ทวีตที่ปักหมุด

English

How My Dictate?

1.4K posts

Today, the Commission issued an order allowing broker-dealers to pledge a diversified basket of Russell 1000 and/or S&P 500 equities as collateral when borrowing securities. More info below. ⬇️

AMAZING! In true @SECGov fashion… They finally figured out they can’t beat us so they CHEAT INSTEAD. Delete the evidence and it never happened, right? Interesting timeframe you all chose. Three years. It’s almost laughable. Nice try. What made you think this was a good plan, @SECPaulSAtkins? A “New SEC”? Nah. You’re as corrupt as ALL of your predecessors! Keep it up. You all can weaponized this system till the cows come home. WE ARE NOT GOING AWAY. #MMTLParmy $MMTLP $MMAT #Relentless sec.gov/newsroom/press…

JUST IN: SEC approves plan for deletion of CAT (Consolidated Audit Trail) data.

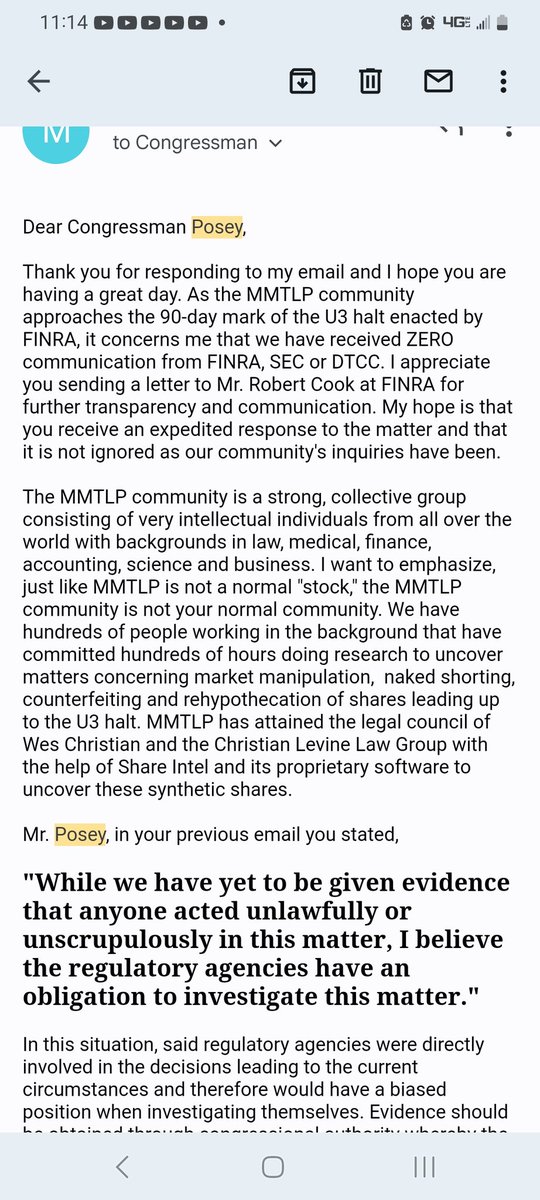

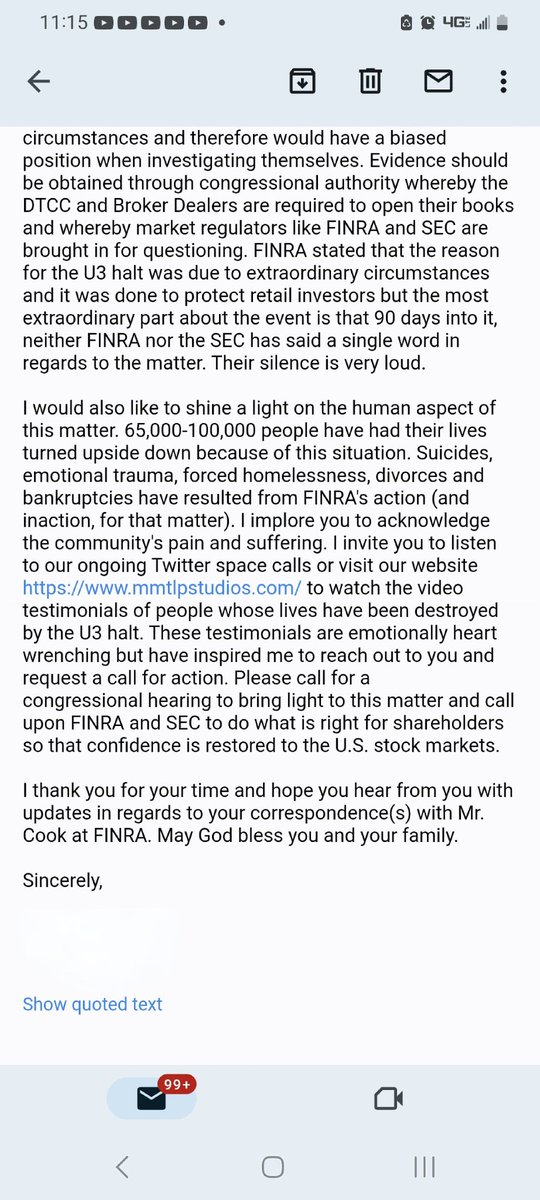

@JDVance #mmtlp Vice President J. D. Vance, you previously raised concerns with the SEC on MMTLP—those issues remain unresolved. Now that you are leading efforts to investigate fraud across the government, this warrants renewed attention. If shares were sold without being properly borrowed or delivered, that may violate Regulation SHO and potentially Rule 10b-5 (securities fraud). If profits were generated from synthetic or unsettled shares, this also raises serious concerns under 26 U.S.C. §§ 7201 and 7206—potentially defrauding the U.S. government of tax revenue. Over 65,000 American families were impacted and denied the ability to exit positions. This is not just a market issue—it is a test of enforcement, transparency, and accountability. A full audit of share counts, fails-to-deliver, and tax reporting is warranted.

The SEC seems to be saying, in effect, “15c2-11 is an OTC equity rule, let’s stop pretending it is a general quotation rule for every security” BUT… What I find even more interesting is Commissioner @HesterPeirce longer statement 2 hrs ago and this part: “They highlighted that the 2020 rule amendments relied entirely on OTC equity data and did not even mention the term “fixed income” once. They noted that they were unaware of Rule 15c2-11 ever being applied to fixed income securities. And they warned that the application of the rule would gravely harm the fixed income market and investors, with no discernable reduction in fraud” The keyword is “fixed income” #MMTLP There is a more strategic interpretation in my opinion. More to follow, thank you Suzy! sec.gov/newsroom/speec…

