Asim Riaz@AsimRiaz1978

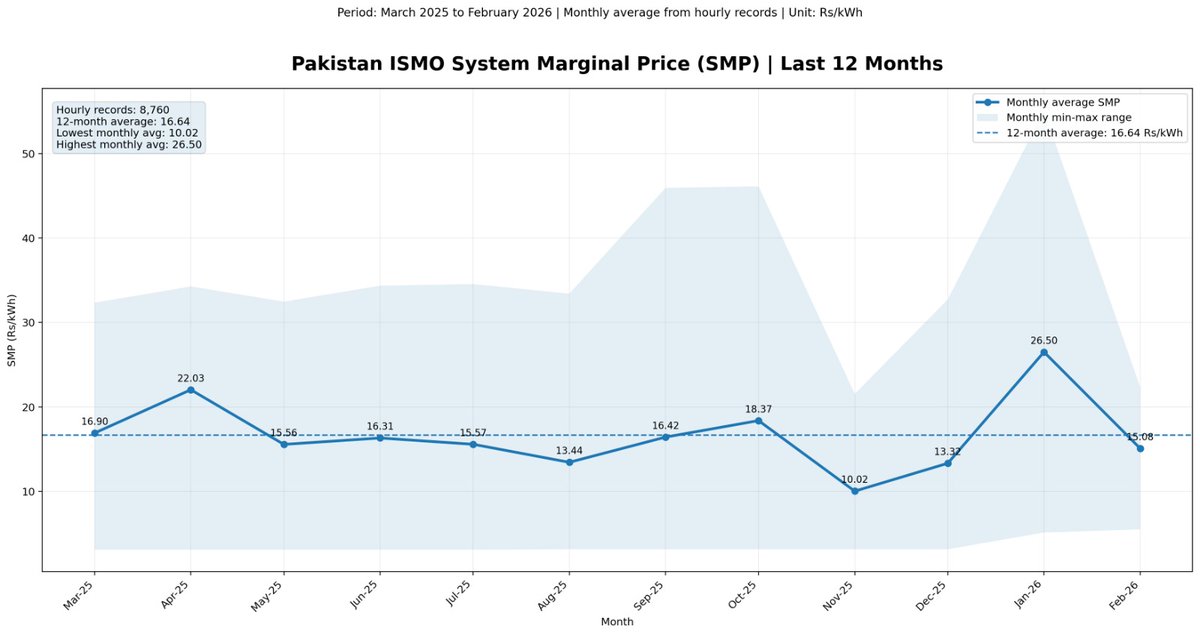

Analysis of ISMO Hourly System Marginal Price (SMP)

Pakistan’s next power-sector reform priority should be to move from a megawatt-addition mindset to a system-optimization framework. The ISMO hourly SMP dataset shows that the central constraint is no longer only capacity availability, but the timing, flexibility, and deliverability of electricity. The early duck-curve signal is now visible: low-marginal-cost solar and must-run resources are pushing midday prices below nighttime levels, while the evening peak has become the system’s value zone.

The 18:00 to 23:00 block is where dispatchable capacity, storage, demand response, ramping capability, and ancillary services carry the highest economic value. Scarcity is episodic, with less than 2% of hours exceeding Rs 40/kWh, but the daily ramping requirement is structural. SMP is therefore an important market signal, but it is not the consumer tariff. Pakistan’s affordability crisis remains driven largely by fixed-cost recovery, underutilized contracted capacity, T&D losses, weak recoveries, and legacy contractual obligations.

The CTBCM framework must now evolve beyond basic bilateral energy trading into a deeper market architecture. It should price energy, congestion, balancing, reserves, deviations, and flexibility. ISMO’s development of transparent market dashboards is an important step toward a credible and rules-based wholesale electricity market. These dashboards should progressively cover hourly SMP, system demand, generation mix, marginal units, reserve margins, constrained dispatch, curtailment, imbalance prices, and ancillary-service procurement.

NEPRA should use this information to strengthen dispatch discipline, market monitoring, transparency, and regulatory accountability. A competitive market cannot rely on price publication alone. It must provide clear, bankable, and auditable signals for investment and operations.

Distributed solar policy must also evolve. Flat compensation for surplus midday exports risks creating artificial arbitrage and shifting fixed grid costs to non-solar consumers. Future solar incentives should prioritize self-consumption, storage-backed exports, time-sensitive net billing, smart inverter functionality, voltage support, and controlled exports during higher-value periods. Solar remains central to Pakistan’s energy transition, but its value must be aligned with timing, location, and grid-support capability.