Vanderlane

257 posts

Vanderlane

@vander_lane

Investing in US small caps within the AI application layer.

Amsterdam Katılım Nisan 2017

454 Takip Edilen88 Takipçiler

$DLO remains a +$35 company trading at $11.

When you have conservative assumptions getting you to those kind of profit gains then you know you can have a lot of confidence in a position.

Even if I take my conservative assumptions through to 2030 and cut it by 50%, we're in for almost a double from here.

Still long $DLO after this quarter.

Oliver | MMMT Wealth (CPA)@MMMTwealth

I was drafting my $DLO thoughts and then I saw @realroseceline post below. Most of it I couldn't say better myself so I'm quoting it here. Big picture it's really as simple as this: The margins were ugly yes in this quarter yes (mostly temporary). But you've got a $3.2 billion dollar company going after a HUGE TAM. It has TPV growing 73% YoY (that itself is super rare). I don't know about you but with the greenspace ahead, as an investor I'd be frustrated if management weren't investing heavily into growth at this stage? This is a company with huge potential across many avenues. Management are going for it. If that means a short-term struggle on margins then fine by me. Long $DLO

English

@ValerijDaniloff @Neil_X10 @PaperBagInvest Yes but how does this work with a cat or a house insurance. Just saying, client related datapoints still need to be captured.

English

Not necessarily. Tesla FSD product already proves the model. Lem does not need an app install to capture driving data.

They connect directly through Tesla fleet API.

The car sends the data.

The customer just gives permission once.

As more manufacturers open their API the same model scales. Your car, your home sensors, your phone already generate the data.

Lem just needs the permission layer and the API connection.

The app becomes optional not required.

And in an agentic world the agent handles the permission flow on your behalf. One setup, then it runs in the background forever.

That is actually fewer friction points than downloading an app today.

English

🍋

Here is what I think is the most underrated $LMND thesis and nobody is talking about it.

Shai tweeted last week that LoCo, Lemonade insurance OS, is practically heaven for AI agents.

More on this at Investor Day he said.

That one sentence deserves a lot more attention than it got.

Today Lem sells insurance directly to consumers.

One customer at a time.

CAC per customer, premium per customer, LTV per customer.

That is a great business. But it is still a linear business.

Now imagine LoCo opens as an API for external AI agents.

An AWS bBedrock agent, a Circle agent, or an AI financial advisor calls the LoCo API and buys insurance on behalf of a user.

Lem earns a margin per policy.

They own the distribution infrastructure but do not need to own the customer relationship directly.

Lem becomes the route all agentic insurance has to flow through.

Think about the Stripe analogy. Stripe does not sell products. They are the payment infrastructure other companies sell products through.

Stripe is used by millions of businesses all paying a small margin per transaction.

Stripe does not need to hire to grow.

They grow with the volume of the internet.

Lem can become Stripe for insurance.

I also think they launch their own AI agent that actively buys, manages and adjusts insurance autonomously on behalf of a user.

The agent monitors life changes.

New car. New home. New pet.

It updates your policy automatically.

This is not something you call. It is something that just happens in the background.

The math on this is straightforward.

The US alone has 290 million cars, 140 million homes and 90 million pets.

That is a 500 billion dollar market. If AI agents start managing insurance autonomously for even 10% of that market via LoCo, that is 50 billion in premium volume potentially flowing through Lem infrastructure.

AWS already has millions of enterprise customers. If even 0.1% of them build AI agents that need insurance infrastructure and choose LoCo, that is thousands of agents generating policies daily without Lem spending a dollar on CAC.

And the biggest upside is not even the premium volume.

It is the data.

Every agent that buys insurance through LoCo gives Lem more data.

More data gives better risk models.

Better risk models give lower loss ratios.

Lower loss ratios create room for lower prices.

Lower prices attract more AI agents.

And the flywheel spins faster and faster.

Today the market prices Lem as an insurance company at a 4.2 billion mcap.

A company that is insurance infrastructure for the agentic economy gets priced like tech infrastructure.

It requires AI agents to actually adopt agentic commerce at scale, LoCo to open as a platform, and Lem to execute on Investor Day in November.

But Shais tweet suggests the direction imo.

And the Clarity Act passing this week makes agentic commerce legally possible for the first time.

You might not just own an insurance company.

You might own the foundation of the next generation of insurance infrastructure.

And the market has absolutely no idea yet.

Shai Wininger@shai_wininger

LoCo, @Lemonade_Inc's insurance OS, is great for humans, but it's practically heaven for (ai) agents. More on this at Investor Day...

English

@ValerijDaniloff It would still require an app install or agent that captures the data and sends it through.

I did not think of his tweet this way, but its indeed super interesting and I hope they go this way. Curious to hear the opinions of others on this! @Neil_X10 @PaperBagInvest ?

English

You dont need to own the client to own the data.

Lem still underwrites the policy. They still pay the claim. Every mile driven, every claim filed, every renewal flows back into their models regardless of who distributed the policy.