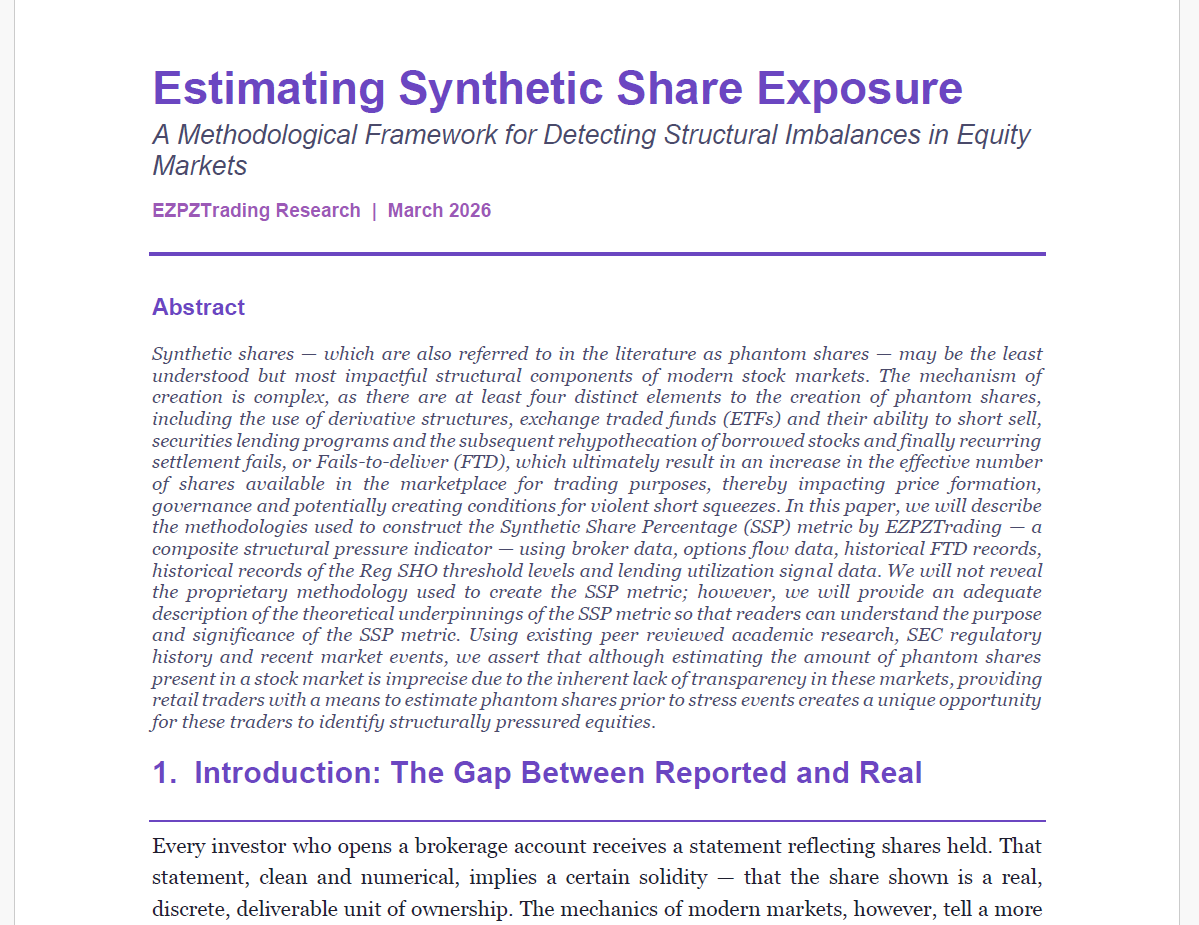

MMTLP vs. SEC #FAFO #Relentless 👀👇 RED FLAGS across the board. No Oversight, Transparency and no answers. Facts based on SEC FOIA data. SEC vs. MMTLP FOIA Analysis (12/2022–2/2026) A quantitative breakdown of systemic disparities in FOIA processing. Volume Comparison: MMTLP Is a Small Slice — But Treated as an Outlier. MMTLP requests represent ~5–6% of all SEC FOIA activity, a meaningful volume, not a fringe anomaly. Yet the processing outcomes diverge dramatically. Disclosure Rates: The Core Red Flag SEC Overall Disclosure Rate (Granted in Full + Granted/Denied in Part) = 11.66% MMTLP Disclosure Rate = 0.043% What this means: MMTLP FOIAs are ~270 times less likely to result in any disclosure than the SEC’s baseline. This is the single most statistically significant indicator that MMTLP requests are being handled under a materially different internal process. “Other Reasons” Classification: A Massive Outlier SEC “Other Reasons”. 15,239 out of 21,978 closed → 69.3%. MMTLP “Other Reasons”. 857 out of 1,207 closed → 71.0%. While the percentages look similar, the context matters: • For the SEC overall, “Other Reasons” is spread across thousands of unrelated topics. • For MMTLP, the majority of all closures fall into this opaque category (MMTLP & NBH). • Combined with the near‑zero disclosure rate, this suggests “Other Reasons” is being used as a catch‑all to avoid releasing records. Denials in Full: MMTLP Is Disproportionately Blocked. MMTLP requests are denied outright at a 40% higher rate than the SEC baseline. B7 Exemptions: Criminal / Enforcement Shielding. FOIA B7 exemptions apply to law‑enforcement‑related records. SEC B7 Exemptions - 1,671 total MMTLP B7 Exemptions - 285 total But here’s the key: MMTLP represents 5.7% of all FOIA requests but 17.1% of all B7 exemptions. This is a 3× over‑representation. That strongly suggests: • MMTLP‑related records are being treated as part of an active or sensitive enforcement matter. • The SEC is shielding these records under law‑enforcement exemptions at a rate far above normal. Year‑Over‑Year Trends: The Spike in 2025. MMTLP FOIA requests jump dramatically in 2025: • 1,319 requests in 2025 alone • That’s 62% of all MMTLP FOIAs since 2022 Yet disclosures remain almost nonexistent. This is also the period where: • Aggregation (bundling) practices increased, identified on 3/28/2025 • “Other Reasons” surged • B7 exemptions spiked The timing aligns with the community’s intensified push for transparency — and the SEC’s increased resistance. Statistical Summary: What the Data Shows MMTLP FOIAs are: • 270× less likely to receive any disclosure • 40% more likely to be denied outright • 3× more likely to be classified under B7 law‑enforcement exemptions • Overwhelmingly closed under “Other Reasons” with no transparency • Almost