When you know why it's about to happen, how it's about to happen, what's about to happen, and by when it could happen.

Everything becomes slow motion.

In a state of ultra instinct.

Nobles —@nobles305

I want to follow up and clarify my position from yesterday.

Based on the E*TRADE notice alone, I initially treated this as a possible broker-side categorization issue rather than evidence of a real tender offer. Given how generic front-end broker language often is, that was a cautious interpretation at the time.

What changed my view was seeing the DTCC back-end event classification tied to the same issuer and CUSIP, explicitly registered as “Tender Offer – INFORMATION ONLY” (OPTION: NA). That additional layer of data matters. Once something is formally registered at the DTCC level, it can no longer be explained as a UI coincidence or labeling overlap.

“Information only” doesn’t mean there is no offer — it means the offer exists structurally, but the economic terms and elections haven’t been activated yet. That distinction wasn’t clear yesterday without the DTCC context.

So the update isn’t about flipping narratives, just about incorporating better data as it became available. No assumptions about price or outcome — only acknowledging that this is now a confirmed tender event at the clearing layer.

Appreciate the discussion and the push to keep it precise.

Google definitions don’t rewrite bankruptcy plans.

Being an accountant, this should be straightforward for you.

Cash doesn’t get implied. It gets booked.

If releases were exchanged for money, there would be cash consideration language, a stated amount, and a corresponding cash entry. None exists.

“Consideration” in a legal finding isn’t a substitute for cash flow — and you know that.

This isn’t bullish vs bearish. It’s accrual vs imagination.

@youknowwho2b@jake2b Jfc, Google it. It represents price; goods, money, services, etc.

This is why those who understand it are bullish. It's because, and hear me out here... we fucking understand it. 🍻

When the argument runs out, the focus shifts to “AI prompts.”

That’s not a rebuttal — it’s a deflection.

This discussion isn’t about how anyone analyzes the text. It’s about what the text actually says.

If the Plan states the releases were exchanged for cash, quote it.

If it doesn’t, attacking the method instead of the language just confirms the gap.

@youknowwho2b whatever you are prompting your ai it is not responding on the subject we are discussing anymore.

have another look at the Plan Supplement. it says what I am saying.

everything you put into your ai about JPM is incorrect, they were already removed from the creditor queue.

@Bbq_79BU@Kraven1776@jake2b Releases are not money.

They don’t create funds, they don’t belong to anyone, and they don’t make classes whole.

They exist to make the Plan legally confirmable — nothing more

@Kraven1776@jake2b@youknowwho2b 3rd party release funds are entitled to everyone in the bk. Since judge papalia forced down the 2.5% technically to move it along its his ass on legal line if class 6 isnt made whole from all the funds in the release. Sure class9 will make bank but cl6 lawfully gets 100% also

In Chapter 11, consideration does not default to cash, even when the counterparty is JP Morgan. Lender consideration routinely consists of consent, forbearance, lien waivers, claim releases, cooperation, and voting support.

“Not yet consummated” changes timing, not substance. It doesn’t magically turn non-cash consideration into money.

If cash had been paid for the releases, the Plan or Supplement would explicitly say cash or monetary consideration and state an amount. Courts do not imply cash. Ever.

Calling settled bankruptcy doctrine “nonsense” just highlights the lack of textual support.

your assumption about the financial record-keeping is incorrect. the Plan Supplement makes it clear that the third-party release has not yet been consummated.

and my image absolutely implies that cash was paid because the main benefactor is JP Morgan. what other kind of consideration would they be providing? nonsense.

That sentence establishes that the releases were supported by legally sufficient consideration, as required for approval.

It does not state — or imply — that cash was paid.

In Chapter 11, consideration includes consent, claim waivers, and plan support. Cash consideration would be expressly stated. It is not.

If money had been paid for the releases, the Plan or Order would explicitly say cash or monetary consideration and identify an amount.

It doesn’t — because the consideration was non-monetary. 😊

@seymourbutts741@jake2b@I_only_use_tide Releases can be critical to plan confirmation without generating a single dollar.

