Sabitlenmiş Tweet

matze | growthepie 🥧

2.7K posts

matze | growthepie 🥧

@web3_data

Data-driven takes on the Ethereum Ecosystem | Co-Founder @growthepie_eth & @open_labels | Building dashboards, calisthenics, and walking our dog 🐶

Berlin, Germany Katılım Ocak 2022

1.1K Takip Edilen2.2K Takipçiler

English

@web3_data @RobinhoodApp @growthepie_eth let's hope that the streak of successful L2 launches continues and that there will be many more to come

Robinhood has the potential to serve as a role model for many in this field

English

Stablecoin supply on @RobinhoodApp chain is currently sitting at $327M - after only 12 days of being live.

This is the fastest growth trajectory that we've seen so far.

English

@web3_data Yes he just did. Can only imagine he wrote something he believed and then legal/politics had him take it down

English

This post is from the heart, motivated by Brian Chesky's bullpost last night. We're so close now.

It's been 3 years since I wrote the below essay explaining precisely how Ethereum reduces friction to enable bringing the global economy onchain and enhance productivity. It got 540 likes which is pretty good for an account my size. It was my pinned post for years.

Last night, Brian Chesky (Airbnb Founder & CEO) became the most famous, successful, and high status trad tech CEO to finally say the quietest part out loud:

The most special thing about public chains is friction reduction.

In doing so, Brian effectively endorsed Robinhood L2 and Eth's whole L1+2 model.

I have been a big fan of the podcast EconTalk for my whole adult life and of its most frequent guest Mike Munger. This gave me early exposure to the theory of friction which economists refer to as "transaction costs"... not to be confused with gas fees. It helped me see the global friction reduction benefits of eth, which I have been writing about since 2019. That being said-

During these early years, the world's onchain adoption has had and will have 3 distinct phases.

Phase 1: Admitting the tech is pretty great. We saw this gradually ramp up from 2017-2024 in the form of early failed private blockchains, early institutional discussions and uptake of programmability, etc.

Phase 1 is about institutions, corps, governments, central banks, and silicon valley recognizing that our onchain tech (almost always EVM) is a 1000x improvement to their offchain systems.

Phase 2: Admitting that public chains are special networks. This started approximately with Facebook's Libra and has exploded after GENIUS, with the launch of many new corpo L1s.

Phase 2 is characterized by trad folks all agreeing with each other and aping into the fact that public chains embody "come for the tech, stay for the market". The growth of international tbill demand from stablecoins played a key role in this.

Brian's post has taken us to the bottom of the 8th inning here today in Phase 2. What happens next is Phase 3. That's where we win.

Phase 3: admitting that the additional friction reduction-- above and beyond EVM tech and just any public chain-- from the Ethereum L1's decentralization and the L1 being the hub for defi/L2s is extremely valuable at global scale, and not available anywhere else.

Phase 3 is where the world collectively realizes that the Ethereum L1 has a monopoly on being maximally decentralized and on being the global defi/L2 hub with the deepest liquidity, and also realizes that the world desperately needs this, or else the global economy literally can't come onchain.

It's too risky and inconvenient to bring trillions in assets/activity onchain without Eth L1+L2.

Skipping going onchain is not an option, specifically because the world wants to capture all of the magical apps/UX/markets uniquely enabled by Ethereum. Ethereum is inevitable.

Friends... fellow Ethereum and ETH lovers and holders... it has been a long and frankly brutal road.

As of today, we have never been closer and more certain to the realization of the incredible outcomes that used to merely exist in our dreams.

We are near the end of the beginning.

In the coming quarters and years, the world will enter Phase 3 of early adoption and hit the ramp of the global adoption S-curve. The entire world will realize that not only do they need to be onchain, but they need to be onchain on Ethereum L1+L2, where the friction/risk are lowest, protocols are strongest, and liquidity is deepest.

Ethereum will achieve its potential to provide a level economic playing field for all of humanity.

ETH will achieve its potential as a global treasury-grade SoV.

Both will dominate for decades, maybe centuries.

From the heart- love all of you that have been on this journey together for so long. And a huge welcome to everyone joining us now.

