Jason Wong

1.2K posts

Jason Wong

@Jason_KYW

Strategic Finance @blocks @afterpay_au | previously M&A @armapartners | learning about fintech, saas and angel investing

London, England เข้าร่วม Aralık 2018

1.1K กำลังติดตาม127 ผู้ติดตาม

OpenAI and Anthropic engineers leaked a prompting technique that separates beginners from experts.

It's called "Socratic prompting" and it's insanely simple.

Instead of telling the AI what to do, you ask it questions.

My output quality: 6.2/10 → 9.1/10

Here's how it works:

English

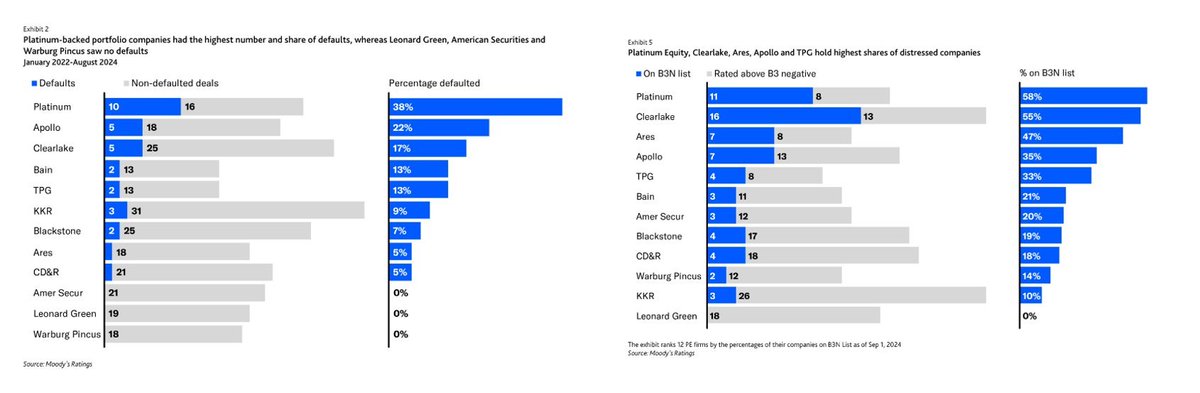

MOODY'S REPORT ON DISTRESS IN PRIVATE EQUITY LAND | A MUST READ

As a former restructuring banker and current private equity associate, this is a must read. So excited to dive in —→

1) Large-Cap Private Equity Recent Defaults

2) PE shops with the most default deals

3) PE shops with the most dividend recapitalizations

4) PE shops with the most distressed deals

5) Upgrades and Downgrades across PE Shops

6) Approach to Leverage across PE shops

7) Downgrade odds across PE vs non PE companies

A 🧵 Thread

English

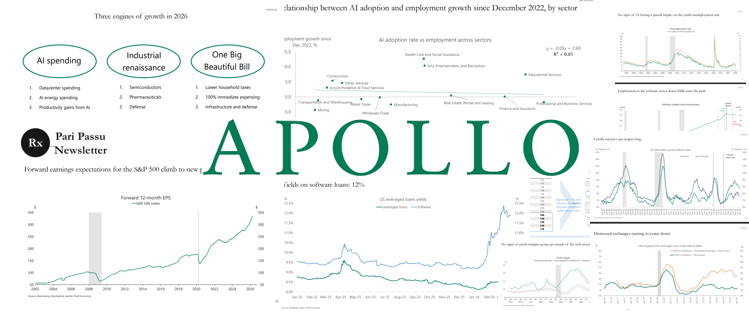

Great 50 page deck from Apollo on the Outlook for public and private markets

1/ Growth algo for 2026

2/ S&P Earnings outlook

3/ Credit Markets Overview

4/ AI Impact on Employment and Software Jobs

5/ AI Adoption x Employment Growth Correlation

6/ AI Impact on Margins

7/ Software Loans = High Yield

8/ Public IG Index evolution 🧵

English

🚨 BREAKING: Note-taking is a waste of time.

Claude can build a second brain for you in minutes.

Here are 10 Claude prompts to think, organize, and remember like a machine:

English

Final interview.

They ask: "What are your salary expectations?"

Your mind races.

You say: "I'm looking for around $100k."

They smile and write it down. You just cost yourself $30k in 5 seconds.

