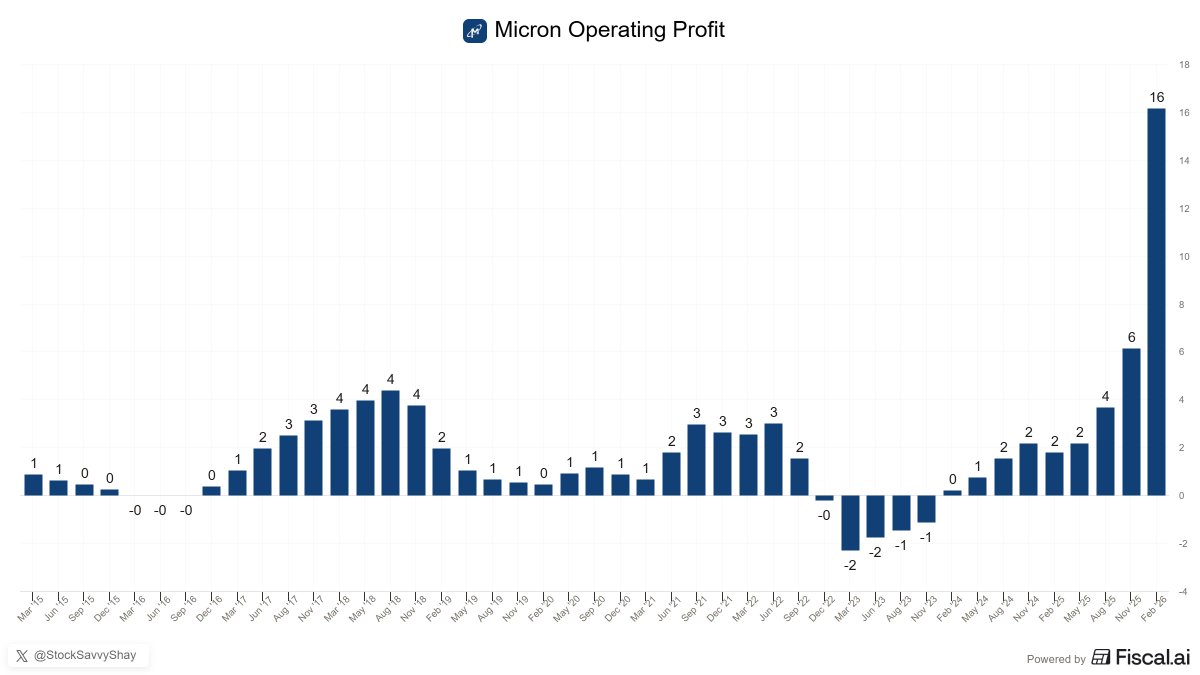

This AI cycle is fundamentally different from every prior memory supercycle in $MU history.

Past supercycles were driven by unit volume growth with more phones + servers buying largely commoditized DRAM but but this one is a capacity-constrained cycle where HBM sells at ~5x conventional DRAM ASPs.

Hyperscalers are willing to pay whatever it takes because the real cost is leaving massive GPU clusters underutilized.

That is how Micron ends up producing $16B of operating profit in a single quarter.

Shay Boloor@StockSavvyShay

$MU ABSOLUTELY CRUSHED THEIR EARNINGS • Revenue $23.9B vs Est. $19.5B • EPS $12.20 vs Est. $8.73 • Net Income $14.0B vs Est. $10.5B • Gross Margin 74% vs Est. 69% Q3 Guide • Revenue $33.5B vs Est. $23.3B • EPS $19.15 vs Est. $10.77 • Gross Margin 81% vs Est. 71%

English