The agent is just the channel.

Lem is the infrastructure underneath.

And paradoxically an AI agent that automatically updates your policy when you buy a new car probably gives Lem better and more timely risk data than a human customer who forgets to call in the change.

English

@chrisstlmo @vander_lane That’s fair

My personal rule for these small cap spec names is the 200 wma is always in play

Right now that’s at $30

I consider Lmnd a higher tier spec name because the execution has been amazing. So I don’t see it below $30

Just so you don’t think I’m making numbers up.

English

I honestly don't understand why $LMND is still trading around $50-60. Is the market not seeing what we are seeing or is everyone chasing chip stocks?

English

@KrishnaY152841 @BastianelliLore Combined ratio incl growth spent was 115% for 26Q1, not?

English

@vander_lane @BastianelliLore $LMND headwinds are ~138 Combined Ratio, Isreal war and performance allotment of stock to founders at approximately $115 just for a mere 30 trading days

English

@BastianelliLore I agree, its my largest position by far. But the stock performance has been quite week the last 4 months.

English

@vander_lane Push harder profitability? I prefer they prioritize growth honestly.. they need scale, high margins can wait. $LMND is a 10 years or more growth story, they’ll be the biggest insurer, let’s give them time to cook 🧑🍳

English

@MMMTwealth @MMMTwealth what is your take on $TMDX 26Q1 figures and the sell off? Saw you continue to DCA into this name.

English

Three key positions for me report after the close today:

1. $ZETA: Far too cheap at 10.2x EBITDA whilst growing EBITDA at 40%. Another beat and raise quarter incoming most likely.

2. $TMDX: Q4 flight data was very strong...that's not everything anymore but it paints a nice picture. Expecting a Q4 beat and a raise in guidance. Still trades at just 27x NTM EBITDA for an expected 28% EBITDA growth.

3. $SEI: Has consistently beat on revenue for the last 5 quarters. Analysts expect $164.1M in revenue in Q4 25 which would be a 68% increase from Q4 24....trades at just 4.6x NTM sales.

English

@BastianelliLore However, once $LMND goes up, it will go up harder than $ROOT, as it has better quality revenues.

English

@BastianelliLore It will take roughly until early 2029 before $LMND will post similar Net income figures as $ROOT did in 26Q1. Different model, but 3 years is a long time. I think $LMND could and should push harder.

English

@bradsferguson @Jaktier1 I believe they could grow a lot faster than they do now if they could deploy more capital, but I agree they are not constrained for the current growth trajectory. So yes, this depends on how you look at it.

English

@vander_lane @Jaktier1 They are not capital constrained. We just asked management directly about it.

English

Did $LMND just roll out it’s third state for renters in ~ a week? Yes they did.

They accelerate growth even without state expansion and this is definitely pushing the numbers further.

Glad to be a long term investor, we are just in the beginning.

English

@Jaktier1 You must see $LMNDs system as a perfect capital allocator. You put in $1 and it makes $3 or even $4 over time. They are active in many markets, so they just optimize for the best possible LTVCAC. As soon as they turn profitable, a positive flywheel will come into place.

English

@vander_lane You are right. What’s your opinion on the growth rate with that in mind?

I would argue that the larger TAM addressed with more states will do its work anyway (organic growth)

English

It's hilarious to see so many people dunking on real estate. Three years from now they will wish they converted some of their stock portfolio into a down payment in 2026.

Kalshi@Kalshi

JUST IN: US home sellers now outnumber buyers by 630,000 — largest gap ever.

English

@jakebrowatzke @vishal_better Where to start @jakebrowatzke when looking into Better? Top 5 sources you would recommend ?

English

Love seeing founders such as @vishal_better buying more of their shares with their own money as the market panics

Here's the bottom line in my opinion regarding $BETR's Q1:

1) a product (Tinman) now representing 50% of total volume grew 400% year over year in Q1. There is no question about whether or not we have found substantial product-market fit. This product is just getting started.

2) despite the disappointing guide for Q2, it was confirmed that Tinman top-of-funnel volume doubled in the month of April alone. And while we won't see the payoff of this immediately due to rates increasing recently on Better's platform reducing conversion rates and somewhat counteracting the top-of-funnel growth, we'll still grow in the mid-20% to 40% range year over year in Q2 even before rates come back down. Despite tightening financial conditions Better is able to grow through it, guiding for 15% sequential growth in revenue from Q1 to Q2. I cannot stress enough what this signals for the growth ahead. There will be substantial volume growth as financial conditions begin to loosen and we now have double, triple or even fours times the top of funnel volume as the Better of 2025. In my opinion easing financial conditions are a matter of when, not if, thanks to AI being the biggest deflationary force in the history of humanity, and the incoming fed chair Kevin Walsh understanding this.