Approval is procedural. Proceeds are financial.

Mixing the two is the mistake.

If releases “directly created cash,” point to the Plan language where cash is paid for the releases and the PCR line where that cash is booked as proceeds.

If the only cash comes from an asset sale, then the asset created the cash.

Rebranding sale proceeds doesn’t change their source.

Hair-splitting is necessary when loose language starts inventing outcomes.

In BBBY, releases didn’t create cash — they preserved issuer continuity.

They removed litigation risk so the same registrant could survive with valid stock, warrants, and post-confirmation corporate actions.

Assets generate proceeds. Releases remove risk. Continuity preserves rights.

@ThePPseedsShow

you’re splitting hairs. if it weren’t for the releases the lien holders would not have agreed to transact for the asset. this is all documented in the Plan.

the third party release will be a multi-party transaction. there needs to be money coming in exchange for the release itself, that is how the Plan is written and the release approved. separately, there is an agreement that as a result of the protections provided for in the release, there was an agreement to transact for the asset.

you can’t have one without the other.

the releases generated proceeds. the Plan is clear about this and has multiple pages of disclosure confirming it.

I believe all of it also tied to an Asset Sale Transaction which when consummated, will be funded into the General Account and presumably disclosed in the PCR statements.

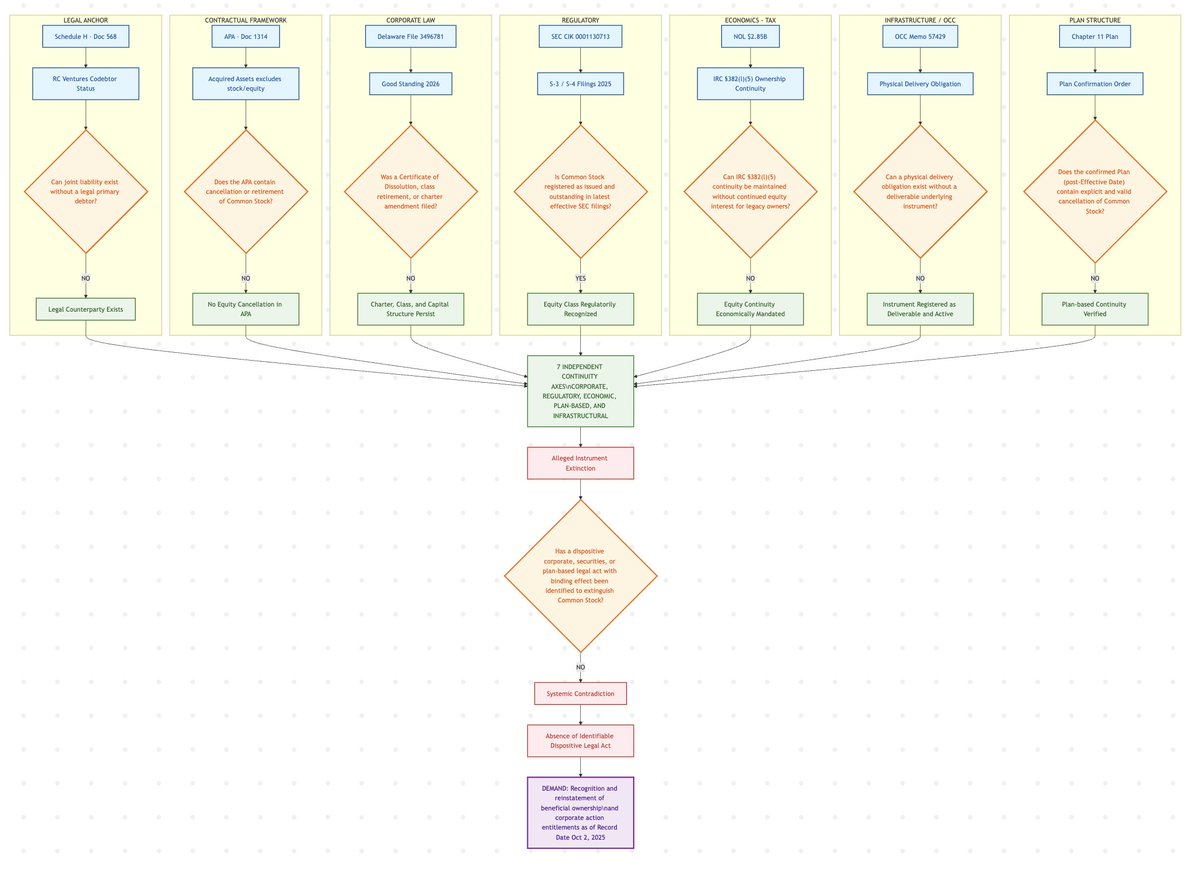

Good question.

By substantive event I mean an event that creates, modifies, or extinguishes rights or obligations for holders.

Examples would be:

– an issuer initiated tender or exchange offer

– a warrant exercise window with consideration

– a merger closing or conversion

– a distribution or cancellation backed by an issuer action or filing

Using an active issuer CUSIP for warrants does not by itself constitute a substantive event.

CUSIPs identify instruments; they don’t create rights.

In this case, there is:

– no offeror

– no consideration

– no election

– no Schedule TO

– no issuer initiated action

That’s why I view this as non substantive.

The governing language is INFORMATION ONLY / NO ACTION REQUIRED.

Happy to clarify further.....😉😀

@youknowwho2b@MorganStanley@etrade@marcuslemonis What is a substantive event for you? Do you believe using CUSIP on an active company used for warrants satisfy that term? Let’s hear it my man enlighten us👍🏻

