DBP

465 posts

$IREN CEO @danroberts0101 on @theallinpod along with $CRWV (CoreWeave), Perplexity, and Mistral

The All-In Podcast@theallinpod

🚨INTERVIEW SPECIAL!: Four CEOs on the Future of AI: CoreWeave, Perplexity, Mistral, and IREN (0:00) Intro live from Nvidia GTC (0:37) CoreWeave CEO, Michael Intrator (32:58) Perplexity CEO, Aravind Srinivas (1:07:11) Mistral CEO, Arthur Mensch (1:18:57) IREN CEO, Daniel Roberts -------------------------------------- Our episode is sponsored by the New York Stock Exchange - a modern marketplace and exchange for building the future. It all happens at the NYSE - nyse.com

English

If your Mining Mafia membership application is still pending or you want a fast-track review on a new application… reply with “review” within 4 hours… I’m actively reviewing applications.

If you’re an existing member and want to show your support comment “Few”

x.com/i/communities/…

English

The Wynn has always been like my second home 🎰 stoked to announce my 2026 Vegas residency with @WynnLasVegas. dates are LIVE now, let me know which show y’all want to come to & I’ll pick one person to fly out to any show + bring their friends on stage for the night…who’s down?

English

@TheKamaHsutra @Agrippa_Inv @_Sgr_A_Star @brianfry01 Agrippa can definitely go for the leaner cuts and eat the A5 chauteaubriand cut daily

English

English

Merry Christmas everyone!

At this time of year I like to let my imagination run wild and think about what 2026 will bring for all of us involved with $IREN and the AI space.

🚨 Dan Roberts has given us a Christmas Present post.

"Vertically integrated clouds compound ownership.

Asset-lite neo-clouds compound lease exposure.

Every day, the gap becomes more real."

Translation:

$IREN owns power, land, data centers, GPUs—complete vertical stack. Every capex dollar → appreciating assets → lower costs → stronger margins → reinvestment → sustained dominance.

Dan and Will Roberts (Co-CEOs) see the exponential AI Factory future clearly: massive scale, extreme compute density, rapid model iteration, and winner-takes-most economics. Leasing adds friction and limits control. Full ownership removes bottlenecks and unlocks true speed, flexibility, and compounding advantage.

And here we are: $IREN in full exponential acceleration. Can you imagine what is going to happen in 2026? So exciting!

#IREN #AI #BitcoinMining #VerticalIntegration #AIFactory

Daniel Roberts@danroberts0101

Vertically integrated clouds compound ownership. Asset-lite neo-clouds compound lease exposure. Every day, the gap becomes more real.

English

@litigious_dulce I was anticipating a 30% pullback, but this beatdown was definitely not on my bingo card

English

I haven't posted a lot as of late, but don't mistake silence for quitting. The trend will reverse at some point.

I'll be honest, I learned some lessons. First: bears never die. They are far more underhanded than I could have ever imagined, and they will find an opportunity to strike. No matter what the fundamentals are, manage risk.

Second: the stock market is weird beyond belief. Some will say that a dump was predictable, and sure a pullback makes sense. But these massive drawdowns when everyone knows AI/HPC is not only the greatest innovation ever and mostly funded by positive free cash flow (see Goldman Sachs commentary)???

I really hate to admit that technicals are so important, but maybe that's the inescapable truth in an algo-dominated world. However, in the long run, we know what's coming.

English

@TheKamaHsutra I thought you would’ve used the “Proceed With Purchase” frame 😂

English

As an $IREN shareholder, I love the transparent nature of the company. Whether it's BTC mining or AI DCs, IREN stands out from its peer in terms of letting shareholders know what is going on, on a regular basis. This rare in BTC mining, but virtually non-existent in the DC building world.

In this most recent video of the Horizon buildouts at Childress, $IREN is dropping more nuggets on us if we are paying close attention.

I have echoed this theme many times in the past, Childress is a sleeping giant that many people are not appreciating. Childress already has 750 MW of energized power today (with even more possible in the future). This video frame below really captures what this means. With what is already built in the present that can be quickly transformed to the future.

Time to power is invaluable in the AI race, and at 750 MW, Childress would instantly become one of the biggest AI DC campuses in the world by the end of 2026 (or even EOY 2027) if all of it was converted to an AI DC mega campus. This is not a pipe dream that was once mocked. With the $IREN x $MSFT deal, we know for certain that hyperscalers extremely interested in Childress for very good reasons.

What enables the possibilities of Childress becoming one of the biggest AI campuses in the world so fast is $IREN's foresight, and thinking through first principles. The shells used for Horizon DC shells are largely the exact same shells that are already built and currently housing the ASIC miners for BTC mining. IREN is showing us what the interior of the shells look like with it set up for liquid-cooling infrastructure, and not the air-cooled conversion we see in BC.

IREN is touting that the Horizon DC shells and infrastructure as being future proofed. This is largely done by having all of the mechanicals separated from data halls inside the shells. When the time comes to upgrade the mechanical components, it is much easier to upgrade them without disrupting the data halls.