3) stock-based compensation only vests if substantial gains are made in both Bettors' stock price and in Tinman's revenue, with two tranches of vesting. We are not being deluded as shareholders without reason or payoff and we won't even see much of the stock-based compensation that appeared in the Q1 earnings report unless the stock hits $90 per share and Tinman has passes a $300 million annual revenue run rate. That makes the increase in stock-based compensation a much smaller deal in my opinion. In fact I view it as a positive. As long as this compensation is tied to out-performance compared to the industry, substantial out-performance even, I'm a fan.

You have to spend money to make money, keep paying your best players in order to build a dynasty, and I'm excited because Better.com's time of making money, and then substantial money, is right around the corner.

The continuous insider buying doesn't hurt my conviction either.

Average Insider@AvgInsider

🚨 $BETR Insider Buy Garg Vishal (Director) bought 6,583 shares ($197.49K) May 7 | Price: $30.52 52W: $10.81–$94.06 averageinsider.com/accession/0001…

English

@goddreng10 @HenryInvests @davegirouard @paulxgu Where to start when diving deep in $UPST ? Any good accounts you would recommend?

English

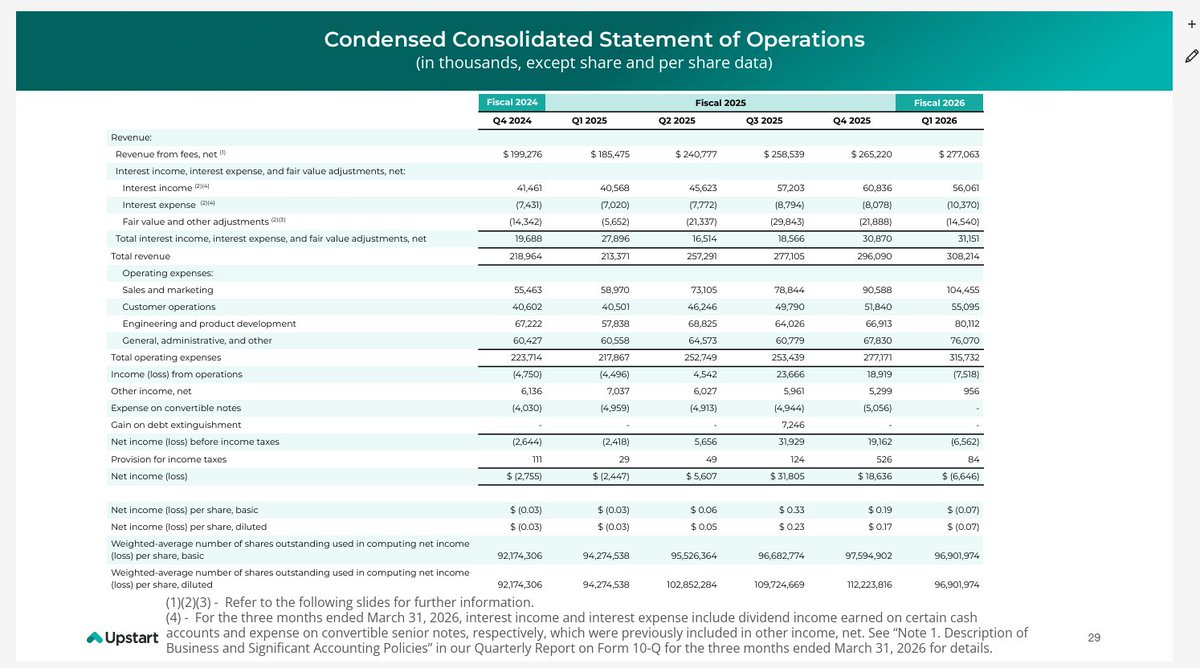

$UPST

Q1 25

Revenue: $213M

OPEX: $217M

Q1 26

Revenue: $308M

OPEX: $315M

45% rev growth and 45% OPEX growth - where is the operating leverage? $UPST needs a firing round and focus on cost cuts. Sell BS loans and BB 10% of shares.

@HenryInvests @davegirouard @paulxgu

English

@Neil_X10 @petermasica Im in the same position. Feel I understand $LMND completely. Also all-in with size and comfortable sleeping at night because I know FV is >$150. Its like watching paint dry.

English

For all intents and purposes, I'm all-in.

With my experience in financial markets / this being right in my wheelhouse, at this point it makes sense not to diversify, and I may actually hurt myself chasing something I don't fully comprehend.

We're still like 4x undervalued. I'll continue building out my position as long as we're this far from fair value.

English

Why $LMND seems so boring at times ...

shirish@shiri_shh

$25,000 in Sandisk 1 year ago is $1,039,000 today.

English

It feels a bit like the momentum in the stock is gone. Are we really just waiting for Q3 and Q4 to see some fireworks again?

English

@PaperBagInvest Likely impacted by lower CPMs this quarter and the Elon push (FSD product release). But anything above 3x is great really at this scale.

English

But seriously, look at where 2026 Q1 is on this graph of Trailing-12-Month LTV/CAC vs Growth Spend 🍋 $LMND

English