The best is truly yet to come. So close now.❤️🚀

⟠@ryanberckmans

For any person in the world, the goods & services accessible by them are determined by the extent of their trade network. A larger trade network increases capacity for specialization, resulting in new goods & services and making existing goods & services better and cheaper. The size of a person's trade network depends on the total friction of their individual circumstances. Economists refer to this friction as "aggregate transaction costs". They use a much wider definition of "transaction cost" than, for example, a gas fee. Any kind of added friction cost whatsoever reduces the size of a person's trade network, and that reduces the quality, affordability, and variety of their available goods & services. Costs of all kinds play a role in determining the extent of a person's trade network: Does the person live in a city or on a farm? Is their city separated from neighboring cities by a mountain range or a flat highway? What regulations or taxes exist to restrict or enable commerce? Are there any wars, famine, natural disasters, or other circumstances? Does their country have good physical infrastructure? All types of costs and friction play a role. How does a person's trade network move information? Do they rely on wagon loads of clay tablets hauled by oxen to move information, as was done in some ancient civilizations? Do they use morse code telegraph lines? Or, do they have digital information transfer, ie. the internet? Is the same information transfer technology available everywhere in their trade network? How does their trade network move goods? Do they haul wagons of wheat on dirt-packed roads? Or, do they have a modern network of vehicles and highways, of ships and shipping lanes? What loss of goods occurs during transit? To disasters? To theft? Perishable? What technologies and systems work to prevent these losses? Political systems? Security cameras and national ID databases? Is the level of risk similar throughout the trade network, or are some parts safer than others? How does a person's trade network move money? Do they pass around IOUs by messengers on horseback? Do they pass around digital IOUs in a rigid banking federation based on privilege and relationships (web2 finance)? Or, do they have a global internet financial system that's an open access level playing field and lets you "hand cash" to anyone in the world (web3)? Jason asks, "How does web3 improve economic output?" The answer is that economic output depends on the quality, affordability, and variety of goods & services available to each person, and this depends on that person's unique vantage point into the global trade network, and that depends on each person's trade network's aggregate transaction costs, and these transactions costs are greatly reduced by web3. Web3 - reduces information transfer transaction costs (secure open data for prices, markets, etc) - reduces money transfer transaction costs (bearer ownership, instant settlement, etc) - decentralization reduces risk which further reduces transaction costs. Example: erc20 transfer on BSC vs Eth L1, both are the same token transfer, but the one on Eth has much lower risk because BSC is centralized. That lower risk is a type of transaction cost reduction. - public chains are global and open-access, so these beneficial reductions in transaction costs can apply to everyone in the world's unique vantage point into the global trade network. Web3 helps everyone, not just people in wealthy countries. Every major benefit of web3 tends to reduce transaction costs: ERC standards, public composability, trustless bridging among L2s, censorship resistance, strong property rights, open innovation, etc. In short, web3 increases economic output by reducing friction costs that limit the extent of the global trade network and therefore growing the quality, affordability, and variety of goods & services available to everyone in the world.

English

@CryptoProphet15 @growthepie_eth x.com/barnabemonnot/…

- Faster slots on L1

- Faster finality for L2s

- Better interop between L1/L2

-> more demand for L1 block and blob space

->> higher revenue for Ethereum

Barnabé Monnot | barnabé.eth@barnabemonnot

We may disagree on whether it is sensible to offer Ethereum security at cost, as a growth lever vs a revenue play. But we should not disagree that the value of blockspace should increase, to make the network as a whole, with ETH at its centre, more valuable. As long as scale is sufficiently addressed, this both supercharges growth and raises the revenue floor. For L1: Faster slots. For L2s: Faster finality. For L1 & L2s: Better interop.

English

@web3_data @growthepie_eth Thanks for the reply. Do you think glamsterdam will lead to more fees paid to ETH over time? What is the best way to get significantly more revenue for ethereum

English

matze | growthepie 🥧 retweetledi

You've underrepresented Robinhood's rent paid to Ethereum by a factor of 4x because you used Arbitrum's rent paid.

0.6% of revenue is the correct figure for Robinhood Chain. With the current low price of blobs, 98.5% of that goes to L1 settlement... You may still want this to be higher, but at least you can now reference the correct figures.

See for yourself: growthepie.com/economics

Lorenzo Valente@LorenzoARK

The Robinhood Chain is the cleanest case study of what happened to ETH's economics over time. Since inception, @RobinhoodApp Chain has grossed ~$816K in revenue. @Arbitrum, the middleware provider, takes 10%: ~$80K. Arbitrum then pays Ethereum for settlement: $1,538. The margin profile roughly: Robinhood: 89% Arbitrum: 10% Ethereum: 0.15% If your thesis is "ETH is money," Robinhood building here is ultra bullish. More activity, more ETH collateral, more lindyness. If your thesis is "ETH is a revenue generating asset," this is the ultra-bear case. And here's the uncomfortable truth: Robinhood was never going to build on Solana, Sui or any monolithic L1. They want the stack customization. They want to be landlords, not renters. Ethereum won this deal on merit. It's just not pricing it right. A healthy split to me looks more like: Robinhood: 75% Arbitrum: 10% Ethereum: 15% Ethereum sells the most valuable settlement layer in crypto at marginal cost. Things need to change. @ethlabs_org

English

@CryptoProphet15 @growthepie_eth Base has a slightly better margin at the moment, yes. Probably because of higher priority fees (users paying more for a tx).