IREN is also touting the flexibility of the of the Horizon DC designs, with the ability to offer various rack densities inside the same DC shell. This was once overlooked. However, with the emergence of the viability of other non-GPU silicon processing power, the ability to house various workloads working side by side will be very valuable. In this rending from the video, we can clearly see the GB300 racks (1). However, we also see other hardware in the same data hall, with Dell XE9680/XE9680L servers shown (2) in the same racks with what appears to be Dell XE9640 servers (3).

dell.com/en-us/shop/ipo…

dell.com/en-us/shop/ipo…

dell.com/en-us/shop/ipo…

Time to power is invaluable in the AI race. There is zero reason to believe that there isn't in fact a bidding war for the rest of Childress IMO. After the MSFT deal, I don't think Dan Roberts will ever be mocked again for mentioning an email from an hyperscaler. Don't sleep on the sleeping giant that is Childress.

English

@FransBakker9812 Would this mean there is a risk of under monetization if too much capacity from Sweetwater is potentially signed to colo agreements that are normally 10+ years?

English

$IREN

I don’t think the market fully understands that the Vera Rubin era will mark the beginning of a major inflection point for AI cloud companies that own and operate their own data centers.

As token output per megawatt increases exponentially, the power demand (TDP) per GPU is rising faster than the price per GPU.

The logical consequence is that the GPU cost per megawatt of deployed capacity will decrease relative to both the token output and the total cost of building and operating a megawatt of infrastructure.

In other words, each megawatt becomes dramatically more productive while the share of cost coming from GPUs shrinks within the total TCO stack.

This means that for each megawatt of deployed capacity, the capex mix tilts toward data-center infrastructure and away from GPUs. Over time, a larger share of the investment sits in assets that depreciate over 20 years (buildings, power, cooling) rather than 5 years (GPUs).

This shift makes every megawatt more profitable over its lifecycle. As the cost mix moves toward long-lived infrastructure and away from short-life GPUs, the site gains operating leverage: revenues per MW rise sharply while annual depreciation per MW declines, because more of the upfront capex is amortized over 20 years instead of 5.

The result is higher EBIT and net margins on the initial deployment, followed by materially higher ROIC and free cash flow when successive GPU generations are rolled into largely depreciated, already-built infrastructure.

That is the inflection point of the Vera Rubin era: a structural break where the economics of AI cloud shift from GPU-dominated cost cycles to long-lived MW-dominated cash generation.

If IREN’s Sweetwater 1 is engineered to run Vera Rubin at full density (and potentially Rubin Ultra), then its 1,400 MW footprint will amplify the structural economics I outlined: more throughput per MW, more revenue per MW, and a larger share of capex tied to long-lived infrastructure.

Canada is the golden goose, and Childress is the stepping stone —but Sweetwater positions @IREN_Ltd to generate unmatched unit economics at industrial scale, leaving peers scrambling for scraps.

Note: This doesn’t even consider the possibility of NVIDIA lowering margins as competition intensifies, nor does it factor in IREN potentially deploying TPUs, alternative GPUs, or future AI accelerators.

All else equal, each of these would only improve the economics further.

English

@TheKamaHsutra @Cloudzillas People who look back to April lows tend to forget that although $IREN at $4 was extremely attractive, there was far more risk vs now when we have seen more of the thesis play out.

English

Thanks for the shoutout. Has $IREN ran up really fast? Yes. Does it scare people looking for an entry now if purely look at the charts? Yes, perhaps. However, $IREN is just starting it's AI journey. If your bet is that AI is real, then IREN still has long ways to go to reach it's potential. NFA.

English

I invested in $IREN in early 2024 and been lurking around on X ever since. I never posted here but it was hard watching the stock round trip $15 to single digits multiple times. The last 6 months have been crazy watching my portfolio grow into the millions and finally seeing the attention this company deserves.

I still hold most of my position but the stock definitely isn't as attractive as it was in April. That being said management has been great at executing and the Iren gang on X is one of the strongest of any stock I've seen. Shoutout to the longterm goats @TheKamaHsutra @Agrippa_Inv @Umbisam @FransBakker9812 for having huge balls and keeping retailer motivated 🐐