Here’s the answer that actually maximizes your offer:

English

BREAKING: AI can now build financial models like Goldman Sachs analysts (for free).

Here are 12 Claude prompts that replace $150K/year investment banking work (Save for later)

English

As a new manager, my biggest regret is how I handled underperforming employees. I gave them the benefit of the doubt for too long and my team suffered as a result. Sometimes, my best people left instead. Here are 3 tests I now use to act more decisively:

English

Career mistakes to avoid in 2026

1. Waiting to be noticed instead of positioning yourself

2. Avoiding uncomfortable but necessary conversations

3. Over-explaining instead of delivering results

4. Believing effort alone guarantees progress

5. Ignoring feedback that could sharpen you

6. Staying too long in one place out of comfort

7. Confusing loyalty with growth

8. Being good at your job but invisible

9. Avoiding personal branding

10. Not documenting or communicating results

11. Networking only when desperate

12. Underestimating the power of soft skills

13. Rejecting mentorship and guidance

14. Playing safe for too long

15. Saying yes to everything

16. Not understanding how business really works

17. Ignoring industry trends

18. Complaining without taking action

19. Resisting change

20. Working hard with no clear direction

21. Treating your career casually

22. Hoping instead of planning

Talent is not enough.

Careers grow intentionally, not accidentally.

