George Noble@gnoble79

Private credit didn't blow up because of Blue Owl or bad software loans or AI disruption.

Those were SYMPTOMS.

The disease is the same one I've seen 3 times in 45 years on Wall Street:

Too much money, too much leverage, too little discipline, and a financial product sold as "safe" to people who didn't understand what they owned.

Private credit grew to $3 trillion on a simple lie - that you could earn 9-10% yields with "semi-liquidity" on assets that have no liquid market.

That's not investing. That's volatility laundering. And the Street dressed it up beautifully.

"Private credit." Sounds so exclusive, so sophisticated. Illiquid loan sharking would be more accurate.

And don't get me started on "private equity", another Wall Street rebrand designed to make LEVERAGED BUYOUTS sound like fine wine. They changed the name because the old one scared people. The risk didn't change. Just the marketing.

Wall Street has always been brilliant at one thing: rebranding risk as exclusivity and selling it to people who don't know what they're buying.

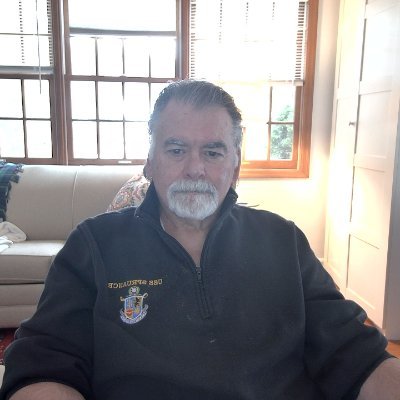

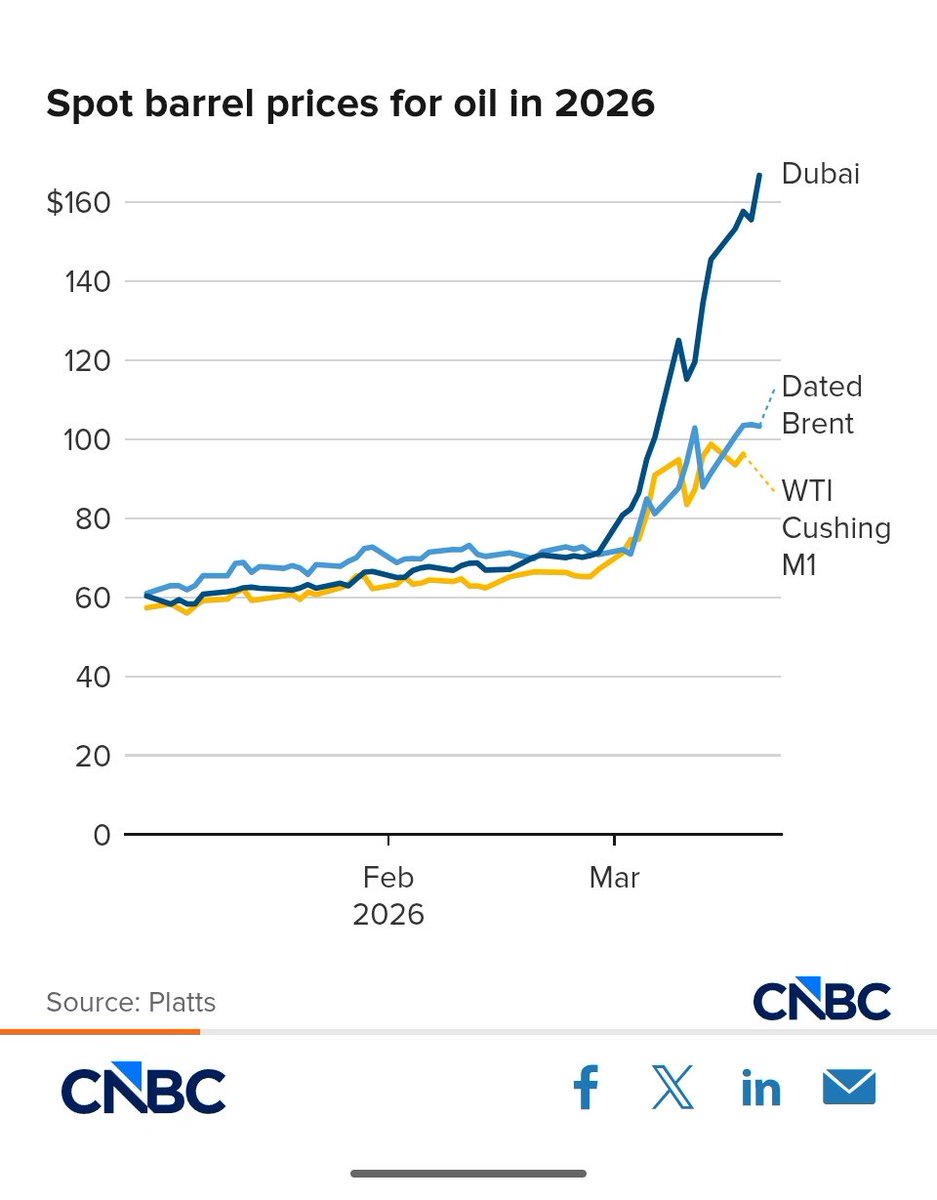

Now add oil at $113 a barrel and watch the whole thing come apart.

The Strait of Hormuz is shut. The IEA is calling it the largest supply disruption in the history of the global oil market. The Fed held rates steady yesterday and the market just RIPPED AWAY expectations for even a single cut this year.

Oil is the fuse. But the TNT was packed years ago.

Oil above $100 means inflation stays sticky. No rate cuts. Every overleveraged borrower inside these private credit portfolios gets squeezed harder every single month.

Interest coverage ratios deteriorate. Defaults tick up. Valuations get marked down.

And when valuations drop, the leverage stacked on top of that leverage (the "back-leverage" that banks provide using those same loans as collateral) starts to unwind.

And JPMorgan already started.

They marked down software loan collateral and restricted lending to private credit funds. When the biggest bank in America pulls back, that's a SIGNAL.

High-yield spreads just surged to 470 basis points. The widest in years. Credit markets are screaming what equity markets haven't fully heard yet.

I've watched this exact pattern before.

- Junk bonds in the '80s

- Dot-com leverage in 2000

- Structured mortgage products in 2007

The product changes every time but the architecture never does:

Wall Street creates something complex, sells it as safe, layers leverage on top, markets the yields to retail investors, and collects enormous fees on the way in.

Then something breaks and the gates go up.

The people who built the machine are fine - they already got paid. The people who bought the brochure are trapped behind locked doors.

$265 billion in market cap already wiped from the major PE firms. I don't think we're close to done.

And you know what? That's FANTASTIC.

Perhaps we'll finally get some real price discovery. Just say no to mark to model.

Holders of this fine merchandise will get the returns they deserve. The pension funds, endowments, and insurance companies that piled into this garbage should take the hit. No bailouts. NONE.

This nonsense has gone on far too long and moral hazard is the predictable result.

The only way to end this insanity is to let Mr. Market operate.

Allow price discovery. Allow bankruptcy. No more money printing. No more crony capitalism. No more extend and pretend.

Blow it all up. That is the only way.

"But what about the individuals who get hurt!"

Better to take the hit now and reset than continue down this road. Hyper-financialization is destroying our economy and enriching the fortunes of the few. This must stop. NOW.

But I have little confidence it will. We'll get more of the same:

Rule changes. Special accommodations. The inevitable big ease will come.

Count on it.

AND BUY GOLD