Vashistha Iyer retweetledi

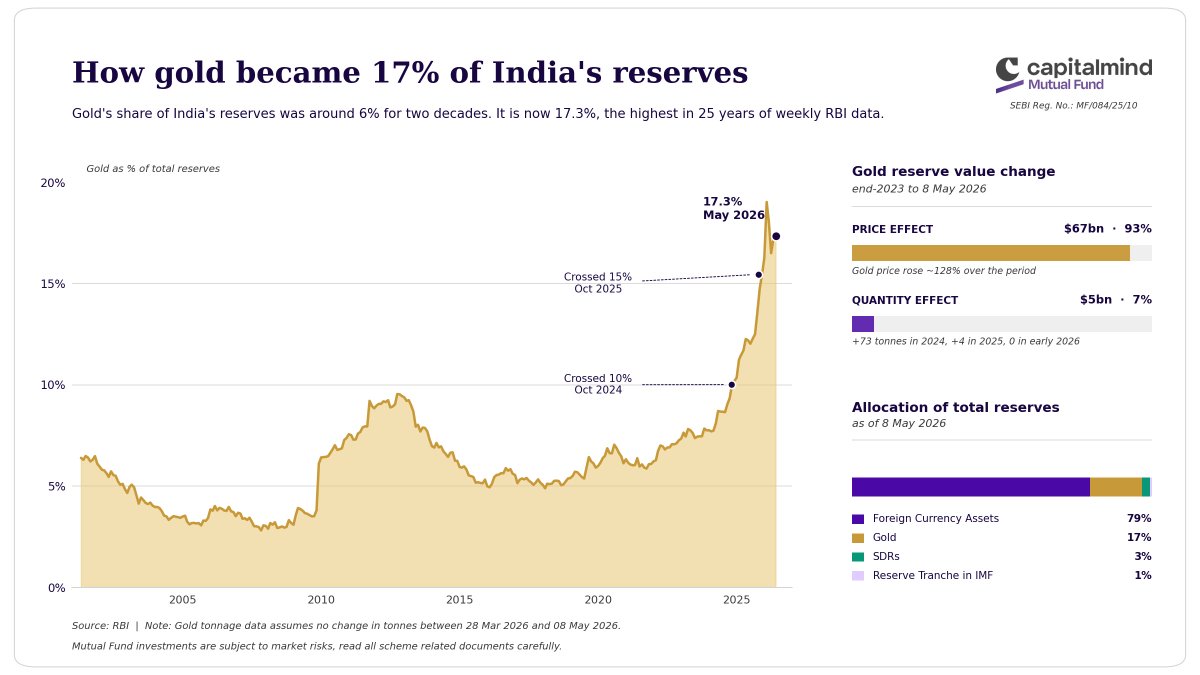

Has RBI been buying gold aggressively?

India's gold reserves just hit a 25-year high at 17.3% of total forex reserves.

Of the $72bn rise in gold's reserve value since end-2023, 93% came from price appreciation and only 7% from buying more gold.

RBI bought only 73 tones in 2024, 4 in 2025, and nothing in 2026.

English