English

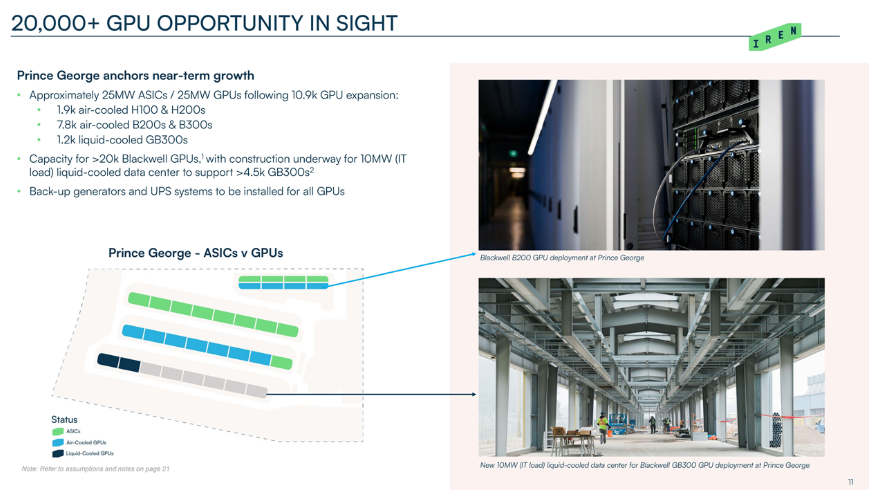

@FransBakker9812 Guidance of 140k gpus (>60k from BC + 76k from H1-4) = 136k gpus. Assumption of >60k from BC from existing MW capacity. Expansion of 10MW to 40MW liquid cooled (>4500 GB300s per 10MW) yields an additional of at least 13.5k GB300s?

English

@FransBakker9812 Hey Frans, coming back to this slide. Do you think the 40 MW expansion in Prince George for the GB300s will happen by EOY2026? If so, assuming >4500 GB300s per 10MW, it seems like IREN would have capacity for ~ 150k gpus if my math is close?

English

DBP รีทวีตแล้ว

I am so pleased by the market's reaction to $IREN's deal with Microsoft. The analysis I'm seeing on X is so asinine, so illiterate, that I can be confident we have much more to run.

My general understanding of this deal is that after 5 years, IREN will have 200 MW of a hyperscale-quality data center, 100k GB300s, and cashflow of $1B--all with potentially no dilution.

Now, I am assuming IREN secures financing, such as project financing. In project finance, the equity portion is typically around 20–30%, with debt covering 70–80% of the total project cost. This ratio is known as the debt-to-equity ratio or gearing.

So where is the 20% equity coming from? The partial prepayment from $MSFT of course!

With zero dollars (!) out of its own pocket, IREN can own hundreds, if not thousands, of MWs of data center. With zero dollars (!) out of its own pocket, IREN can own 100k GB300s. And people have the audacity to call this a bad deal...

The structure of this deal is mw-invariant, meaning that IREN can use this structure for its entire energy portfolio. At minimum, this will extend to the rest of Childress, and very likely it will extend to Sweetwater 1 and 2.

The terms of the deal can also be updated with each new GPU ($NVDA is now releasing a new product every year). That means every year IREN can do a deal with Microsoft (or another hyperscaler) for another tranche of MW, and after the deal is over IREN owns both the data center and the GPUS inside!

However, I hear some talk about how IREN's deal is worse than $NBIS's. These people believe IREN makes less money... How exactly when you don't even know the terms of the $NBIS deal? Think for a second: How is NBIS financing the GPUs? Won't NBIS own 5 year old GB300s at the end of the deal as well? And how much is NBIS paying in colocation fees?

These "analysts" don't even realize that data centers have residual value (data centers last for 20+ years)! And while they complain about IREN's supposedly low profitability, they don't even acknowledge that NBIS and $CRWV are still unprofitable! The hypocrisy stinks.

@matthew_sigel has the right take on this: x.com/matthew_sigel/…. The only way you can conclude the deal is bad is if "you assume zero residual value, zero financing leverage, and an unrealistic cost structure." But who in their right mind would assume that?

------------

IREN will make about $2.3/GPU-hr from the GB300. I believe it could easily charge $4.5/GPU-hr under a 2 or 3 year contract through its own IrenCloud. This leads me to believe IREN must have financing secured for both the GPUs and the data centers, such that the levered returns are very attractive.

English

@sammydabull911 @TheKamaHsutra Probably more cringe that you took the time to comment about what another man is wearing 😂😂

English

@DByProg @TheKamaHsutra Bro. Ain’t no one “poor”. In 2023 everyone got on board with Jesse and Mike on bitcoin miner cycles. It turned into AI. We all got lucky! Fuck it. Better to be lucky than smart sometimes. All i said was that miner merch shit is cringe. This ain’t the dodgers or Yankees lol chill

English

Gotta bust out the $IREN swag today, on a day like this. Years in the making. 😉

English

@TheKamaHsutra @sammydabull911 Just tell the loser to have fun staying poor. People say off the wall shit to just get a response

English

Why the fuck would that be cringe? That is a retarded take. I can't be proud of the company that has completely changed the course of my financial future? I can't show $IREN a debt of gratitude? I can't be proud of myself for sticking to my thesis and not be shaken out after several massive drawdowns? That take reeks of jealousy and envy.

English

Thank you @FransBakker9812 @litigious_dulce @TheKamaHsutra @bitcoinbutcher1 @Agrippa_Inv @mcF_dan and others I didn't mention. Researching in public is hard - anyone who followed you prior to this morning knew the quality of your work, but you were made legends today. Well done.

English

Where my bros @RHouseResearch @icyopro23 @Lazarus_Capital @FloodCapital at this morning? Great Morning to be an $IREN holder isn't it? 😉

And I haven't even pulled out any receipts yet.... there is still a long ways to go before I pull out receipts, and a lot more people I haven't tagged yet. 😂

English