English

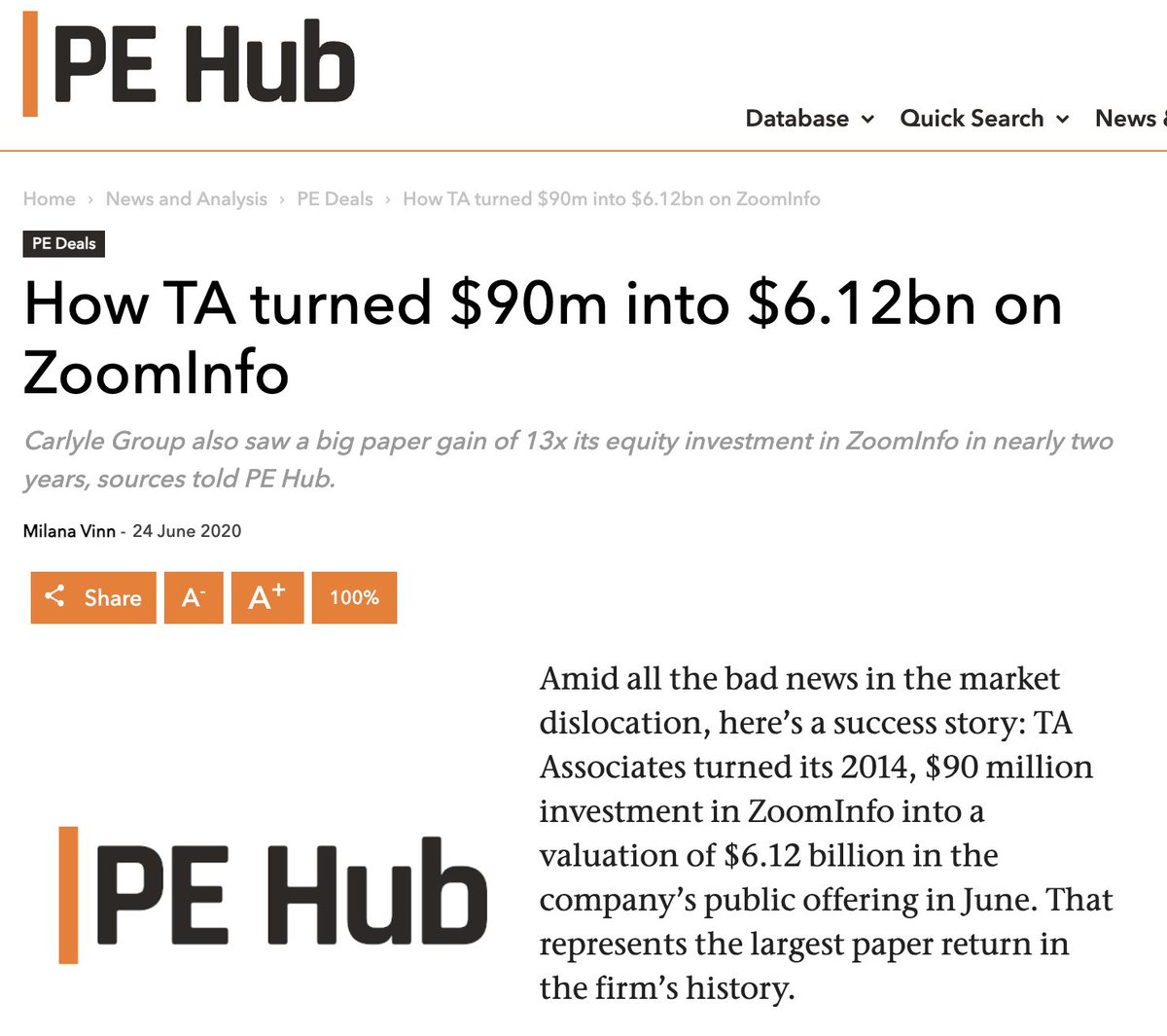

Over the last 12 years, I've worked with 4 Private Equity funds at ZoomInfo. Here’s my 12-step playbook for working with PE Owners.

In 2014, I took on my first PE investors (TA Associates and 22C Capital).

In 2018, we brought on Carlyle and CPPIB.

Private Equity is in the headlines everywhere now - buying businesses like Smartsheet, Zuora, SolarWinds, Avalara…

Here are lessons I learned on how to make working with them a LOT easier.

1. Get aligned from Day 1

Ask them what they underwrote the deal to. That’s a fancy way of asking:

“What did you tell your investment committee this business would be worth in 4–5 years in the base case?”

Then ask about the upside case.

If you want real alignment, ask for the memo. If they get squirrely, just say:

“I assume there might be some misgivings about me in there - can we talk about those so I’m aware?”

There is no faster way to get aligned than seeing exactly how they described the investment.

2. Understand the clock

If you want to invest in growth and bring down margins to do it, do it early. As you approach exit, EBITDA becomes a sacred cow.

Want to launch a new product? Great. Show what sales is committing to it and when. If you can’t do that, don’t even bother asking.

3. You don’t have to do everything they tell you

After my second board meeting I went to D. Randall Winn (my PE board member and CEO of S&P Capital IQ) and said, “Randy, just tell me what you want me to do and I’ll go do it.”

He laughed and said: “Whoa whoa, that's not how it works - no one here knows your business as well as you do. We’re going to give you advice and pattern match. Your job is to listen and decide.”

That said, you MUST listen to their advice and explain your choice. This doesn't have to happen immediately.

Try phrases like this: “I hadn’t thought about that - it’s a good point, I want to take some time to think it through and get back to you.”

Then actually follow-up.

4. You NEED a strong CFO and FP&A team

Most of your private equity investors’ interactions are with your CFO. A strong CFO and FP&A team build trust. They help you craft strategy around data AND they're endlessly valuable to your PE partners because they can build models and get them the data they need to understand what’s happening in the biz.

This makes life easier for you and them.

5. Response time matters

PE employees work all hours. One of the associates on our deal told me that she was sleeping in her car outside their office for ~2 hours and then starting to work again cause she didn’t want to waste 30 mins driving home.

When they email asking for clarification or making a suggestion, respond fast - even if it’s just to say you’ll follow up.

6. Send them swag

This one might sound dumb, but you want them to FEEL like they are on your team. When you get new swag, put it in an envelope and send it with a nice note - you want them to feel the same level of pride you feel in your company.

7. Expect pressure to do M&A

I remember being at a PE conference where they flashed a slide showing that portfolio companies that did M&A far outperformed the ones that didn’t.

Every firm had the same slide, they all believe it and you should expect pressure here.

8. Be prepared to offshore

They believe deeply in offshoring because labor offshore can be equally talented at 1/2 to 1/3 the cost. There is an organizational tax that comes with this, you can’t negotiate it away. You just have to prepare the company to manage it.

9. When a metric goes sideways, don’t show up like a macho man

If you show up with a confident solution, you’re begging for a fight.

Instead: present the metric, share POTENTIAL hypotheses, explain what you’re testing and ask what they think you might be missing

Make them partners in solving, otherwise you’ll quickly turn them into adversaries poking holes.

10. Cutting costs is easier than driving growth

This is just objectively true.

