Yabadabadoo

2.1K posts

@aleabitoreddit @aleabitoreddit,非常感谢您这么详细地解答我的问题! 从toxic financing、ATM dilution、债务利息到股权激励的分析都超级实用,让我对早期AI机会的筛选又多了一个清晰的checklist。尤其是$IREN vs $NBIS的对比例子,讲得特别透彻。 会继续认真跟着您的分享学习,期待更多干货!再次谢谢女神!

中文

Sure, #1 thing is toxic financing structure/float dynamics.

Best example is current Neoclouds landscape:

- $IREN is basically trash, since they have $6,000,000,000 ATMs and virtually infinite dilution, likely selling into every rally (structural overhang)

- While $NBIS is now YTD 153%+, from optimal structures (eg. $NVDA direct funding, mix of convertibles, etc.).

- On the other hand, $CRWV has endless debt interest given they took out high interest rate loans to finance GPUs.

It's extremely nuanced, but you need to take a look at the float dynamics.

If they're legitimately a good company, then it might be a good idea to go long after all the existing holders get diluted to oblivion.

But if you care about your equity appreciation, it's a good idea to stay far away from toxic financing structures or toxic overhang (eg. debt interest, that eats away at a company FCF long term)

With smaller companies, they have this all the time, like

$SLNH, where there's new $500m ATMs on a $250m MC.

Or like $BKKT where there's endless dilution to fund executive pay.

With these companies you're basically transferring your money over to the company while influencers talk about them. So those are red flags.

With many software names like $SNAP, they mask stock-based compensation with profitability. So while the company optically looks profitable, you'll likely see the value of your equity decrease due to dilution.

There's endless types of these share structures you need to look when screening ideas.

跟着Serenity学投资@chuge857

@aleabitoreddit 想请教一个具体问题: 你在筛选这类早期机会时,除了「现实世界观察 + 行业人脉」,还有没有一个你自己总结的「最小验证 checklist」?比如某个信号一旦出现,你就会把仓位从观察池提到重仓池? 非常欣赏这种把金融、VC和硬科技研发背景融合起来的打法,期待继续看你分享!

English

English

Added to my clean water contribution...

It's cool how they've gamified donations! Goal is to reach 100,000 lives changed through @charitywater.

Despite the odd comments in my last post, after doing my due diligence, @scottharrison and his team seem exceptionally trustworthy.

Wayne Liang@wliang

Lately I've been seeing a ton of people donate their X payouts to charities, and it's wonderful! For the last ~5 years, I've been sponsoring numerous children and funding schools in Ghana, but I've never contributed to clean water... Started my new journey with @charitywater!

English

@TejKhaled @daniel_koss "we" ? Reread what I wrote. I wasn't in on it for that lol.

English

@robbhope @daniel_koss You're panicking because a stock dropped with the entire market? Come on man.

We went up 17% in a day a couple days ago. 10% up and down has been part of this stock for as long as I can remember. Get used to it, and get some conviction.

English

@daniel_koss You liked my comment but didn't reply lol. Now I'm even more curious. Should I buy more? Lol

English

@daniel_koss Please give me hope. I just plopped 10% of my portfolio into it on Thursday night after hours when it was down 5%.

English

@Sandeman52 Hey Sandeman, still just as bullish as before on NBIS, right? Nothing's changed? I put about 10% of my portfolio into it on Thursday night after I saw it dip 5% in AH. lol. Terrible timing on my part.

English

Rosanna has been nailing it all weekend.

Rosanna Prestia, MBA@RosannaInvests

My take: one high-volume down day tells you about emotion and sell algos, not direction and it’s resolved both ways historically. The more useful question is the catalyst. Friday sold off on hike fears from a jobs number that was mostly a World Cup one-off. The scare was noise; the selling was mechanical. That’s the real “will this time be different.”

English

@RingOfFireCGY That's an obnoxious amount to trade for the 1st overall. Calgary says no.

English

Who says no?

To Calgary

- 1st overall pick (Flames take Gavin McKenna)

To Toronto

- 6th overall pick

- VGK 2026 1st round pick (30 or 31)

- Four 2026 2nd round picks (35, 36, 51, 55)

- 3rd round pick (68)

English

@TheProfInvestor Don’t listen to him. He’s a paid account. Short $AMPX

English

@daniel_koss Perhaps putting the money into Daniel’s Autopilot would not turn a bad idea at all 👌🏻

English

New investors have a genuinely brutal problem right now:

The best stocks look like they already ran too far.