never granted in full (3 total in 4+ years) This is not random variation. The probability of these disparities occurring by chance is effectively zero. The data strongly supports the conclusion that: 👀👉"MMTLP FOIA requests are being processed under a materially different internal policy or directive within the SEC." This ☝️ "processing" has been requested by FOIA - Acknowledged 3/10/2026, Closed 3/11/2026, NO EXPLANATION by the SEC. Refer to PAL. What This Implies About SEC Internal Handling Based on the patterns: • There is likely an internal enforcement matter, investigation, or sensitive review tied to MMTLP. • FOIA staff appear to be instructed to withhold, aggregate, or divert these requests. • The near‑zero disclosure rate is incompatible with normal FOIA operations. • The heavy use of B7 exemptions suggests ongoing or past enforcement activity that the SEC has not publicly acknowledged. These are not opinions or interpretations—they are documented facts, drawn directly from the SEC’s own monthly FOIA disclosures and aggregated against a tiny, non‑trading placeholder security that only became tradable because two market makers unilaterally activated it in October 2021. From that moment forward, every consequential action, from the creation of a tradable ticker, to the handling of corporate actions, to the ultimate U3 trading halt imposed by FINRA on December 9, 2022, occurred without any input, consent, or participation from the companies involved. Despite this, both FINRA and the SEC continue to publicly frame their decisions as “retail investor protections.” Yet the data tells a very different story. When you combine these patterns with the fact that the issuers had zero control over the trading, halting, or regulatory decisions that affected their shareholders, the picture becomes unmistakable: This is not investor protection. This is a regulatory failure that has harmed retail investors for more than 1,090 days. And that is why the fight continues—because the numbers, the timelines, and the agencies’ own records all point to the same conclusion: The MMTLP community was subjected to actions outside the issuers’ control, outside normal regulatory transparency, and outside the standards of fairness that FINRA and the SEC claim to uphold. Share and support us in this ongoing effort. We thank you! MMTLP.AI MMTLPresources.com @palikaras @johnbrda @annvandersteel @MaureenSteele_ @petersantilli @TheRobbCarter @kshaughnessy2 @KristiTalmadge @kristie_dugan @FinancialCmte @BankingGOP

Dear @SECGov and @SECPaulSAtkins 🚨🚨🚨1141 days🚨🚨🚨 January 23, 2023 - TODAY 💡Next move - Contact Guinness Book of World Records to formally enter NextBridge Hydrocarbons as the longest S-1 process in the history of S-1 submissions. Absolutely disgusting. DO YOUR DAMB JOB, already! $MMTLP $MMAT #MMTLParmy #WhatstheShareCount