Cutoff dates and “confidential materials” language are standard system placeholders used for all TEND-category events.

The governing text here is INFORMATION ONLY / NO ACTION REQUIRED, which means no offer exists and no materials exist.

This is a routing artifact, not a substantive event.

ANC – Anti Noise Cancellation

After three years of signal pollution, it’s time to turn ANC on.

NOISE (what does NOT matter):

• Vibes, photos, emojis, coincidence timing

• Named individuals used as narrative anchors

• Motive speculation and inferred intent

• Chapter 11 framed as conspiracy

• “Equity wiped” stated without legal scope or duration

• Broker UI screenshots and internal status labels

• Accounting language treated as dispositive law

• Forced narratives built on analogies (Berkshire, moats, tokenization) rather than legal structure

Noise creates stories. Not rights.

SIGNAL (the clean tones):

🎵 Issuer continuity

Bed Bath & Beyond Inc. continues as the legal issuer.

Same CIK. Same common stock class.

This is established through SEC filings.

🎶 Equity interests were extinguished, but contextually

Chapter 11 extinguished debtor-era equity interests for purposes of the estate and its waterfall.

That extinguishment was limited to the debtor context and does not, by itself, constitute a perpetual prohibition on future rights tied to a continuing issuer.

🎼 Rights can attach only through a new legal reference

Post-Chapter 11, any entitlement must arise from a new, affirmative legal reference, such as:

• a new record date

• a corporate action

• a distribution defined by issuer disclosure

This is not revival of old interests.

It is attachment of new rights in a new legal context.

🎹 The record date defines entitlement (OCC memo #57429)

The record date (2. October) determines who is entitled.

Delivery mechanics and broker bookkeeping do not redefine entitlement.

🎻 OCC + S-3 + S-4 define the structure

• OCC confirms the existence and deliverability of securities

• S-3 defines the maximum issuable supply, not entitlement

• S-4 confirms issuer continuity and merger structure

Together, these establish that entitlement is legal, while deliverability is technical — and the two are not required to align instantly. But align they will...

ANC engaged. 🎧🔇🧘♀️

Time to hear the beautiful outro and get paid.

@ThePPseedsShow@No_Pie_2109@nobles305@michaeljburry@owlofthematrix@PhantomBlack699@jake2b@Giggle_Pufff@pulte@marcuslemonis@AustinTobitt@BBBY_Bondholder@Hey_ross