TickerLeague.com

17 posts

TickerLeague.com

@tickerleague

Competitive Financial Markets Games Test your financial markets knowledge in skill-based games. Predict metrics, compare fundamentals, and climb global leaderbo

Katılım Ocak 2026

23 Takip Edilen4 Takipçiler

@dividendology That's why a solid ETF like $VOO is so safe during market times like this.

English

MAG7 returns year-to-date:

🤖 $NVDA: -1.28%

🔎 $GOOG: -3.6%

👥 $META: -5.47%

🍎 $AAPL: -7.17%

📦 $AMZN: -9.48%

⚡ $TSLA: -11.69%

🪟 $MSFT: -17.58%

Every single MAG7 stock is down.

English

The story of Ronald Read really is insane.

Born in 1921, Read lived one of the simplest lives you can imagine.

He was a janitor and and worked as a gas station. To everyone around him, he looked like an ordinary, hardworking man with modest means.

But he had a secret.

Over the course of several decades, Ronald Read quietly built an $8 million fortune.

How?

• He lived frugally

• He saved consistently

• He invested in high-quality, dividend-paying stocks

And most importantly… he held them for decades His portfolio included companies like Johnson & Johnson, Procter & Gamble, JPMorgan, and Dow Chemical.

These were blue-chip businesses that steadily grew and paid dividends year after year.

Read rarely sold anything. He simply let the power of compounding do the heavy lifting.

When he passed away in 2014 at age 92, the town was stunned.

Ronald Read donated $6 million to the local hospital and $2 million to the public library.

Nobody had any idea he had accumulated that kind of wealth. His story is one of the best real-world examples of what long-term investing can do, even for someone who never earned a high income.

Ronald Read proved that you don’t need a big salary to become wealthy.

You need time, patience, discipline, and the willingness to let compounding work its magic.

Most people look at this story and point out that he never 'got to enjoy his wealth'-

And to a degree that is true.

However, the deeper meaning behind this story is this:

Anyone can build wealth when you let compounding work for you.

English

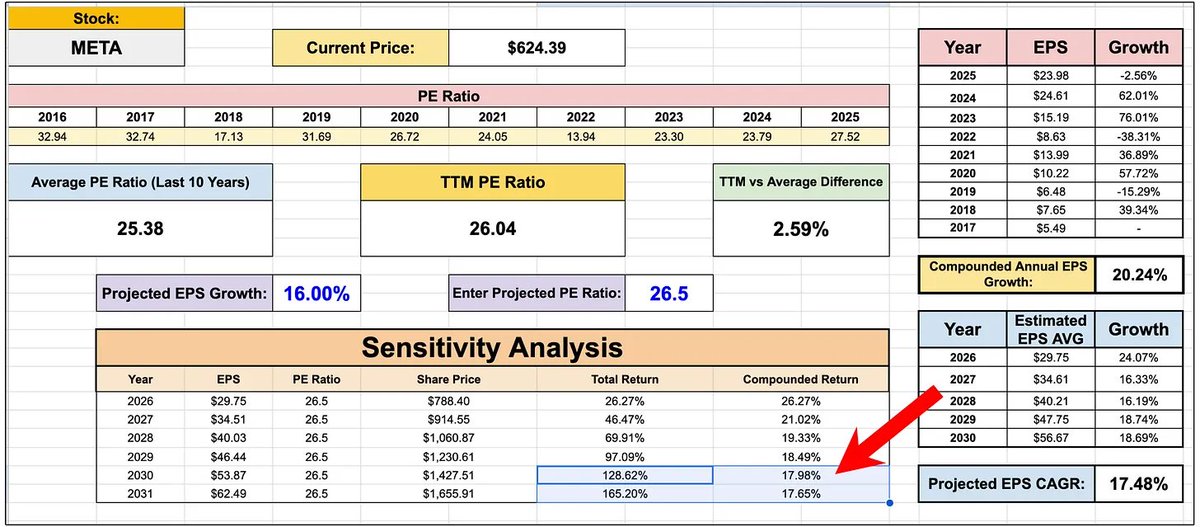

Despite being one of the most dominant technology companies in the world, the stock has been relatively flat recently.

Every Mag7 stock is currently down year to date, with $META currently down slightly over 8%.

The company’s core business remains extremely straightforward:

Digital advertising.

Roughly 99% of Meta’s revenue comes from advertising across platforms like:

- Facebook

- Instagram

- WhatsApp

Historically, this business has compounded at extraordinary rates.

Over the past decade, Meta grew revenue from roughly $17.9 billion in 2015 to more than $200 billion in 2025, representing a 10-year revenue CAGR of about 27%.

