Sabitlenmiş Tweet

I never post my trades because I don't believe it benefits me in any way. But I will do it just this once.

99% of you FinTwit regards are cowards. Too emotional. When your positions are up, you are celebrating. Gain porn falling out of everyone's assholes. When your positions are down, you're pointing fingers at other people. Mad that other people may be succesful and bitter you aren't. Refusing to point the finger at yourself and take accountability for your mistakes.

x.com/i/status/20195…

$IREN is 80% of my port. The past few weeks were brutal, with my account drawing down nearly 50%. But I was able to mitigate it to a small degree.

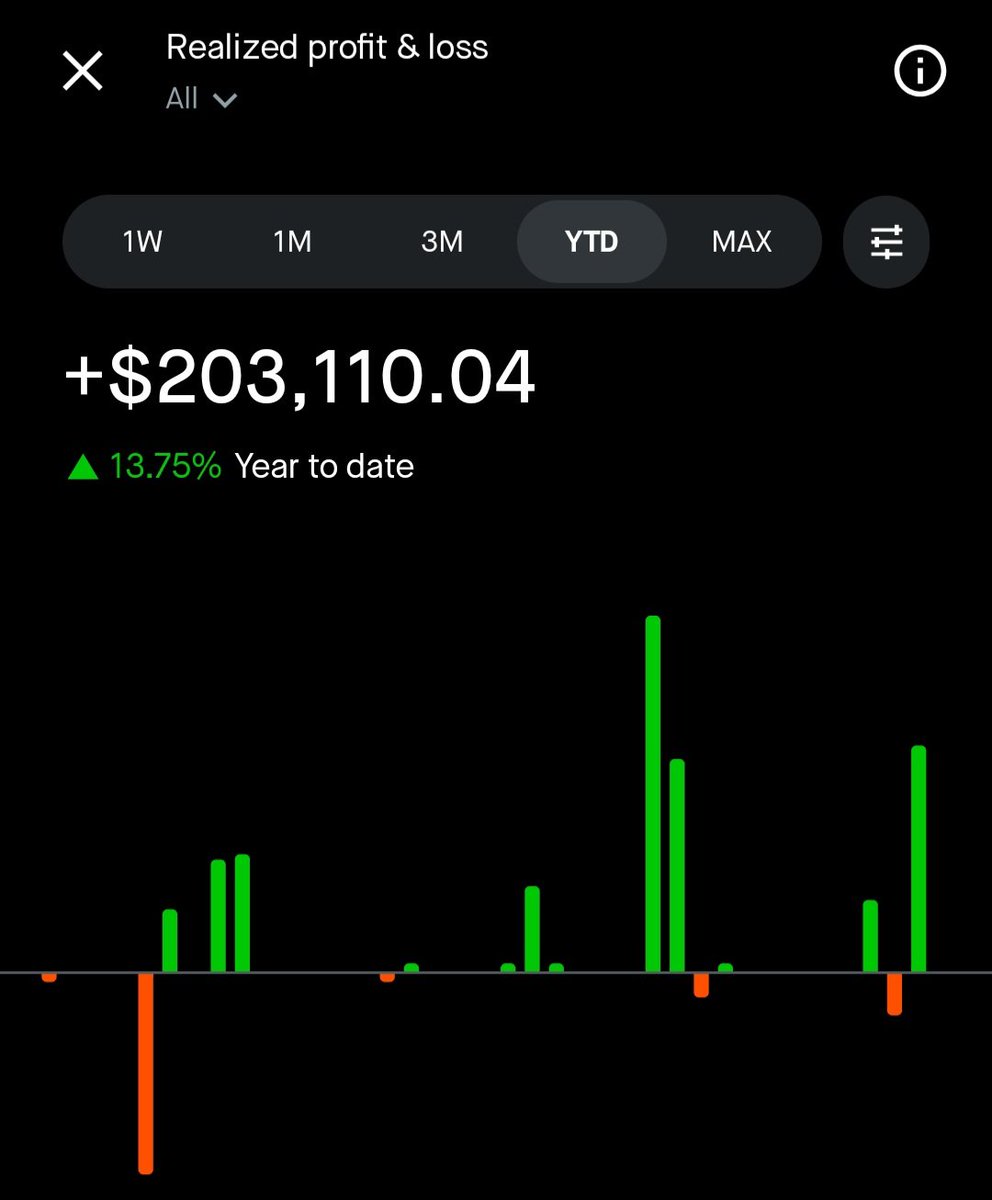

$203K of realized PnL YTD. My only other options position is a short $38 $IREN put expiring 2/13 that I am up $7,500 on. This PnL is not from taking profit on other positions. $150K of this comes fron selling covered calls, short puts, and put credit spreads, all on $IREN.

You guys make sarcastic remarks like "apparently everyone knew this would be the bottom." You know in your heart you are lying to yourself, twisting other's words, making them sound like furus to make yourself feel good. Mental masturbation that is destroying your progress as a trader and investor.

Talk is cheap. But there is a lesson in every post. Every reply. Most of you will never realize this. You can learn from the most regarded people. If a regard is right and you were wrong, it doesn't matter whether he's regarded or not. It doesn't matter whether you're smart or experienced or rich. You were wrong.

Stop pointing fingers at other people. Stop making statements like "I know what I own." You made a series of mistakes. You fucked up letting your portfolio draw down 20, 30, 40, 50%. Spend your mental energy looking for solutions and understanding your mistakes rather than engaging in mental masturbation.

English