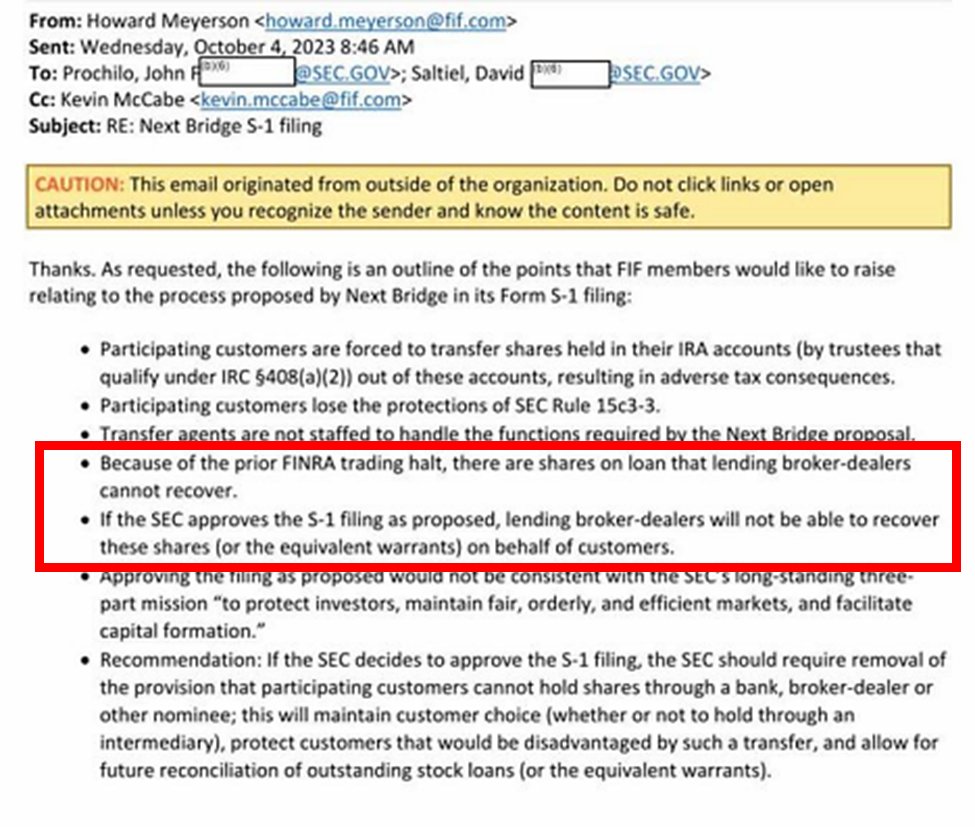

"Under investigation"?!? ... The @SECGov has weaponized their "investigations" to deflect transparency for decades. The MMTLP Army has exposed the SEC as CO-CONSPIRATORS in the defrauding of 65k+ investors who did NOTHING WRONG. #RICO WE HAVE THE RECEIPTS!!! #FOIA But, instead of providing the transparency investors need to bring about resolution, the SEC continues to OBSTRUCT to protect their own CRIMINAL BEHAVIOR. Issuers DID NOT sell counterfeit shares into the market. Investors DID NOT sell counterfeit shares into the market. Broker-Dealers (FIF) have admitted they can NOT DELIVER on their OBLIGATIONS...because their customers are holding COUNTERFEIT SHARES!!! THEY PUT IT IN WRITING...👇👇👇 x.com/JunkSavvy/stat… CONGRESS HAS KNOWN FOR 3 YEARS and NEEDS TO STOP BEING PART OF THE COVER-UP and BE PART OF THE SOLUTION!!! Accepting another bullshit "under investigation" excuse WILL NOT WORK THIS TIME. DO YOUR JOB. INVESTIGATE!!! @RepDonaldsPress WE ARE NOT GOING AWAY!!! #Relentless MMTLP MMAT TRCH

Based upon this exchange, the @SECGov reached-out to my office to inform me that this is currently under investigation. I proudly joined my colleagues in demanding MMTLP transparency back in 2023 and I thank the Trump admin–SEC for fighting to ensure that this issue is resolved. We will continue to monitor the situation.

$MMTLP High-res clips from “Ask Byron Anything” LIVE at Versailles Restaurant in Miami, FL. Where @johnnaarintl directly addresses Rep. @ByronDonalds on #MMTLP transparency! Download & use this powerful moment to your advantage. Huge thanks to @johnnaarintl and @thedocespo! 💪