Just looking at the charts makes you feel like you are buying a generational top and will be a bagholder for the next decade.

I am not saying this is rational.

I am saying this is what many new investors write me in DMs.

So I will write a Substack article on how I would start investing if I were currently 100% cash and a totally new investor.

As a new investor, I think you honestly need at least one year to develop a feeling for how markets work.

You need to learn what makes stocks go up, what makes them go down, how earnings play into this, and what catalysts actually matter.

Then slowly increase your risk exposure after you have proved to yourself that you actually have a winning system.

Aping in in your first year of investing and expecting a great return is NOT the way to go and NOT what I can promise or offer here!

I think you need to give yourself time to learn and understand the mistakes and biases you have and make.

English

@Jackson59994888 @TheProfInvestor I just bought a bit. GL if you buy.

English

@daniel_koss Ohhh ok fair enough. Is autopilot an app? Got a link? I follow you on Substance but not autopilot.

English

@robbhope I no longer share it publicly, only to X Subscribers, but you can kinda cheat if you look at Autopilot 😂

English

YTD is now at +315%.

Return since 2024 just passed +3,000%.

May MVPs: $NBIS $DRAM $OUST.

Life-changing money.

These crazy numbers give me a lot of psychological safety to keep trading like an absolute madman.

It is nice to know that even if my portfolio crashed 90% tomorrow, I still would have done way better than if I had simply left my money in the bank and let inflation slowly eat it up every year.

English

Ouch.

I don't understand why anyone would short $NBIS

There are so many actually great shorts out there today.

Why pick one of the obvious winners at the heart of inference demand, the most parabolic growth chart in market history (that I know of)?

Jeremy M. Jacquin@jeremymjacquin

$NBIS Last year, Nebius stood out to me as a compelling undervalued pure-play AI infrastructure company, backed by tangible data center assets and meaningful GPU capacity. Hence the reason I accumulated 9,000 shares with a $39/share cost basis. Today, it trades as a highly speculative hype-driven stock, priced at unsustainable multiples based largely on unproven future promises rather than current fundamentals. The risk/reward profile has deteriorated sharply. Prudent investors may consider taking profits on their overexposure amid elevated valuation risk. I have now opened a short position worth $40k on the @leopoldasch pump at $225 and $230.