The company also operates an extremely efficient business model, with relatively low leverage and consistently strong returns on invested capital, often approaching or exceeding 20%.

What makes Meta particularly interesting today is its valuation.

The stock currently trades at a forward P/E ratio of about 20.3, which is actually slightly cheaper than the S&P 500, which recently traded at roughly 22x forward earnings.

In other words, investors can buy Meta, a company expected to grow far faster than the overall market, at a valuation below the market average.

According to analyst estimates, Meta’s projected EPS growth over the next 3–5 years is around 22.4% annually.

This combination of strong expected earnings growth and a market-level valuation is one of the main reasons analysts remain highly bullish.

The average Wall Street price target currently sits around $858, implying roughly 34% upside from current prices.

It isn’t just analysts who are paying attention either.

Hedge fund manager Bill Ackman recently initiated a position in Meta, making it over 11% of his portfolio.

More broadly, Meta is also the 6th most widely owned stock among “super investors” (investors managing over $100 million in assets).

Looking ahead, Meta still has several powerful growth drivers.

Revenue growth is largely determined by three factors:

1. Daily active users

2. Ad impressions

3. Average price per ad

In Meta’s most recent results, all three metrics moved in the right direction. Daily active users grew 7% year-over-year, ad impressions increased 18%, and the average price per ad rose between 6% and 9%.

The main concern investors have today is Meta’s rising capital expenditures, largely driven by the company’s aggressive investment in AI infrastructure.

However, the path to monetizing this capex spending is more clear than some of their big tech peers.

AI could ultimately strengthen Meta’s advertising engine by improving ad targeting, increasing engagement, and raising the price advertisers are willing to pay.

Meta also recently introduced a dividend, though the yield remains small at roughly 0.3%.

With a payout ratio of only about 11% of free cash flow, the company has substantial room for dividend growth in the years ahead.

Even using conservative assumptions, Meta appears capable of delivering market-beating returns, which is why many analysts continue to view the stock as one of the most attractive opportunities among large-cap tech today.

English

$MU Further Breakdown

Financials 📊

🔷 Revenue: $23.86B (+196.4% YoY) (+75% Q/Q)

🔷 EPS: $12.20 (+682.1% YoY)

🔷 Gross Margins: 75% (+3,700 bps)

Q3 2026 Guidance:

🔷 Revenue: $33.5B (+260.2% YoY)

🔷 EPS: $19.15 (+902.6% YoY)

📌 $MU absolutely shattered earnings expectations as demand for their memory required for AI compute chips is off the charts. The company still trades absurdly cheap at a forward P/E under 10, which is ridiculous for its growth rate. Historically a cyclical memory producer, it has been treated as cyclical, and the market is pricing in a downturn. But data center demand appears to have changed that. It is absurd that the company is up 353% YoY and still looks like a bargain.

Quality Compounders@QualCompounders

$MU fiscal Q2 2026 earnings are out: 🚨 Financials: ✅Revenue actual: $23.86B – estimate: $19.19B ✅EPS actual: $12.20 – estimate: $8.79 Q3 2026 guidance: ✅Revenue: $32.75B – $34.25B – $22.53B estimate ✅EPS: $18.75 – $19.55 (midpoint: $19.15) – $10.57 estimate Highlights: 💡 🎯 Record-Breaking Quarter: Micron set all-time records for revenue, gross margin, EPS, and free cash flow this quarter, driven by the insatiable demand for AI memory. 🎯 HBM Sold Out: Management confirmed their entire High-Bandwidth Memory (HBM) production capacity for the remainder of the 2026 calendar year is already 100% sold out under binding agreements. 🎯 AI Asset Status: CEO Sanjay Mehrotra stated that in the AI era, memory has become a "strategic asset," leading the board to approve a 30% increase in the quarterly dividend.

English

@QualCompounders I have $TSM, $META, $AMZN from the list :)

