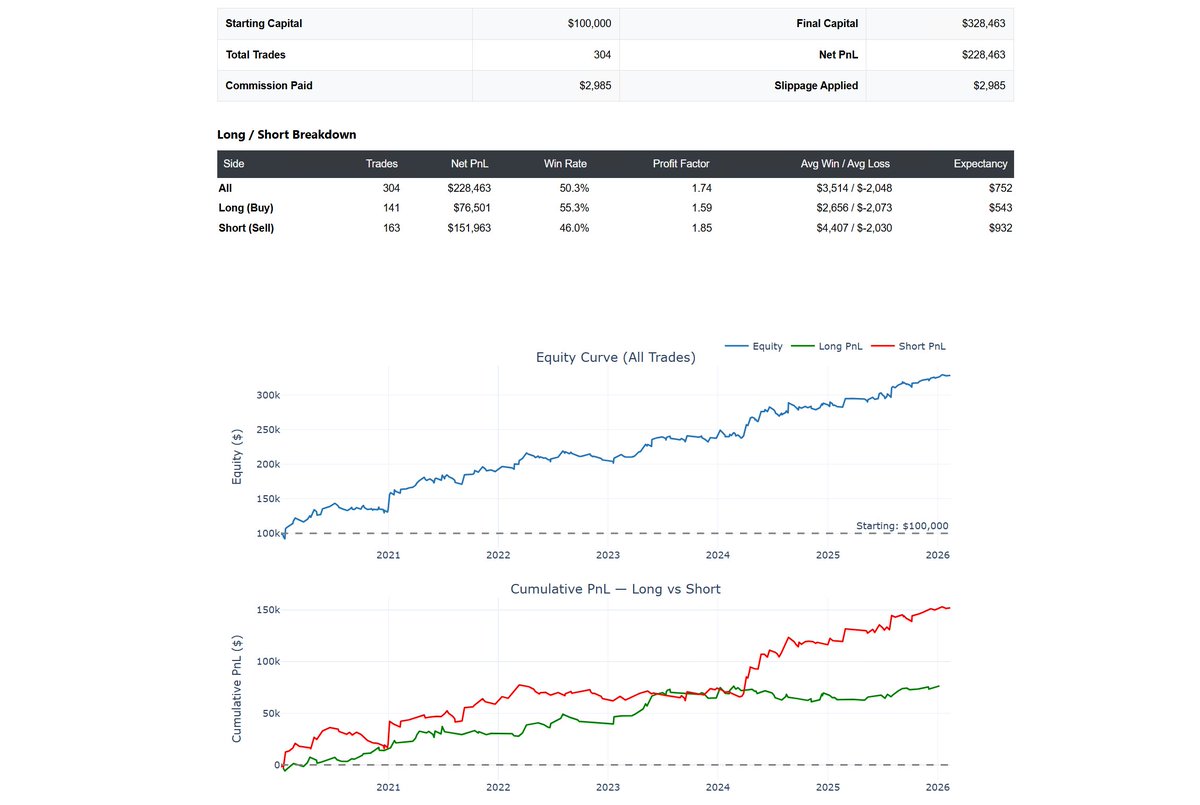

Made quite a lot of progress with my LLM research workflow by adding Nautilus Trader + Databento.

Not as “LLM hunting for the holy grail”.

I, as the trader, still define the idea, market, rules, constraints and invalidation criteria.

The LLM helps compress the research loop:

idea

-> project spec

-> Databento data prep

-> Nautilus backtest

-> metrics + tearsheet

-> red-team results

-> checkpoint + git commit

-> journal

-> next iteration

It is forcing every idea through the same process and journaling everything.

Nautilus + Databento is quite powerful and can backtest in hours what would otherwise take me weeks to research.

I am now comfortably running backtests of orderflow patterns, futures, stocks, options and even options strategies - including combinations with futures/stocks.

Execution is not in this workflow yet. We still execute with in-house Python scripts.

But for research, the speed difference is massive.

What used to take me weeks can now become a structured research session.

And I am especially happy that I can onboard my research team members into the same workflow, which should make everything much more efficient.

Read “I Used AI to Build an Intraday QQQ Trading Strategy From Scratch — Here’s What 249 Days of Data…“ by Alex on Medium: @tradermnk/i-used-ai-to-build-an-intraday-qqq-trading-strategy-from-scratch-heres-what-249-days-of-data-bfaf11bc8935" target="_blank" rel="nofollow noopener">medium.com/@tradermnk/i-u…

I’m seriously considering moving from my home-made scripts to a more universal framework for backtesting + live trading (especially for intraday). Tested NautilusTrader today and it looks very interesting.

Why it caught my attention:

- Open source

- Event-driven Python API, Rust core (fast)

- Biggest win: same strategy codepath for backtest and live (no “version 2” rewrite)

- Because it’s Python, Claude Code can actually help you ship strategies without coding.

I ported my intraday volatility breakout strategy in minutes.

Anyone here running NautilusTrader live?

What’s your experience with brokers/data/execution - any gotchas?

You read about index rebalance strategies everywhere, and it seems like a hedge fund darling, why?