English

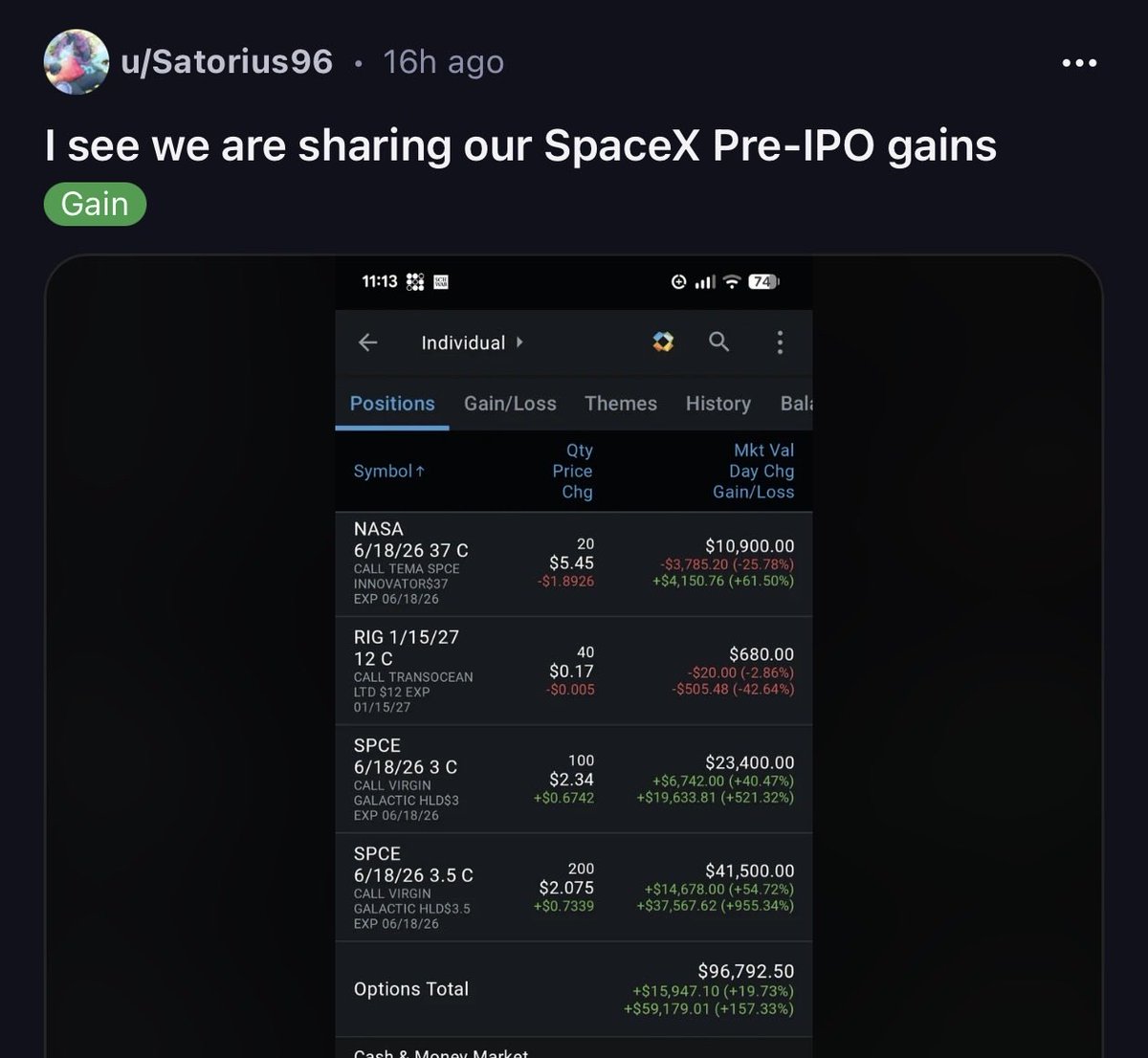

@vz921 @aleabitoreddit I think a ton of people are buying it simply because they expect retail to buy the wrong one on the IPO launch day. Including me. Zero actual interest in SPCX lol.

English

@aleabitoreddit Buying the wrong space ticker out of pure FOMO. If that’s not a sign of how much pent-up demand SPCX has, nothing is.

English

@DeepValueBagger yeah welcomed news after you called him a retard! 😂 not sure how your followers trust you

English

Just last week I pointed out he held many ai dc plays but not $nbis. This is welcomed news. I wonder if this really made the market move afterhours. I feel extremely lucky as i just removed the 10 covered calls i had on it this week.

Wall St Engine@wallstengine

Leopold Aschenbrenner's Situational Awareness LP disclosed beneficial ownership of 12.41M Class A shares of Nebius $NBIS, representing a 5.6% stake.

English

Wow, beautiful day for $CPSH!

Given the fundamentals, especially with the forced-flow from $NASA, this is still undervalued at ~$200M MC.

Nonetheless, tomorrow is a blank canvas. Will elaborate on the AlSiC angle in my thesis soon.

Wayne Liang@wliang

So I was deep diving into $NASA ETF holdings to see what will heavily benefit from $SPCX IPO... And I came across $CPSH. At the start of this year, it was a solid US AlSiC play, but quickly became a multi-thesis bet. As of last week, $NASA ETF holds ~1.8M shares of $CPSH (I immediately started a relatively large position). This is important because $NASA is the only pure-play space ETF with direct SpaceX exposure pre-IPO. And a portion of every dollar flowing into $NASA for SpaceX exposure becomes a purchase of $CPSH. As SpaceX IPO momentum builds toward June 12, that flow accelerates. But let's go over why $CPSH even made the cut into $NASA's portfolio. At the beginning of 2026: > It was the only meaningful US/Western hedge against East Asian AlSiC supply (Denka, Sumitomo, JFC, etc.) > Existing customers: US Military, NASA, $LMT, $RTX, Northrop, General Dynamics, and more > AI optionality as $NVDA Rubin generation scales towards multi-thousand watt requirements (this angle alone deserves a whole new post) And the foundation has only gotten stronger... > Record 2025 annual revenue of $32.6M and Q4 2025 revenue $8.2M vs $5.9M prior year (+39% YoY). Q4 gross margin recovered to 14.6% from a Q4 2024 gross loss > New $4M hermetic packaging order announced post-Q1 > Navy SBIR office extended Phase I program for Amphibious Combat Vehicles > Potential US Navy destroyer ballistic shield contracts with Congressional funding already secured Now add the $NASA ETF layer... Large asymmetry here.

