@stokdog Stone age did not end because they ran out of stones.

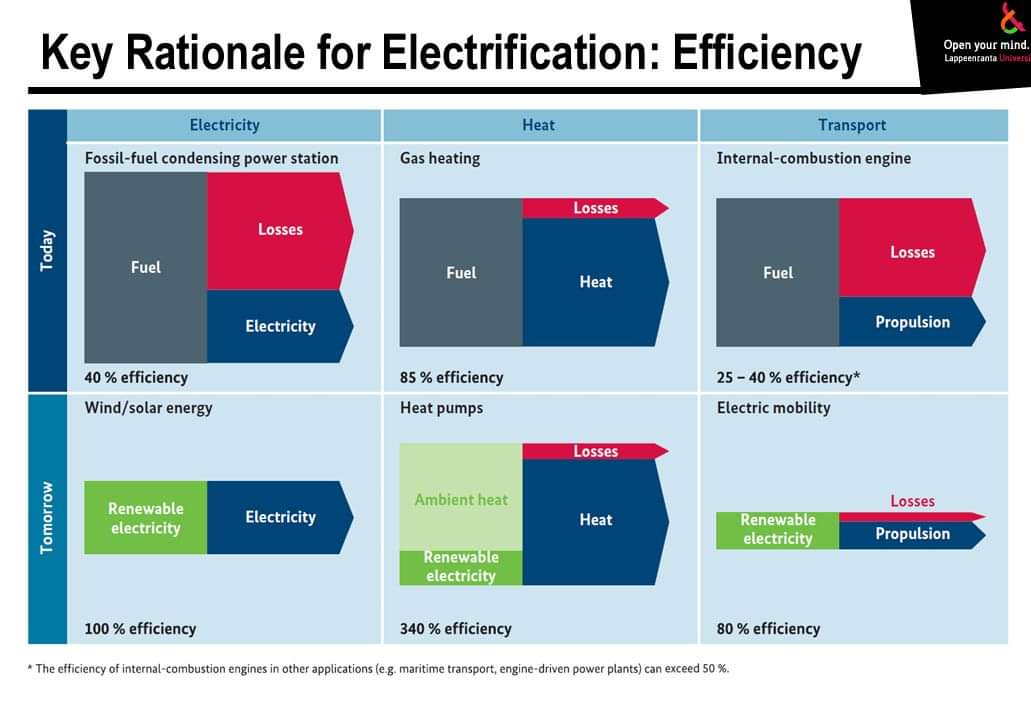

Over 60% of the energy from fossil fuels is wasted.

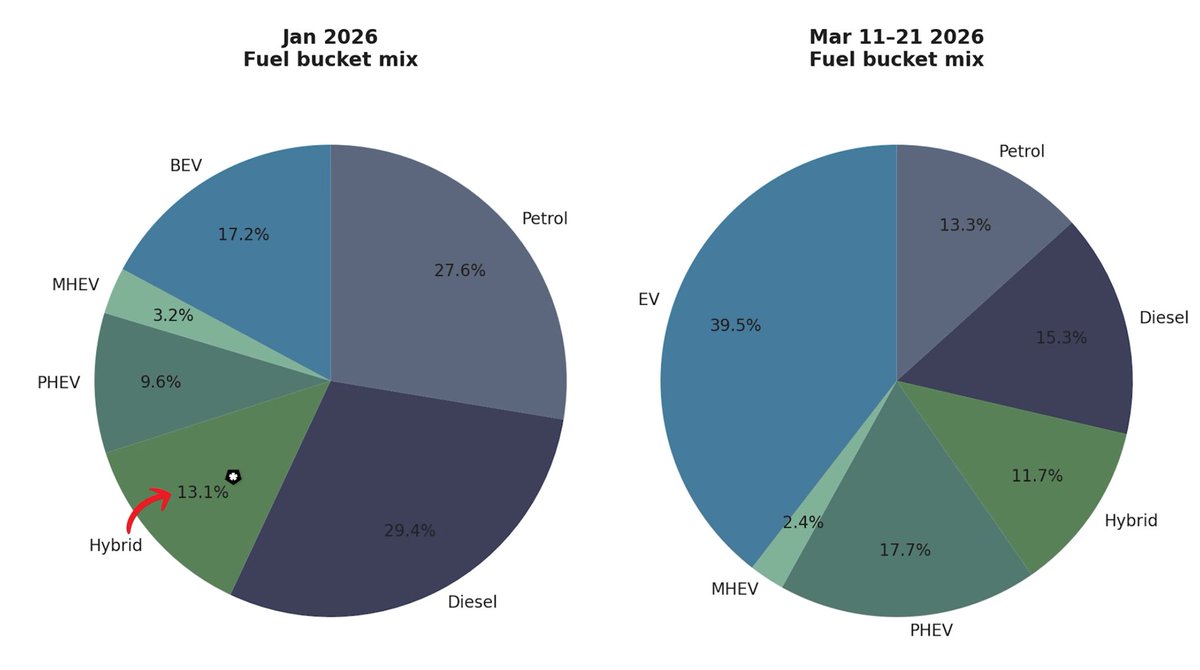

Similar to FF brain-dead proponents.

* Electricity from 40% to 100%

* Heat from 85% to 340%

* Transport from 25% to 80%

English

Hugh Butler

4.1K posts

@HughButler35

Author, research, innovation, angel investor, strategic management. Start-up in datacomms, solar. Medicine. 310 ppm @hughbutler35.bsky.social

I have never seen a transition to BEV close to this fast. Indonesia is on an entirely different level. Every time I add more recent data I think to myself "this can't go on this month, can it?", but it does go on. Indonesia has ~600k registrations per year, so they are even a decent size.

In Australia right now, a diesel prime mover sits at A$200k–$250k. The Windrose BEV E700 lands at A$450k–$500k. “Twice the price.” That’s the headline. That’s where most people stop. Layer in Tesla. The Semi is arriving at US$260k–$300k (~A$400k–$460k). And BYD? In a different league entirely—scaling heavy-duty electrics in China at aggressive prices through full vertical integration. Yes, electric still carries the upfront premium. But that’s the wrong comparison. You’re not choosing between A$250k and A$450k. You’re choosing between: • Diesel: A$250k + ~A$2 million in volatile fuel over 10 years • Electric: higher capex, then structurally far cheaper to run The Windrose isn’t a compromise. ~700 km loaded range. ~700 kWh LFP pack. ~1,400 hp. ~870 kW charging. ~68-tonne capability. That’s diesel performance—without the fuel dependency. Tesla’s Semi is already proving materially lower real-world cost per kilometre in fleet deployments. BYD is industrialising faster, quieter, and cheaper. Here’s what actually matters. The visible gap (purchase price) is shrinking fast. The invisible gap (operating cost) is widening faster. Those two curves are converging hard. That’s the squeeze. Once they cross, adoption doesn’t crawl—it flips. Freight doesn’t care about narratives. It cares about cost per kilometre. And the loop is now running in electric’s favour. Oil shocks used to reinforce oil. Now they accelerate its replacement. Every diesel price spike forces fleets to run the numbers. Every electric truck on the road kills future diesel demand. That weakens supply investment. Which makes the next spike worse. We’re sitting in diesel’s last comfort zone on sticker price. The real shift isn’t happening on the invoice. It’s happening in the system underneath. And when that system flips? Diesel doesn’t compete. It gets exposed. ⚡🔋 #Bettrification