If your strategy increases costs in the hope of faster growth, you need to answer two questions:

- What metrics and checkpoints will tell us this is working - and when do we kill it if it’s not?

- Does the additional growth actually change the multiple and valuation of your business?

If you go from 15% to 20% growth in an EBITDA-dilutive way, you may have made the business worth less, not more. Your PE partners will care a lot about this.

11. They LOVE pedigree.

Hiring someone from Stanford or Salesforce is almost never questioned. But take a risk on a state school or a non A-plus company hire and you’ll be defending that person even in good times - your job is to build the best team you can so the price of doing that is owning those hiring decisions at the board level.

12. Relationships matter

There were a handful of times where I knew that I got on the wrong side of one of my PE board members. So I would tell my wife, “hey listen, I’m flying to San Francisco or New York on Sunday and I’m going to have breakfast with them and then fly home.” Then I’d call them and just say “Hey, do you have time for breakfast on Sunday? Maybe a workout before.” They always said yes and it gave me 4 hours of time, some relationship building and then we got right into the reasons we were misaligned and what I could do better.

These were super valuable - don’t EVER underestimate the power of getting in person with your partners - same rule applies to your team.

The thing I loved about working with Private Equity is that there is no singing kumbaya pretending we are some happy family. It’s a 4-5 year relationship and the expectations are very clear.

I really appreciated that.

English

Here are a bunch of my thoughts on private equity. They won’t be popular. That’s fine.

I have been in investment banking or private equity for nearly 20 years, working with and for private equity firms. I’ve interviewed, met with, and interacted with hundreds of PE firms over the years. I’ve worked with good firms and bad firms, good people and bad people. I’ve seen what works and what doesn’t.

So that’s my background, but I’m still just one guy with incomplete information, biases, and all the other baggage that comes with being human. Take it with a grain of salt.

When I started in the space, private equity felt entrepreneurial. We called them “shops” (maybe that was just us?). They were hungry. They took risks. Success was not guaranteed.

I started my career excited about the prospect of joining, buying, fixing, growing, and selling companies. Since then the space has changed. That’s natural in any industry.

But PE has become commoditized. A systematic career ladder.

People don’t join PE because they love businesses or because they want to innovate. They join because it’s one of the safest, highest-paid tracks in America. If you make it into the system- the right schools, the right banks, the right funds, you’re set. Worst case, you fail and go do something else in finance. Best case, you become a Managing Director (MD) and make generational money.

That is not risk-taking. That’s joining a protected class.

The industry has been drifting. There are more firms than ever, more funds than ever, and more Patagonia vests being sold than ever before. Profits attract competition. That’s not new.

What used to be exciting and entrepreneurial is now systematic.

And people inside it are deeply defensive of this system. They don’t want change. Why would they? The system is working for them. It’s the rest of us who are just not appreciating how much value they actually create! (PE is not exactly known for its humility.)

But the system is good if you can get inside. Use other people’s money, take out debt, charge fees, and enjoy preferential tax treatment.

Still, there are signs of cracking - more recently, returns mimicking the S&P500 and longer hold periods are increasingly normal. Continuation funds are more common.

But the point is the system is asymmetric to the benefit of the private equity firms, the GPs.

Private equity general partners make money whether their investors do or not and sadly, whether they improve the companies they buy or not.

How? Fees.

Fees on capital raised, management fees levied on the companies, transaction fees, reimbursements, etc.

Keep in mind, these fees are disconnected from performance. Management fees are based on capital raised or charged to the companies for the pleasure of their ownership. On top of that, there can be other fees- transaction fees, deal fees, reimbursements, etc.

So right out of the gate, the firm is making money, whether they perform or not.

And when private equity does perform, they take a meaningful chunk of that value too. The classic 2&20 structure means they take a 2% fee on the capital raised and 20% of the earnings above a certain threshold (carried interest).

All together, ChatGPT reports private equity GPs collect 30-40% of the total economic value of any given deal (it actually caveats that it may be more like 40-50%).

Carried interest is designed to align incentives. It is payment for the firm's labor - not return on their own investment. The partners at a private equity firm may invest their own capital, but that is not what we’re talking about here. I’m just sharing the typical take home resulting from the structure. Lucrative.

On top of capturing a huge chunk of the economic value, believe it or not, much of the take home pay actually gets preferential tax treatment.

Carried interest is taxed at capital gains tax rates, not ordinary income.

