Cluelessbio

454 posts

Cluelessbio

@cluelessbio

Propably better off investing in an index fund | Prescribe side

Just hit another $1 million month to date! The market’s been strong, and I’ve been working to capitalize on the momentum. It wasn’t about one name , my biggest winner was $96K, while the biggest loser month to date was $80k (thanks to $OSCR giving back a bit from last month’s gains) while 2nd biggest loser was 18k! Also, I want to say a big thank you for helping me cross 50K followers , truly humbled and grateful. And finally, my motto is always “The more you give, the more you get back.” If you’ve made some gains this month or this year, consider giving a little back to someone in need. It’s one of the best investments you’ll ever make.

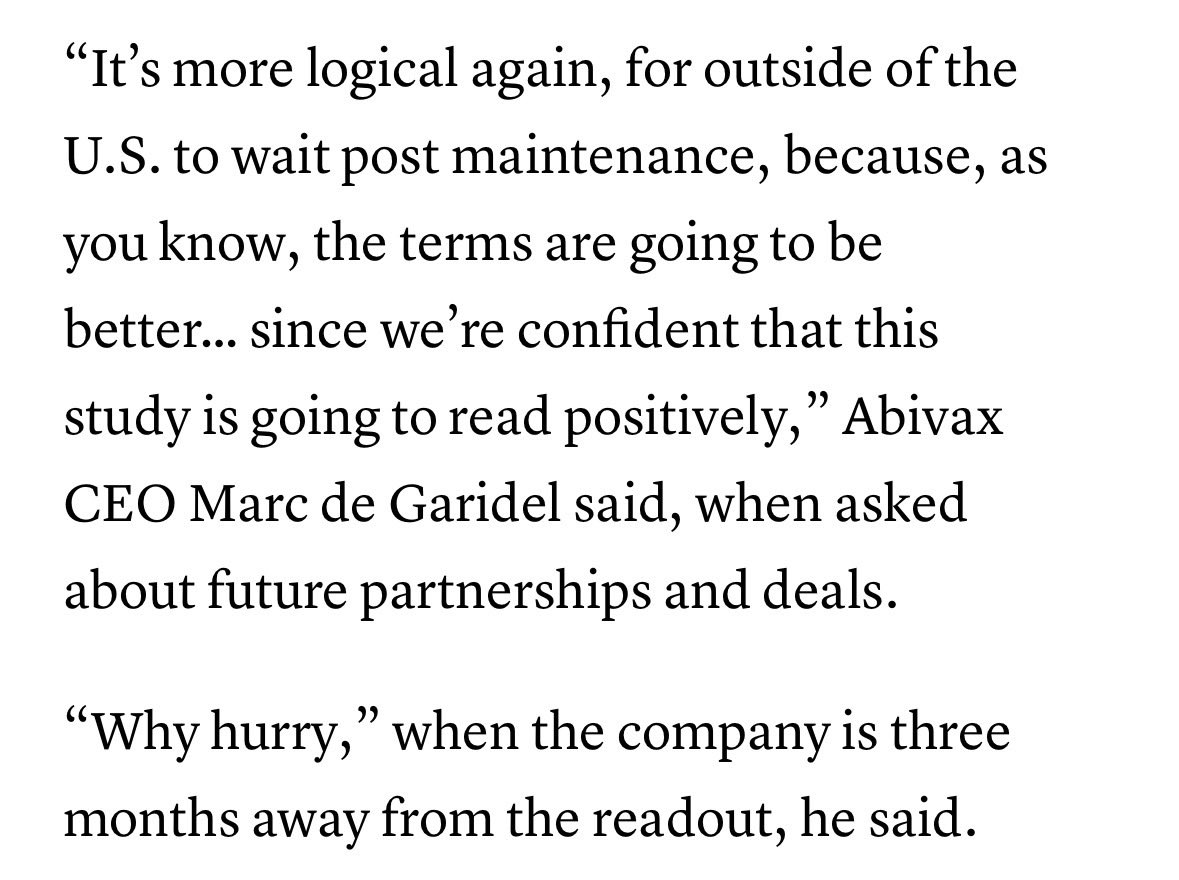

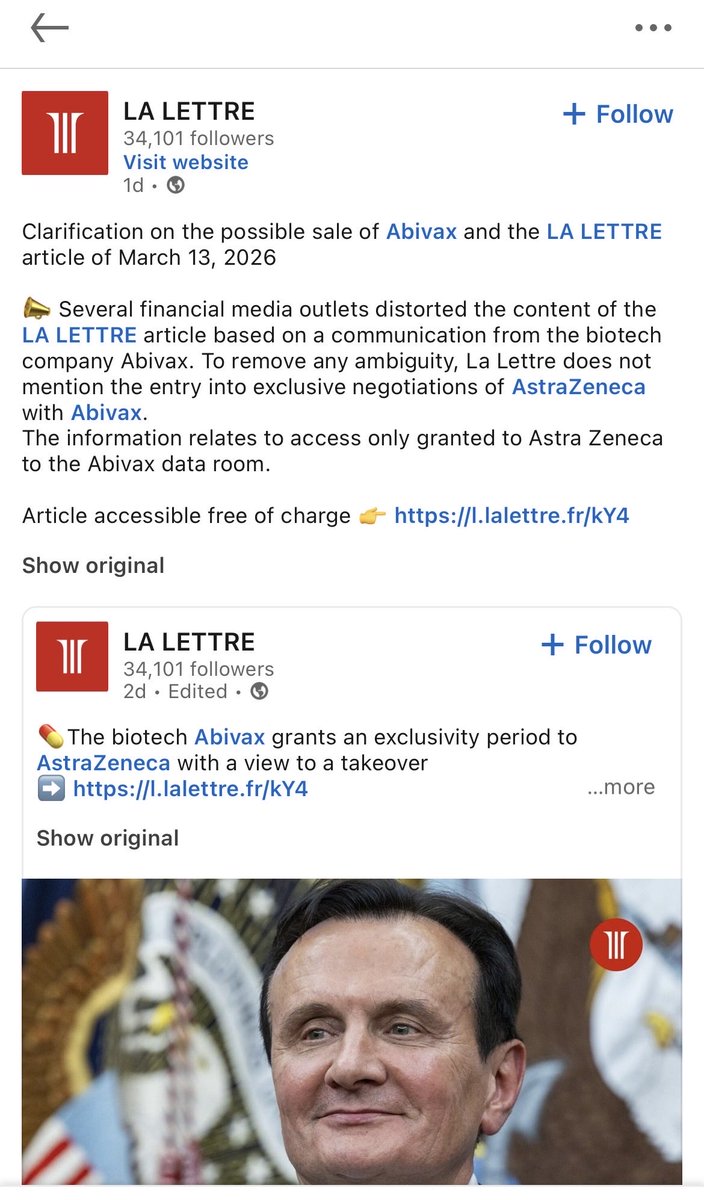

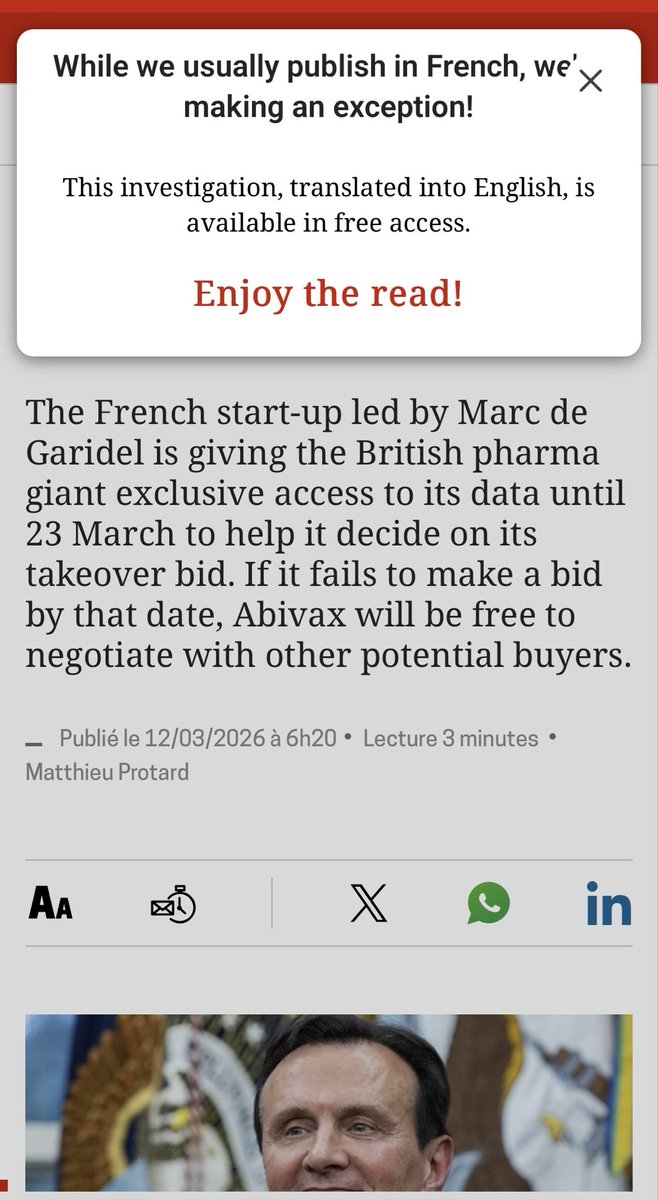

la lettre doubles down $ABVX

$copn Cosmo pharmaceuticals Clascoterone (breezula/cb0301) will sell ok, but is a dud. „500 % improvement relative to placebo“ is a red flag way to report results. Also takes 8 hours (!!) for drug to be hydrolyzed, so it has systemic side effects.

I understand the enthusiasm around $ABVX but maybe $EQ is being overlooked. Same MoA and maybe even better product with mid-2026 trial readout. What am I missing?