It's one of the few systematic* strategies that are extremely scalable (you can run BILLIONS in capacity), and where the economic rationale for working is easily understood.

Index rebalance is all about predicting how much dollar flow is going into a stock relative to its average daily traded dollar volume. A high dollar flow relative to its usual traded dollar volume will mean the stock price will go up, and vice versa. It is beautifully simple conceptually, but VERY difficult to get right practically. A lot of PMs talk a big game about index rebal, but actually getting it right and managing your risks is NOT easy. Especially when so much of your gross returns can show up as momentum and short interest factors!

---

I write below about a foundational methodology, a starting point for thinking systematically about index changes. You’ll build more sophisticated signals over time, but this framework captures the core mechanics.

This methodology on systematic index change prediction crystallizes an approach many quant shops have traded for years.

Comment AND retweet on THIS post to get a chance for a free article!

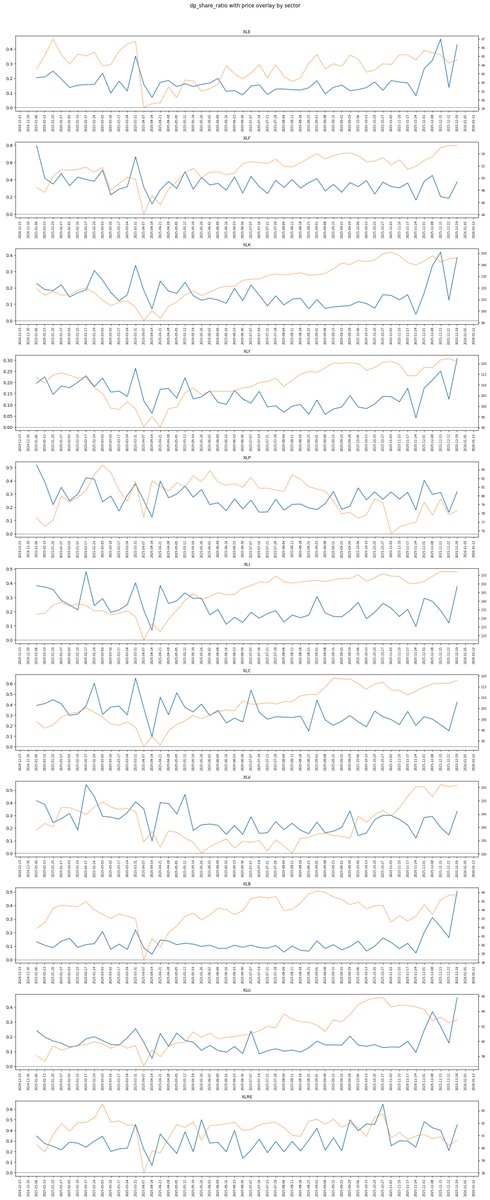

@TailThatWagsDog Inspired by your sector rotation tweet, I ran a sector‑level dp study using FINRA ATS/OTC data. Small multiples showed lots of noise but no consistent rotation signal. IMHO, I don't see dp has a clear tell, could you pls comment what could be derived from this?

@FlowAnalyst Purely candlestick formations. FYI:- I previously had strat on GEX but after 2yrs of tracking it i think I overfitted then the strat was no longer very effective. Stopped tracking it. Sorry I can't help with gex strats.

@FlowAnalyst Thanks for your feedback. I have a few setups and have freely shared some insights on my most recent developed one "Daily candlestick patterns". To the T? Well each trader will have different risk mgmt and R:R. But I give the probabilities and backtested results with the setup.

@deus_trader I appreciate you answering that in detail.

I guess before I ask you for any hints/sources/direction, I better scrape your feed to see if there's any alpha pointers somewhere! That 102.47% is just badly growing on me!

Mostly, in terms of underlying methodology. But it always evolves into more variants. In 2024 I had maybe 3 scanners producing trades, now I have 10 scanners and just picking various trades from each one. In 2024 I’ve also traded more earnings and short-term options in general but that was exhausting so now I’m more into LEAPs - even when setups are similar. Though LEAPs hold up my margin longer so I’m trading less for that reason as well.

I’m 2025 I’ve also added bearish/put-based strategies, which take away some margin from bullish ones so I trade less.

Also the 2024 strategy was helped by different vol regime that had more pullback, while 2025 was more bullish without too many opportunities to buy cheaper calls, which is why I started looking for bearish setups.

In 2025 I also started trading larger stocks that took away my margin, but likely missed on many smaller runners (AI, semi, energy, minerals) that otherwise I might be buying early as well.

So really I’m building an arsenal of setups that I can tap into depending on market conditions and individual opportunities. Now I have more trade ideas than I can handle time- and margin- wise.

Just posting my last status/balance for 2025. Made $1M+ trading options this year (a Nobel prize) just like last year, now need to pull some money out of other ventures to pay taxes.

Haven’t really been trading last few weeks. Though I’m spending nights staring at a mechanical model of a universe that is also the most symmetric and self-consistent model of spacetime (invariant in space and time). Can’t even define it properly yet because it’s so invariant that it cannot be easily scaled mathematically (like speed of light), even though you can model or draw it at different sizes. Imagine an equation that gives you the same circumference for every circle radii.