But that makes sense since PE labor is creating real value, unlike teachers, plumbers, engineers, police officers, salesmen, warehouse workers, bakers, pastors, waitresses, lawncare workers, doctors, nurses, dog trainers, construction workers… you get the point.

To be fair, you can’t blame private equity for this - it’s the tax law. They’re just capitalizing on an opportunity, but again, it’s asymmetric.

Depending on the year, the private equity partner might pay a lower tax rate than the warehouse worker in the company his firm owns. It’s the Warren Buffett/secretary example.

Private equity’s job is to generate returns. That is the job for which they labor. And yet their labor gets taxed at 15–20%, while your labor gets taxed at 25–37% plus state?

It just begs the question… why in the world are we subsidizing the labor of private equity?

Keep in mind, they’re not deploying their own capital. They’re not the ones who have the capital (they’re just in the process of collecting it). They’re not the ones who run the business.

PE buys companies with other people’s money. They charge management fees to the company they own. And when they sell, they collect carried interest taxed as capital gains-not ordinary income like the rest of us.

But they don’t just buy companies with other people’s money - they also use debt. Glorious, non-recourse, printed-from-thin-air debt.

This debt creates risk. Obviously. But if the PE firm drives a company into the ground, they can walk away. Move on to the next deal with no obligation.

Employees lose jobs. Customers lose a supplier. Banks lose their money. But the PE firm keeps their fees. They move on to the next deal.

Again, asymmetric potential losses relative to the potential gain.

Meanwhile, the small business owning pharmacist who takes out an SBA loan to build his own business has to personally guarantee his loan. If the business goes under, he’s making payments until the bank is whole.

A student making an investment in education, with hopes of earning a living (future returns) is stuck with his loan too, even post bankruptcy!

So the pharmacist and student have to pay back their loans, but a private equity bro can load a company with debt, run it into the ground, and walk away scot-free?

Make it make sense.

(By the way, when new debt is issued, money is created out of thin air. This dilutes the power of your dollar- but that’s a topic for another day.)

Inside portfolio companies, the dynamic is just as distorted. MDs suggest ideas. Everyone scrambles. FP&A burns weeks. CEOs chase ideas they know are dumb because saying no is dangerous. CFOs burn out. Operators are neutered.

I used to think the people in seats before me, who I replaced, were weak. Losers. Why did this guy make this decision? Do things this way? Now I realize they were just beaten down, neutered by spreadsheets and initiatives. They were playing to survive, trying to hang on until their company sold.

But PE folks are mostly people who have never run a business, much less worked inside one. They know debt, models, covenants, and exit multiples. And now their spreadsheets impact the most intimate parts of your daily life.

They’re buying everything: Dentists. ENT practices. Veterinary clinics. Auto shops. Gyms. Valve distributors. Engineering firms. Healthcare groups. Fast casual chains. Your lunch. Your teeth. Your cancer treatment.

Do you really want spreadsheet-driven finance firms deciding how much time your dentist spends with you? Or which treatment plan your oncologist uses? Or where the meat on your sandwich is from?

These are finance guys with spreadsheets. Again, these are people who have never been in a business much less run one, and you think that they have the tools and skill set and judgment and moral compass to drive businesses that impact not just your day-to-day life like where you have a sandwich, but your actual health? Your lifespan? Do you expect to live longer with private equity backed healthcare?

Take Jersey Mike’s. What do you expect now that PE owns it? Higher quality meats? Better trained employees?

No. You expect: prices to go up, quality to erode, employees to become less friendly, the store to be less clean, etc.

That’s not innovation. That’s a transfer of wealth from customers and workers to shareholders.

And that’s a core problem with private equity - there is no innovation. There’s no risk taking. How can you when you are going to sell as soon as you can? (but not before three years - gotta get that cap gains treatment ;))

Hopefully we’re wrong and we all love Jersey Mike’s even more in a few years but the point is - that’s not your expectation when you hear PE bought your favorite restaurant.

No one is excited when they hear private equity bought their favorite business. That tells you a lot.

Operationally, private equity often claims to take a long term view but when you know you’re going to sell in just a few years, that’s just not what happens in practice.

When you are thinking of selling your home, do you replace the roof? Nah, you just replace the shingles, put a bucket in the attic and hope the next buyer doesn’t notice too much.