English

@Limitless_LT @wliang Still like it even after crushing it today?

English

@aleabitoreddit Hey bro, can you stop pumping and misleading people? It's a real disservice. For example, what's your source for "US Army uses $CPSH for 40mm Tungsten Warheads"????

A $1 million RnD program does not mean the US Army uses CPSH for tungsten warheads.

English

I've initiated positions in $CPSH as a US AlSiC pure play chokepoint.

They represent ~25% of the near-term semi-grade AlSiC market.

Their customers:

- U.S. Navy (War)

- U.S. Army (War)

- U.S. Dept. of Energy (Energy / Nuclear)

- U.S. Space Force / NASA (Space)

- Lockheed Martin ( $LMT )

- Raytheon ( $RTX )

- Northrop Grumman

- General Dynamics

- The U.S. Navy uses $CPSH for ballistic protection systems of the newest carriers (like the USS Gerald R. Ford and USS Abraham Lincoln). As well as other fleets like the Danish Navy through Lockheed.

- US Army uses $CPSH for 40mm Tungsten Warheads and UH-60 Black Hawk Helicopters.

- The US Dpt of Energy uses $CPSH for impact limiters when transferring nuclear fuel (SNF) and high-level radioactive waste via rail.

- U.S. Space Force / NASA uses $CPSH for GPS satellites and it sits in many electronic systems in the International Space Station. (Also not including Mars Rover missions)

- Lockheed, Raytheon, Northrop, and General Dynamics uses $CPSH for missile heat-shielding components. AlSiC housings for radar systems, and thermal management materials.

AlSiC or (aluminum silicon carbide) is a well known material composite that handles extreme thermal conditions for many applications above from space to defense.

But as architectures from $NVDA Rubin to scale up to 2300-2500W in 2027-2028, that same material may be used AI due to heat warpage.

My thoughts were that the tiny TAM material used to handle extreme changes in heat from hypersonic missiles to rocket nose cones may likely be used for AI deployments.

This is similar to how InP (niche TAM for Telecom) became a bottleneck as photonics scaled up. Or how Toto's fine ceramics for toilets were critical to memory.

AlSiC (esp. post-processing) may become a potential chokepoint as AI ramps up to Rubin generation chips.

Majority of the world's AlSiC production still originates in East Asia (Denka,Sumitomo, BYD, JFC).

But CPS is currently the primary "US/Western hedge" and CPSH states they represent roughly 25% of the near-term available AlSiC market (CPS Technologies AGM Presentation).

And that percentage of the supply chain is only worth ~$100 MC right now.

Their balance sheet:

$12.7M – $13.8M (pro-forma) cash. Almost 0 debt. Inventory ~5.4M, Liabilities: ~$5.06M (eg. $3.53M for aluminum and silicon carbide)

Y/Y revenue is 8.8M, up +107.29%.

Y/Y Net income is up 207.96K (+119.94%).

Healthy balance sheet and US Government strategic interest + Defense Contractors gives $CPSH low downside risk at $100M or even at $200M as the leading Western AlSiC supply chain.

There were new contracts eg. $15.5M order from the leading Semi likely ~Infineon last October, that more visibility into revenue upside. And they are expanding production (funded by their Oct 25th raise), which hints to higher demand.

"We believe we are the world leader in the design and manufacture of AlSiC... Many of our products are designed specifically for a single customer application, making us the sole-source provider for those components." (10-K filings)

TLDR: The AI upside depends entirely on a material pivot by big tech. Similar to the Toto toilet maker for memory type but the AI fit seems strong.

