Sabitlenmiş Tweet

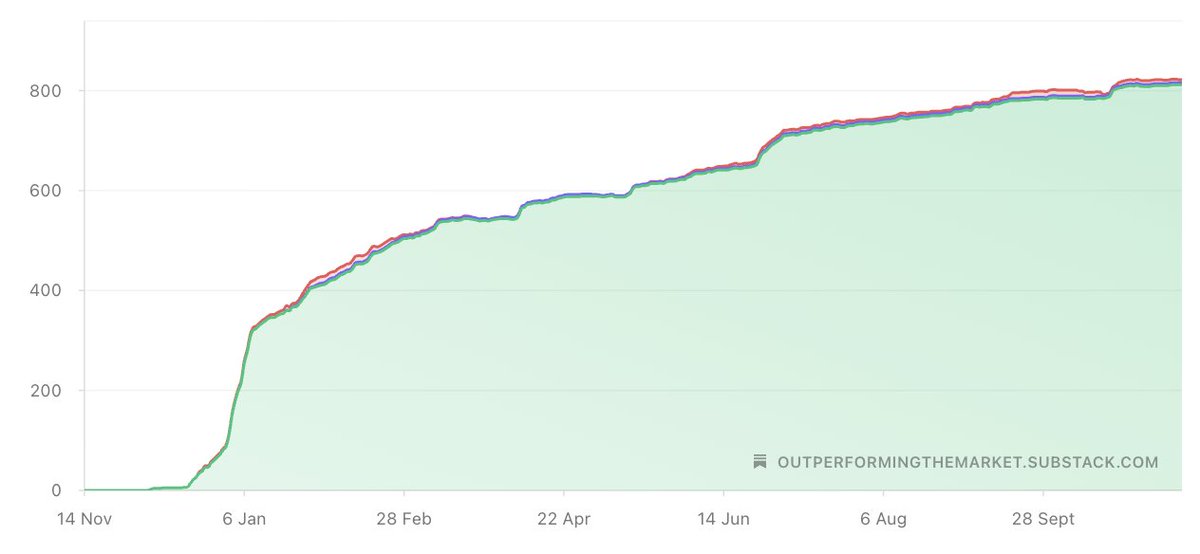

It's slightly less than 1 year since starting Outperforming the Market on SS.

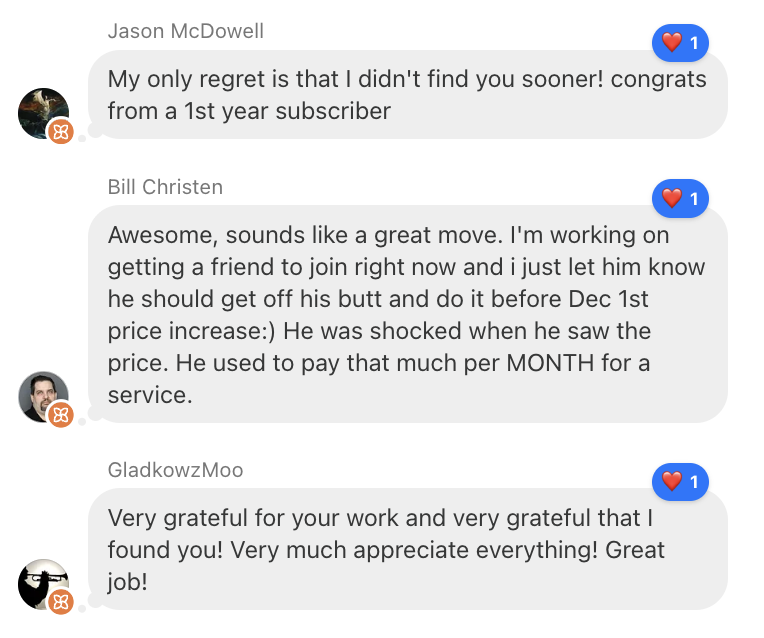

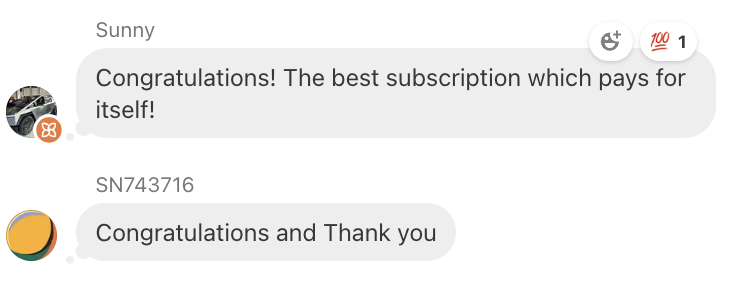

The response has been phenomenal and I sincerely thank you all.

As earlier communicated with subs, I have made the decision to keep the service small to maintain the quality.

Starting 1 Dec 25, I have decided to raise the annual plan from $320/yr to $400/yr.

If you subscribed before 1 Dec, your $320/year or lower plan will be grandfathered and not affected by the price increase.

Thank you all once again for the support and I look forward to helping you to continue to outperform the market.

English