ExAdTechQuant nag-retweet

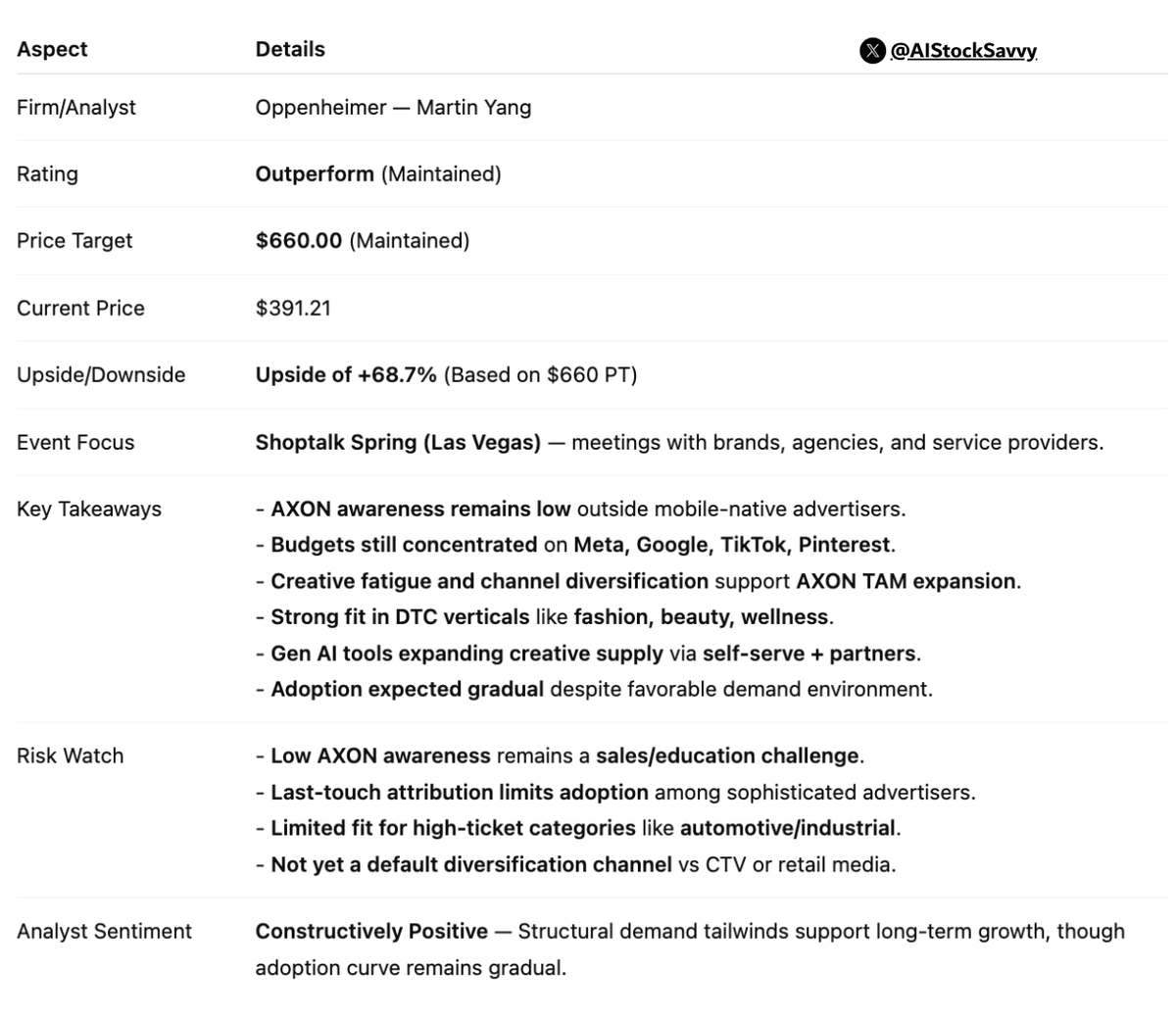

$APP | 𝐀𝐩𝐩𝐋𝐨𝐯𝐢𝐧: Oppenheimer reiterates 𝐎𝐮𝐭𝐩𝐞𝐫𝐟𝐨𝐫𝐦, maintains 𝐏𝐓 𝐚𝐭 $𝟔𝟔𝟎

Analyst sees favorable structural demand tailwinds, though AXON awareness and adoption remain early.

English

ExAdTechQuant

444 posts

@Ad_Quant

not financial advice

What is $APP fair value? Here is a simple analysis using PE multiples to highlight that $APP is the CHEAPEST in its sector and even if it conservatively trades at a sector multiple, it should be a $700 stock. The analysis adjusts PE multiples for FCF conversion and growth rates.