@British_Airways I will raise a complaint if it means that something will happen about the standard of vegan options. This is not the first time, it is generally lacking, but this is on another level 🤷🏻♂️☠️

English

Oliver Bennett

2.6K posts

@oliverbennett_

I plan to live forever or die trying.

🚨 BREAKING: MPs are being recalled to Parliament tomorrow at 11am to discuss British Steel's future

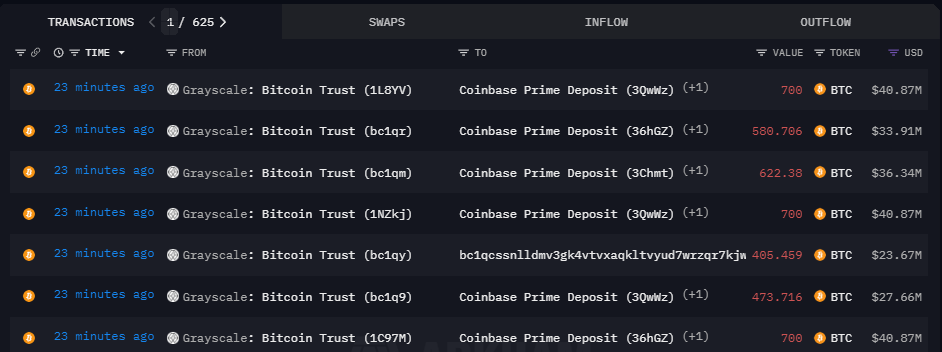

GBTC just sent ~1.0k #Bitcoin to its Coinbase premium account (~$58m). Less than yesterday, and in the first two days of the week the daily outflow has been lower than $100m.