English

@growthepie_eth @web3_data Why is base only .3% am I reading that correctly

English

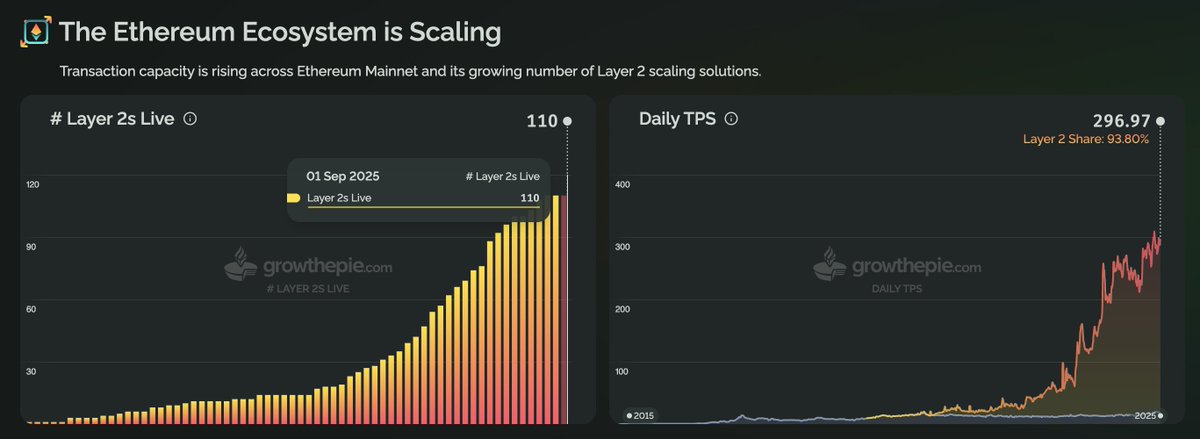

In the last 7 days, @RobinhoodApp:

- generated the highest amount in gas fees out of all L2s with $801,000

- was the highest rent-paying L2 with $4,400

growthepie 🥧📏@growthepie_eth

You've underrepresented Robinhood's rent paid to Ethereum by a factor of 4x because you used Arbitrum's rent paid. 0.6% of revenue is the correct figure for Robinhood Chain. With the current low price of blobs, 98.5% of that goes to L1 settlement... You may still want this to be higher, but at least you can now reference the correct figures. See for yourself: growthepie.com/economics

English

@growthepie_eth @LorenzoARK @RobinhoodApp @arbitrum Oo good catch! Robinhood is an L2, not an L3.

Still relatively small numbers but already 3x higher 😎

English

growthepie 🥧📏@growthepie_eth

You've underrepresented Robinhood's rent paid to Ethereum by a factor of 4x because you used Arbitrum's rent paid. 0.6% of revenue is the correct figure for Robinhood Chain. With the current low price of blobs, 98.5% of that goes to L1 settlement... You may still want this to be higher, but at least you can now reference the correct figures. See for yourself: growthepie.com/economics

QME

The Robinhood Chain is the cleanest case study of what happened to ETH's economics over time.

Since inception, @RobinhoodApp Chain has grossed ~$816K in revenue.

@Arbitrum, the middleware provider, takes 10%: ~$80K.

Arbitrum then pays Ethereum for settlement: $1,538.

The margin profile roughly:

Robinhood: 89%

Arbitrum: 10%

Ethereum: 0.15%

If your thesis is "ETH is money," Robinhood building here is ultra bullish. More activity, more ETH collateral, more lindyness.

If your thesis is "ETH is a revenue generating asset," this is the ultra-bear case.

And here's the uncomfortable truth: Robinhood was never going to build on Solana, Sui or any monolithic L1. They want the stack customization. They want to be landlords, not renters. Ethereum won this deal on merit.

It's just not pricing it right.

A healthy split to me looks more like:

Robinhood: 75%

Arbitrum: 10%

Ethereum: 15%

Ethereum sells the most valuable settlement layer in crypto at marginal cost. Things need to change. @ethlabs_org

English

matze | growthepie 🥧 retweetledi

I bought this old home after it had been abandoned for roughly 20 years.