That may be an extreme example, but it does happen. Regardless of whether that’s the norm or the exception, it’s impossible to be truly long-term oriented when the incentives are to maximize short-term gain.

Truth is, PE is optimizing for 3-7 years time horizons, not a 20-year competitive advantage.

There is no vision setting, no ideating ten years down the road, no innovation. There are just hard, cold initiatives designed to “optimize” and drive the profits higher.

What would I change?

Despite the above, I think private equity investing can be a force for good. Like I said, I’ve seen great firms, great deals, and great people. It can be done well.

PE would do well to recognize how others perceive them, address the criticisms, and adjust. You see some attempts at that lately (e.g., KKR’s employee equity program being emphasized and advertised), but PE is just not great at admitting mistakes. They seem (to me) to be in an especially defensive, insecure posture.

That may be because returns have diminished, holds are longer, and continuation funds have risen in prominence.

But there’s more to adjust than just perception.

Longer holds would help. Making firms stand behind the debt they use would help (at least require them to pay back the mgmt fees they’ve collected when a company defaults). Transparently connecting fees to performance would help. Ending preferential tax treatment for carry would help. Forcing PE bros to actually work inside operating businesses they control would help.

I think the industry is heading for a bifurcation. The mega-funds will keep getting bigger. They’re powerful and political and will dominate fundraising. At the other end, lower-middle-market firms will keep creating real value by taking small businesses to the next level. The middle will get squeezed. You already see it… middle market firms selling stakes in themselves to the big guys (just another PE deal).

The real bottleneck going forward won’t be capital or deals. It will be operators. Financial engineering has been competed away. Sourcing has been automated. Spreadsheets can be done with AI (or will be soon). What actually creates value now is people who know how to run, fix, and grow businesses.

That’s a good thing, I think. The emphasis isn’t even really on operators so much as it’s on creating real value. Maybe PE bros need to lose the deal sleds for boots and become operators themselves…

Which raises an uncomfortable question for private equity: if great managers will create more value in the future, why do they keep giving most of the economics to spreadsheet people?

I think for PE’s next chapter, you will see some corrections, and I think those will be great. I think time horizon will be forced longer. You’ll see fewer 3–5 year windows and more 5–7. I hope that goes to 7–10; maybe it will.

For my money, the lower middle market is the place to be for the foreseeable future in the PE ecosystem. There, it’s genuinely helpful to equip companies with new tools, sophistication, and access to capital that they may or may not have ever been exposed to.

“Launching” these smaller businesses to the next level is valuable to all of us so long as it doesn’t end up in the never-ending cycle of selling from PE firm to PE firm to continuation fund and so on…

Despite the dour assessment, private equity isn’t evil. It’s just a tool, a strategy. Or it’s supposed to be.

There are always good and bad firms, good and bad people and so on. Good ones exist for sure. But that is just not the dominant flavor anymore.

The GP captures upside through fees and carry while transferring downside to LPs, lenders, workers, and the state. This is a structural free option.

Private equity is the only industry where you can lose other people’s money, fire workers, default on debt and still become personally richer.

It has generated a commoditized wealth-extraction machine that increasingly shapes society without accountability.

And I don’t think anyone wants to live in a society run by spreadsheet aristocrats.

English

The Salary Negotiation That Taught Me Everything In 2025

Candidate: "I need 100,000 per month."

HR : Our budget is 60,000 per month.

Boss: "Pass. Too expensive."

HR almost moved on. Almost.

But HR asked one question: "What would make 60,000 not work for you?"

Candidate : "Honestly? Nothing. I have loans, rent just went up, and I'm tired of being underpaid because I'm 'still learning.' I know my worth now."

HR went back to his boss.

Showed them the cost of leaving the role open another 3 months. The lost productivity. The team burnout. The recruiter fees if we went external.

It was over 50,000.

The boss accepted.

Here's the part that still gives the HR chills: Six months later, she told HR she had another offer for 130,000 per month but turned it down because they were the only company that fought FOR her, not AGAINST her.

Candidates remember who believed in them. They remember who negotiated IN GOOD FAITH versus who played games.

Stop treating salary negotiations like a battle to win. Start treating them like the first test of your company culture.

Because if you can't advocate for someone BEFORE they join, why would they believe you'll advocate for them AFTER?

