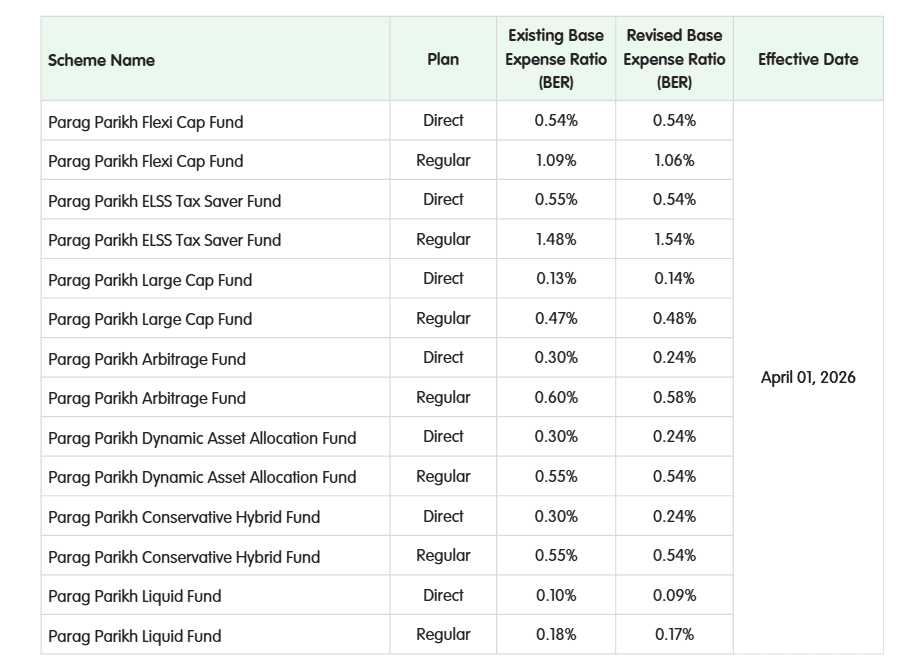

SEBI 2026 MF regulations require TER to be disclosed as four components: Base Expense Ratio, brokerage, transaction costs, and statutory levies. Each reported daily, annualized. The intent is good. Investors should see what they're paying for. But there's nuance that may get lost. Here's how to make sense of it: Brokerage scales with trading volume, not AUM. So do the variable statutory levies - STT, GST on brokerage - and exchange/clearing charges. All are incurred only on days when the fund transacts. Annualizing a single day's transaction costs assumes that level of activity repeats every day for a year. On a heavy trading day, this produces an enormous number. On a quiet day, these components drop to near zero. I pulled this FY's first week's AMFI data for open-ended equity schemes. Two examples: Mirae Asset Arbitrage Fund (Regular): 14% TER on April 1, down to 0.93% by April 3. BER is 0.79% throughout. The difference is entirely transaction costs and statutory levies from one day of likely derivatives activity. Kotak Nifty Midcap 150 Index Fund (Regular): 0.88% on April 1, 3.5% on April 2 (likely rebalancing), 0.63% on April 3. The BER is stable and reflects the actual cost structure of the fund. The variable components are noise at the daily level - they only converge to something meaningful when averaged over a full year. There's a second issue. The new TER isn't comparable to the old TER. It now includes brokerage, STT, exchange charges, and GST - none of which were in the old disclosed number. The old TER was closer to what's now called BER, but even that isn't a clean match: the expense line items and caps have been restructured. There is no like-for-like mapping. Screeners and comparison tools that sort on TER will need to account for this. An interesting side-effect: TER minus BER is now a daily proxy for trading activity by each fund. That data was never available before at this granularity. Whether SEBI intended it or not, anyone tracking fund behavior just got a new metric.