No grid connection, no landline, no sewage, no fresh water pipes.

Super excited to bring it back to life.

ama

English

It's refreshing to see how the content in my feed is slowly more optimistic again.

I think 2026 + 2027 will be big for Ethereum. I also see a solid chance for another run to #1 and to take on Bitcoin.

- Quantum roadmap for Ethereum is solid

- Robinhood, as one of the biggest (or even the biggest) finance app for consumers, is providing proof that L2s make sense for businesses -> many other businesses will evaluate and follow

- Crypto UX still isn't great but it's significantly better than during the last cycle

- Agents will use blockchains and prefer the one's with deep liquidity (Ethereum)

- Basic financial instruments that were novel 4 years ago "just work" now on EVM (stables, lending, options, etc.)

- Fundamentals, despite the bear, still look strong (easy all at 2x from previous bull)

- Ethereum keeps reinventing itself with new orgs like @ethlabs_org and @ethereuminsti

- Big L2s like Arbitrum, Optimism, Polygon, Base, MegaETH, Celo, Starknet, Taiko, Soneium, World, Linea, Ronin, Mantle, and many others are all helping with distribution (all in their own way)

- The Ethereum ecosystem is becoming more pragmatic in many ways and will learn from all these experiments that we ran in the past 4 years (DAOs, grants, tokens, etc.)

It won't happen overnight, but slowly many theses from Ethereum land will work out.

I'm bullish ethereum:native 😎

English

We may disagree on whether it is sensible to offer Ethereum security at cost, as a growth lever vs a revenue play.

But we should not disagree that the value of blockspace should increase, to make the network as a whole, with ETH at its centre, more valuable.

As long as scale is sufficiently addressed, this both supercharges growth and raises the revenue floor.

For L1: Faster slots.

For L2s: Faster finality.

For L1 & L2s: Better interop.

Lorenzo Valente@LorenzoARK

The Robinhood Chain is the cleanest case study of what happened to ETH's economics over time. Since inception, @RobinhoodApp Chain has grossed ~$816K in revenue. @Arbitrum, the middleware provider, takes 10%: ~$80K. Arbitrum then pays Ethereum for settlement: $1,538. The margin profile roughly: Robinhood: 89% Arbitrum: 10% Ethereum: 0.15% If your thesis is "ETH is money," Robinhood building here is ultra bullish. More activity, more ETH collateral, more lindyness. If your thesis is "ETH is a revenue generating asset," this is the ultra-bear case. And here's the uncomfortable truth: Robinhood was never going to build on Solana, Sui or any monolithic L1. They want the stack customization. They want to be landlords, not renters. Ethereum won this deal on merit. It's just not pricing it right. A healthy split to me looks more like: Robinhood: 75% Arbitrum: 10% Ethereum: 15% Ethereum sells the most valuable settlement layer in crypto at marginal cost. Things need to change. @ethlabs_org

English

@chriskeshian Haha not much to gain for anyone but always happy about visitors 😄

English

@web3_data Two questions:

1. Can you send a zoomed out map and address

2. Unrelated, do you keep your private keys on you

English

Main task for this week is to make space around the dead trees so that we can cut them down on Friday.

Since the trees are close to the building, we'll have to be a little more careful.

Plan:

- clear path for trees to fall in

- removing lower branches on trees

- using a winch to pull the trees in the right direction

- cut them down

matze | growthepie 🥧@web3_data

A list of the current (high-level) tasks: - house + driveway accessible ✅️ - removal of dead trees next to building ❕️ - junk removal - new roof - fixing well + testing water quality - understanding current sewage system - gutting the house completely + 100 other things that I'll figure once we get to them

English

@web3_data @growthepie_eth The whole list is solid

The L2 one grabs me most, we can already watch it happening

English

@web3_data @growthepie_eth Agree on the L2 thesis

English

@adamparrish Haha glad you're enjoying it Adam! Hope everything is going well for you :)

English

@web3_data This is quickly becoming one of my favorite things on the internet.

English

A list of the current (high-level) tasks:

- house + driveway accessible ✅️

- removal of dead trees next to building ❕️

- junk removal

- new roof

- fixing well + testing water quality

- understanding current sewage system

- gutting the house completely

+ 100 other things that I'll figure once we get to them

matze | growthepie 🥧@web3_data

Next up, making sure the house itself is also accessible, without branches hitting me in my face wherever I step. Same angle, same stairs - they clean up nice :)

English

@0xNLYFANS 🙏 just getting started :) feel free to lmk if there's anything in particular that you'd be interested in!

English