English

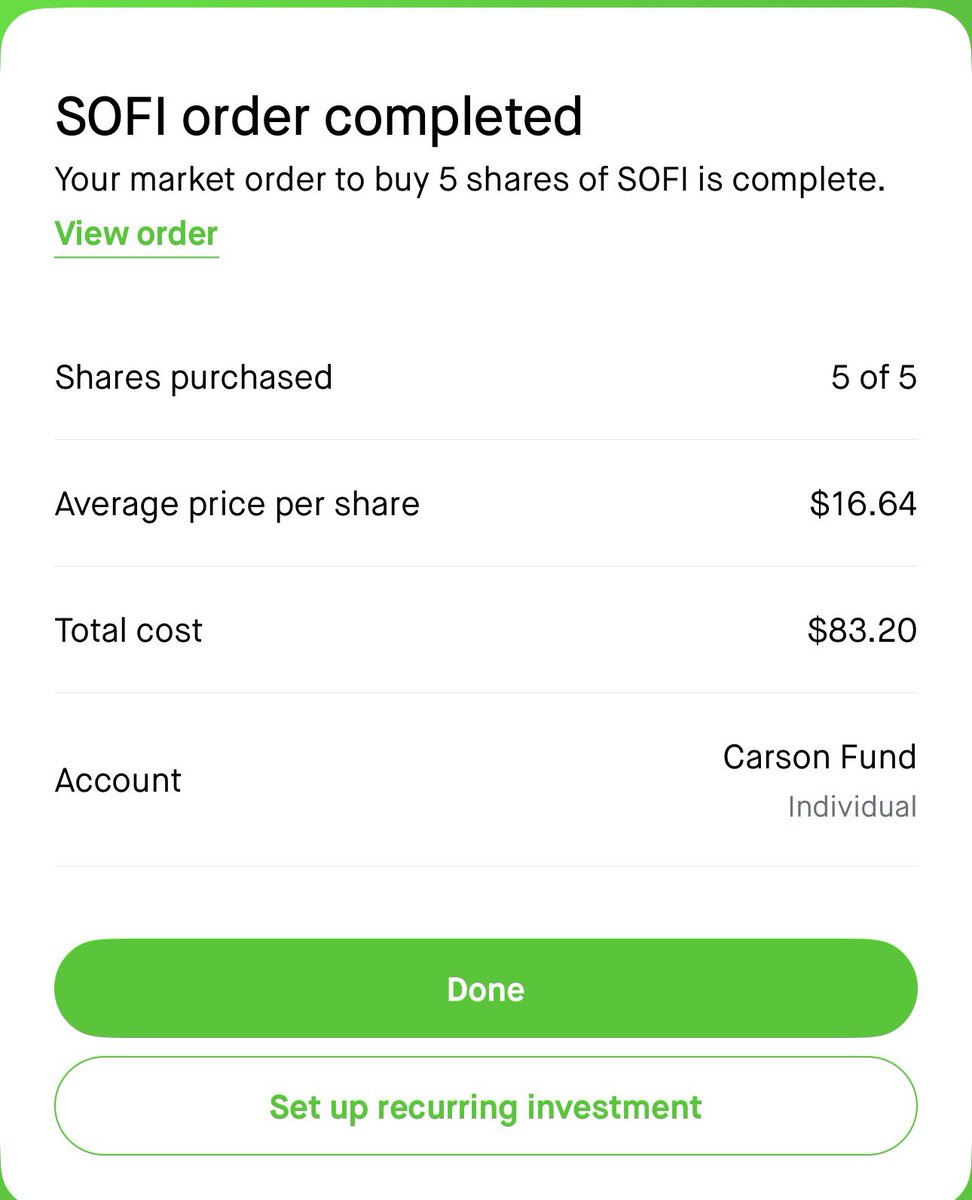

5 Stocks to buy and hold for the next Decade:

1. $TSM

2. $META

3. $AMZN

4. $SOFI

3. $AMD

Let's get into it see the thread below. 👇🧵

English

🚀 New TickerLeague Poll!

In 2026, which of these 4 IPO giants would you buy stock in? Vote below 👇

Which company do you think will moon the hardest?

Drop your pick + why in the comments! 🔥

#IPO2026 #SpaceX #OpenAI #Databricks #Anthropic #Stocks

English

$1,000 in NVIDIA would be $219,357.98 today (+21,836%). Would you have held?

Calculate yours: tickerleague.com/companies/NVDA… #nvda #lifechanging #stock #whatifinvested #tickerleague

English

🌍 Did you know? Meta's revenue exceeds the GDP of Ukraine (#58 economy)! Check it out: tickerleague.com/companies/META… #meta #stock

English

$1,000 in Home Depot at IPO would be $16,860,870.94 today (+1,685,987%). Would you have held?

Calculate yours: tickerleague.com/companies/HD/w… #StockSelection #IPO #LongTermInvesting

English

📈 If I had invested $10,000 in Adobe on 2021-03-19, it would be worth $5,757.64 today (-42.42%)! Check it out: tickerleague.com/companies/ADBE… #adbe #adobe

English

📈 If I had invested $1,000 in Duolingo on 2021-07-28, it would be worth $777.33 today (-22.27%)! Check it out: tickerleague.com/companies/DUOL… #duol #duolingo

English

📈 NVIDIA makes $3.81K per second in profit! Check it out: tickerleague.com/companies/NVDA… #stocks #nvda

English

See how Alphabet (GOOGL) makes money — visual revenue breakdown and profit margins. tickerleague.com/companies/GOOG… #GOOGL #stocks

English