English

Levels of CFOs…

Bookmark if you are hopeful to be a CFO or are just starting out as one. More context at the end…

Level 1: Perform the basics

Close the books, report the numbers, manage vendor payments, collections, etc.

Level 2: Improve the basics

Reduce time to close, reduce working capital, value add reporting package

Level 3: Drive cost discipline

Organizational leadership on cost management, proactively exploring and reducing expenses in all departments, working close with BU leaders to reduce low/no ROI costs

Level 4: Drive operational improvement

Identify and report KPIs to drive P&L efficiency, work through capex underwriting alongside P&L leaders, active vendor management for efficiency (beyond reduced cost), improve P&L to better align with business

*Sometimes this is official, sometimes unofficial. It seems more and more CFOs are expected to be directly involved operationally, sometimes with formal oversight

Level 5: Lead transformational initiatives

Lead due diligence for acquisitions, drive integration for acquisitions, new system implementations, restructuring,

Level 6: Strategic partner to CEO

Near-daily thought partner, heavy Board interaction and involvement, clear #2, “CEOverflow”

This is Buffett-Munger partnership level.

—

The above list of examples isn’t exhaustive, but gives you a sense of what each level looks like.

In my opinion, private equity is looking for at least a Level 4 CFO.

I’ve seen Level 3s but usually that’s because either a) there is a complementary team or b) they inherited him/her and things are fine atm.

Level 1/2 are more like controllers- they typically exist and smaller mom and pops who need a bookkeeper type leader they can count on.

PE boards love Level 5 CFOs. At that level, you are demonstrating tangible value add above and beyond and prove you are a leader who can execute and drive change.

I don’t know that PE cares as much about Level 6 but IMO it is what separates great from the best

No CEO is so universally brilliant that he can do it on his own. He needs partners he can trust and the CFO is uniquely positioned.

The CEO/CFO can divide and conquer. While CEO manages the business leaders, the CFO can cover the blocking and tackling of running the business.

Because they have distinct buckets, there is less conflict of interest. You can have objective conversations about shutting down a business, funding a project or making an acquisition.

The perspective is also unique. Typically only the CEO/CFO have both a birds eye view of the business and complete information.

So while it may not be recognized in the Board room, being a true partner to the CEO is the highest level of CFO.

English

ASSOCIATE’S TOOLKIT

Well the integration playbook ran

Here is the actual end of the rope

Comment, like, follow (so I can DM you) to get

English

1. Your payment terms are too generous.

Net 30 becomes net 60 real fast when you don’t enforce it.

• Shorten your terms

• Incentivize early pay

• Follow up consistently

Slow collections are one of the fastest ways to kill cash.

English

Most cash flow problems are self-inflicted.

After working with 100+ SMBs, I’ve seen the same mistakes over and over.

Here’s how to prevent cash flow issues before they become emergencies:

English

Corporate Rules for Happy Life In 2026

1. Trust nobody.

2. What happens in office, remain in office. Never take office gossips to home and vice versa.

3. Enter office on time, leave on time. Your desktop is not helping improvement in your health.

4. Never make GF/BF and/or brother/sister in office. It will always backfire.

5. Expect nothing. If somebody helps, feel thankful. If not, you will learn to know things on your own.

6. Never rush for position. If you get promoted, congrats. If not, it doesn't matter. You will always be remembered for your knowledge and politeness, not for your designation.

7. Never run behind office stuff. You have better things to do in life.

8. Avoid taking everything on your ego. Your salary matters. You are being paid. Use your assets to get happiness.

9. It doesn't matter how people treat you. Be humble. You are not everyone's cup of tea.

10. In the end nothing matters except family, friends, home, and Inner peace

English

How to Recognize a Bad Boss in 2026

1. Wasting time by calling unnecessary meetings

2. Creating pressure by labeling everything as “urgent”

3. Expecting results without giving clear instructions

4. Overloading employees with work beyond their capacity

5. Creating anxiety by asking for updates every hour

6. Destroying team trust through micromanagement

7. Failing to share important information on time

8. Forcing employees to work even on holidays

9. Judging performance without providing proper training

👉 These behaviors don’t just kill employee motivation,

👉 they gradually destroy the entire team’s performance.

A good boss isn’t someone who only gets work done —

a good boss provides direction, builds trust, and respects both time and people.

English