@SetupAlpha Yea but that’s just curve fitting , there will always be 1 parameter that will look good

English

Sam Weil

336 posts

The two most serious problems are a mismatch between the stated and implemented objectives, and assumptions that largely remove adverse selection.

Ex-Man AHL ($70B firm) fixed-income head on breaking into quant: "You've got a much better chance of being hired by the world's best hedge fund from a non-target school with no qualifications than by trading your own money." Rob Carver (@investingidiocy) — ex-Man AHL, ran a multi-billion systematic fixed-income book | now a one-man shop across 200+ futures markets "I don't really believe I've found any inefficiency — basically all the money I make is risk premia." We cover: - The career myth that won't die — getting "noticed" by trading your own money is a one-in-a-billion event - Why he insists he's found zero market inefficiencies — it's public risk premia anyone can harvest - Skepticism as the #1 trait — every career error he's seen traces back to overconfidence in a backtest - Why "the best quants come from physics" is mostly path dependence — the Yale-historians thought experiment - His actual process: ~1 new strategy a year, a 1-in-5 strike rate — & he thinks more research would lower it - The real innovation of his last decade — running 200+ futures on a small account, not finding edge - Why he'd never join a pod shop — even though he reckons he could land an offer every couple of weeks Highlights: (00:50) The $1B loss week — why the desk stayed calm (02:45) Why he turned off his P&L email (06:40) Do the best quants really come from STEM? He pushes back (09:55) The Yale-historians trap — path dependence in quant hiring (11:35) The one trait that matters most — skepticism (13:00) The Sharpe ratio's blind spots — & the LTCM case (15:55) Geometric return vs Sharpe — the leverage catch (17:40) Avoiding overfitting — explicit vs implicit fitting (21:55) Why an honest backtest should look worse (23:05) Alpha decay by trading speed — HFT vs slow systems (25:35) Inside the portfolio — the full 10-rule suite (30:30) The career myth — trading your own money won't get you hired (31:55) Why he calls his returns risk premia, not inefficiency (33:55) His real innovation — 200+ futures on a small account (35:40) How Man AHL reviewed, vetoed & shipped new strategies (39:30) Will capital consolidate at Citadel & Millennium? (41:45) "My DMs are open" — & why he'd still never join a pod shop (42:45) The AI talent-war parallel — who you actually want to hire

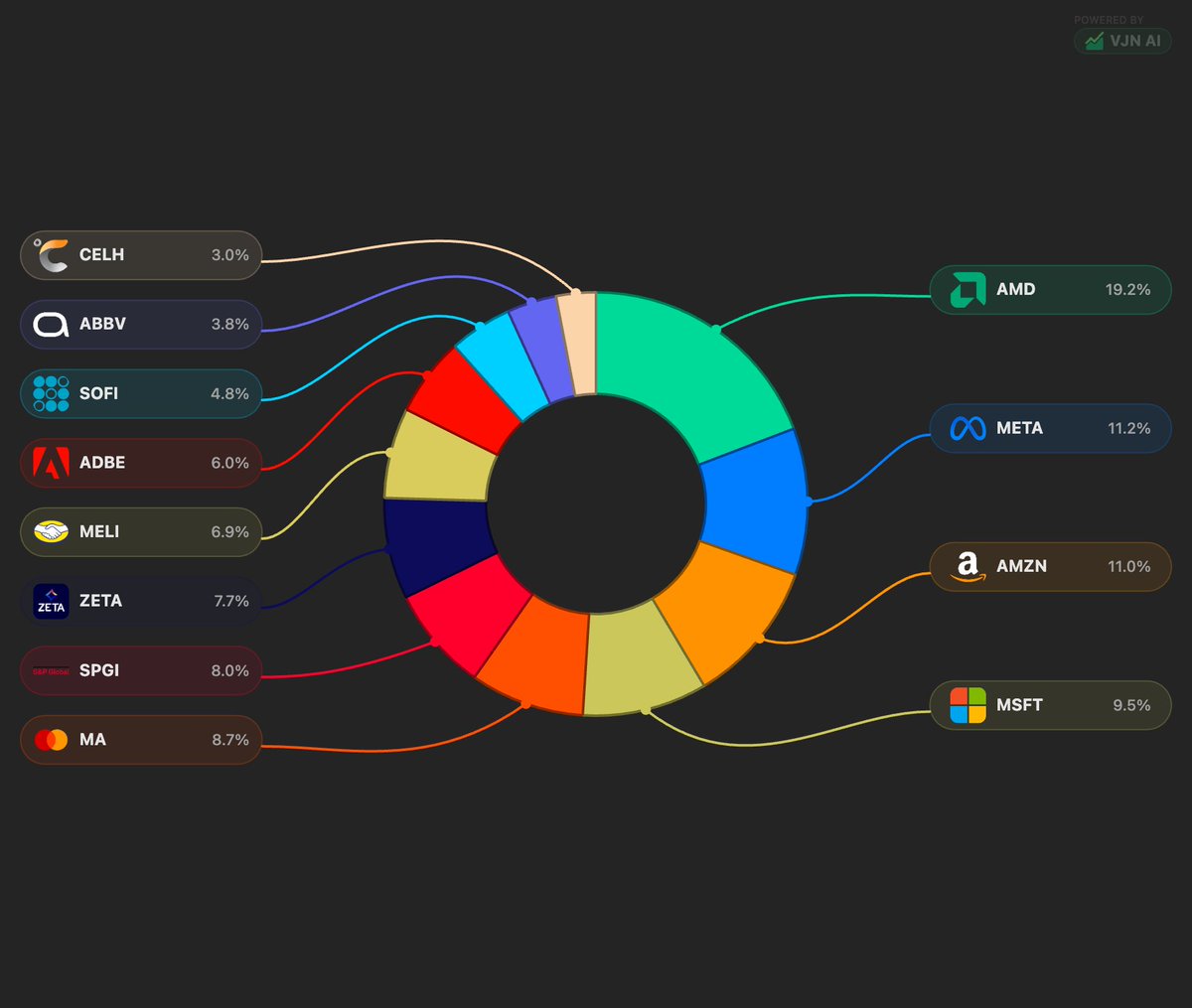

Best part of being a quant is looking at my top holdings, not recognizing any except the one I absolutely hate the company and would never buy the stock.