But the benefit is that its existing list of US DoD contractors gives the company lower downside risk.

This is just my own personal thesis I wanted to share.

But personally I've taken positions in $CPSH as an AlSiC play (and long US supply chains) as it may play an important role with thermal warpage with AI in 2027-2028 as we expand to 2000W+.

Serenity@aleabitoreddit

Thermal is a likely issue for 2027-2028 GPUs: As thermal targets escalate toward the 2000-3000W+ range, copper and aluminum becomes insufficient. But, AlSiC, a metal matrix composite, may become important. Here's why: Rubin VR200 GPU pointed toward 1800W TDP, AMD Instinct MI450X, reportedly reaches up to 2500W, and $NVDA Rubin Ultra's power reportedtly goes to 2300W. The move toward 2300W creates a heat flux problem of massive scale. Aluminum Silicon Carbide (AlSiC) is a metal matrix composite, used as for defense, space, and high-power industrial applications (eg. high-speed rail). Similar to how random toilet companies like Toto became critical for HBM, this material composite used for thermal management for aerospace and industrial might be used for AI as it can survive tens of thousands of thermal cycles without delamination. So, as AI accelerators like Rubin reach power levels comparable to industrial power modules or space, the adoption of AlSiC in semiconductors may become important. For AlSiC in 2300W systems there's: - (Junction-to-Case): Includes the silicon die, the underfill, and the first layer of TIM - (Case-to-Sink): Includes the heat spreader (lid) and the second layer of TIM (TIM2) - (Sink-to-Ambient): The thermal resistance of the cold plate or liquid heat exchanger. Case-to-Sink is likely the application for AlSiC. And as power densities will likely continue to climb toward the 3000W mark there becomes a mechanical and thermal crisis that likely causes a material change from traditional copper packaging. So there's four different parts to this: 1. Internal/External Thermal It does look like SiC interposers (internal) are probably used for $NVDA Rubin gen GPUs. Then AlSiC (external) may be used for the Microchannel Lid (MLCP) or heat spreader that sits on top of the die interposer assembly. 2. 3D vertical stacking (SoIC) These complex packages are highly vulnerable to warping during thermal cycling. A SiC interposer is a brittle crystal and it cannot provide structural rigidity. AlSiC acts as a "stiffener" that prevents the substrate from bowing under the high clamping pressures 3. Rubin Ultra NVL576 rack likely reaches high KW of power density This density creates a weight-loading bottleneck that SiC interposers cannot solve. Rubin Ultra NVL576 rack cumulative weight of the thermal stack plus liquid manifolds can exceed the floor limits (and AlSiC may become necessary to reduce the "dead weight" of the thermal management by 60%+ without compromising heat transfer). 4. Net-Shape Manufacturing of Microchannels Traditional copper lids must be etched or CNC-machined, a process that has reportedly encountered high mass-production difficulty for Rubin volumes. AlSiC is manufactured using "Quickset Injection Molding" to create a ceramic preform that is then infiltrated with aluminum. This allows for the creation of complex internal geometries. AlSiC Microchannel Lids and Silicon Integrated IHS looks like the alternatives for copper for thermal management. We might be seeing this addressed earlier in 2026 as SemiAnalysis in 2025 reported that Nvidia’s Blackwell (B100/B200) faced yield issues specifically due to warpage in the CoWoS-L packaging. TLDR thermal is a likely a bottleneck in 2027-2028: Some beneficiaries are potentially SiC interposers (high-purity SiC powder) and AlSiC composite for thermal management in 2027-2028. This is all ongoing research, but maybe we'll see some extremely niche and random small railway or space AlSiC supplier be used up for AI in 1-2 years time like toilet makers for HBM.

English

@Fibonacci_TA I use Reddit every day and I want nothing to do with FB or Meta. Fwiw.

English

Upped my $RDDT position by 50% today, it's now a 7.5% position of my total portfolio — so for the quick math guys, it used to be 5% and I upped it today by 50%.

Anyway, Facebook is going to murder that platform so that is always a great catalyst.

Fibby.@Fibonacci_TA

I bought $RDDT on Friday. I mean, they will surely get disrupted by Meta, so that seems like a solid way to lose some money.

English