than incremental infra tuning in hyper-efficient markets

this is one area in which i, frankly, need to be better

clearly you can be a B-tier operator in soft markets and make gobs more money than A-tier operators in competitive markets

anyone have a heuristic for crypto table selection? for quant trader types

English

English

@investingidiocy @liquiditygoblin @therobotjames We are going to open up our vaults for deposits soon

Fees are 2/20

It should be *comfortably* over Sharpe 2.0 at scale (probably more at first)

If you'd like to know more about our trading systems watch this

youtube.com/watch?v=GWZcyM…

/40

YouTube

English

A few things I can show to those doing @investingidiocy style trading on shitcoins

An easy win is to rebalance not to the center (like Rob does) but back to the edge of the band

This is because tradfi futures are in contracts of 100k-ish and you want to optimize for number of trades

Whereas crypto you can make tiny trades

It’s a small but meaningful improvement

1/

noalphadecay@noalphadecay

I ran a few simulations on historical data to see how buffering affects trading behavior and the performance of a single-coin portfolio using the trend follow signals previously presented. to be clear: this is not about cherry-picking an optimal value - it is about building intuition for where the limits lie and how the transaction cost model interacts with different buffer widths with buffering, the goal is to reduce trading costs that come from frequent rebalancing. before going further, let me define what I mean by a buffer zone (see [1] for details): given the trading signal and other parameters of the system, we compute a target position. around this target position, we define a buffer zone (e.g., ±10%). the question then becomes: what do we do when the actual position moves outside that zone? in the simulations, I followed the Carver-style approach [1]: when the position breaches the buffer, it is rebalanced back to the nearest boundary of the buffer zone. as the chart below shows, increasing the buffer width naturally leads to fewer trades (BTCUSDT, sample 2021-2025) this introduces a trade-off: a wider buffer means lower transaction costs, but it also means your position lags further behind the target position if the target position drifts. the question is: how much does it really matter whether the buffer is 5%, 10% or 20%? as mentioned, the assumption on the transaction cost model is crucial here. I assume the following simulated fill-price model order_fill_price(t) = close(t) * (1 + order_side(t) * (slippage + spread)) - close(t) is the close price of an bar update. I assume execution occurs immediately after this update - order_side(t) is an indicator: buy (=1), sell (=-1). - slippage represents the assumed market impact (in %). - spread represents the BBO spread (in %). to stay on the conservative side, I include spread cost, because we do not know if the close price of the bar update was a deal on the bid or the ask price in addition, I include transaction costs to account for the assumption that execution mainly happens with IOC orders (taker fees) in my case, I think this model is not far from reality - it is a reasonable approximation for smaller-sized trades. however, for large rebalancing orders that must be executed over time, this assumed fill-price model is overly simplistic let’s have a look at the simulation results. the chart below shows the annualized Sharpe ratio for BTCUSDT under different slippage assumptions (0% to 1%) and buffer widths (0% to 25%). - for low slippage values, frequent rebalancing does not cost much performance - the Sharpe ratio stays fairly stable. only when the buffer width becomes large we do see a noticeable decline - for higher slippage values, the expected trade-offs appear: buffering reduces trading frequency and thus transaction costs, which initially improves Sharpe. however, when the buffer becomes too wide, the position starts to lag significantly behind the target, leading to weaker performance the chart below shows the same simulation, but with Sharpe ratios normalized to 100 at their respective peaks and averaged across several coins (BTC, ETH, SOL, DOGE). this helps visualize the general pattern across a few large-cap coins rather than focusing on BTC only these results simply illustrate how the interaction between slippage assumptions and buffer settings affects portfolio performance under a simple fill-price cost model. other execution assumptions would naturally lead to different outcomes references [1] carver, r: advanced futures trading strategies

English

yoma retweetledi

yoma retweetledi

What should you do?

You should have the exposures you want

That probably means you want a little less risk than you wanted before

And you should be a bit less confident in your ability to predict the future

Do that, wait for edge, and you’ll be fine

/fin

English

A thread on profit taking for non-nerds

From first principles

1/

0xPonzi(bunny arc)@Freenotthinker

@ScottPh77711570 Hi Scott, even though you are an algo chad, is there any advice for profit taking and risk management for normies like me? 🙏

English

substack.com/home/post/p-17…

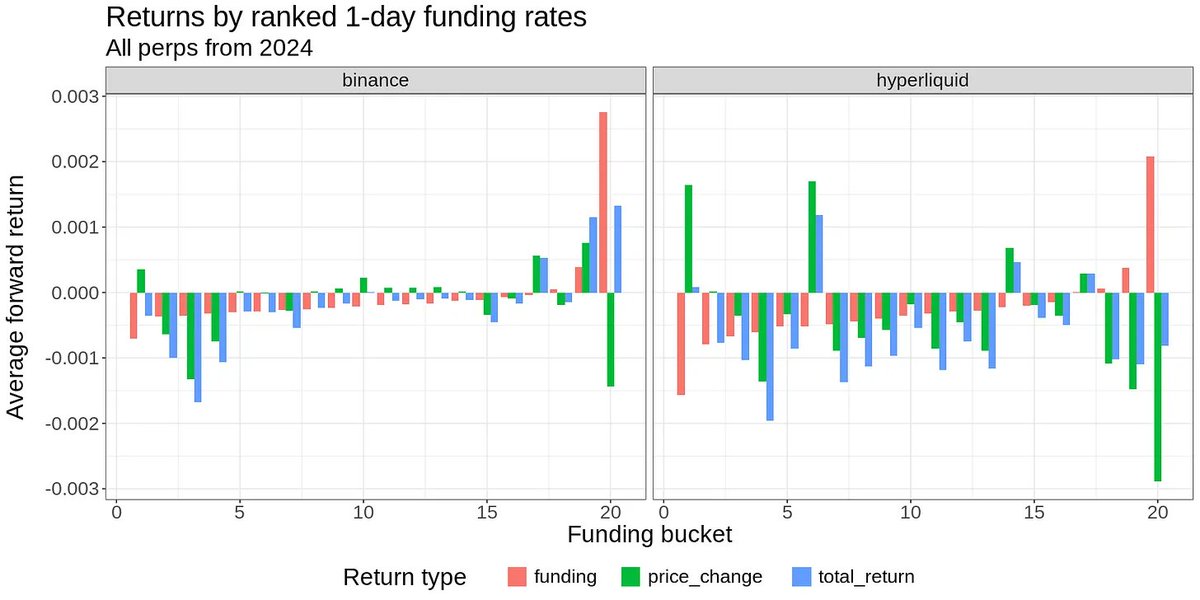

BinanceとHyperliquidでfunding rateが大きくマイナスの場合(ロングが受け取り、二つの図の右端)の値動きが異なるという記事。

これは、HyperliquidではKYCがなくインサイダーが売っているからではという仮説

日本語

yoma retweetledi

For my first substack post about quant trading, here is the insight i would give to anybody starting or needing a reality check.

"No Courses, No Mentors, Just 2 Years in the Crypto HFT Trenches"

armv7l.substack.com/p/no-courses-n…

English