@StonkChris I missed your VIVO post, but found the stock elsewhere. I am so very very bullish on it.

English

Red Panda Invests

1.3K posts

@RedPandaInvests

Just a red panda that likes his stocks. AI + Crypto focused, but value matters. Just my opinions. No financial advice.

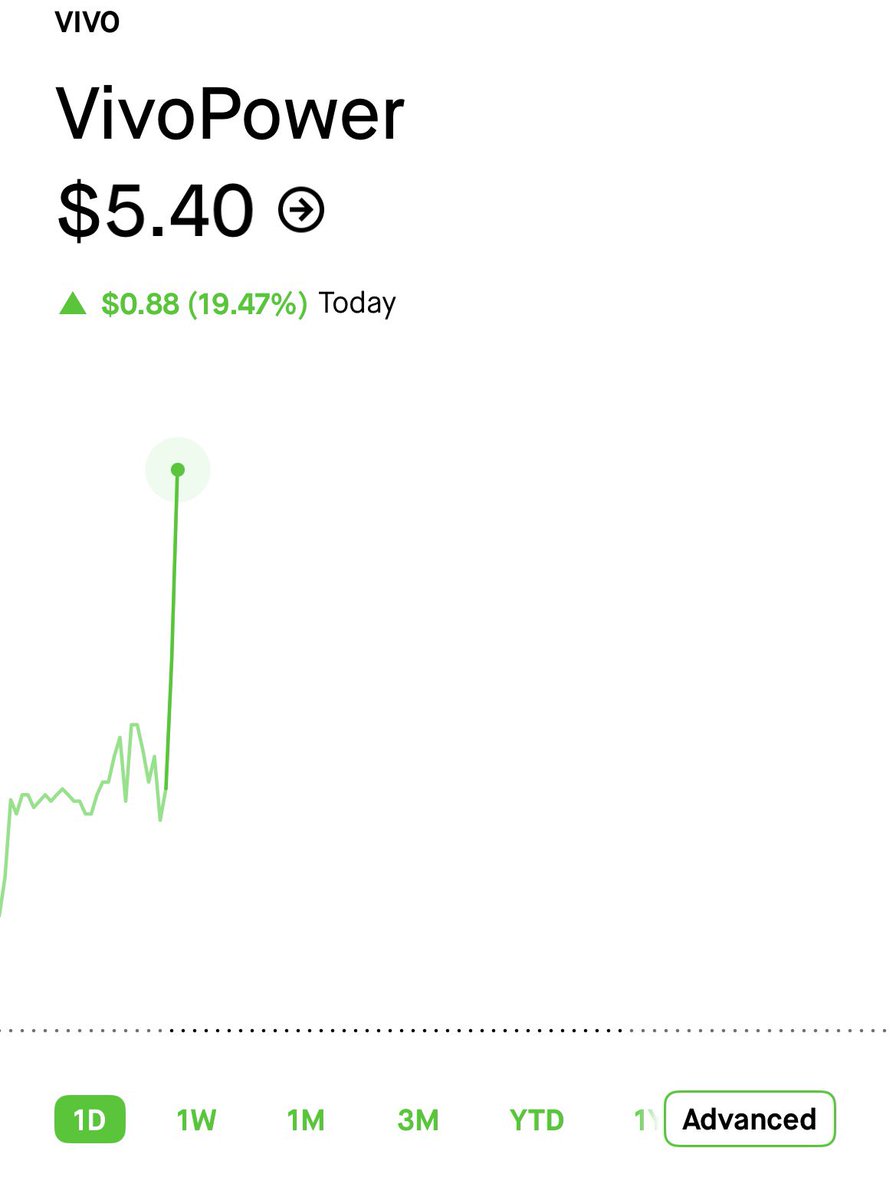

$VIVO is another small cap AI data center name I’ve been tracking long before the FinX crowd started paying attention. Mentioned last night this had potential to become the next $DGXX, and now we’re finally getting that God candle confirmation today 📈. x.com/StonkChris/cre…

I really do think a majority of Crypto AI related plays can 10x from here. $GRASS $NEAR $FET $RENDER

On my investment views and portfolio. AI disrupted everything. On a personal note it did so for my personal work, strategies I ran, work load, tools, businesses I own. It disrupted entire industries and sectors. Beyond it the most significant shift to me is the introduction of new self governing business entities aka AI agents. As money flew into AI it flew out of Crypto. To me that provided one of the best pitches I have seen ever. Only other ideas I felt this strongly about were $BABA $MELI and $UNH (these are all in my top 5 biggest wins ever). I see the world moving to everyone running Family offices. You are the mastermind and run hundreds of AI agents that help you manage your life, your business, any needs and proactive actions. Each action requires authentication, verification, payment and reputation. This is simply impossible to do with the old system. Crypto does not compete with AI, it completes it into the new age of intelligence based workers. The only chain that is secure enough, decentralized enough, fast enough, allows for all facets of the above and has the critical mass of capital, history and developer base is Ethereum $ETH. Now add to the above stablecoins for ex-AI, store of value, Tokanization and alike and you have a mega trade. Not to mention a 5y+ consolidation and a small 300b market cap compared to a worldwide implementation of this new tech. People priced it in as completion to AI and software where as it’s actually infrastructure for AI and ex-AI.

Genuinely think the most asymmetric opportunity that could yield the highest return over the next 5 years is $ETH The best part? About 99% of investors have given up on it, $BMNR and any other ethereum related equity.