@toy59496 Are you now bullish on $4DX?

Anyway, looks like error 3 here is the bull case for $LDX.ax

English

99Opportunities

1.2K posts

@99Proble

Everything is awesome. Here for the stock chat.

$4DX.AX : Analysis & Valuation x.com/toy59496/statu… I've reviewed this company as I was concerned I got it wrong 6 months ago. Looking at it now I did get it wrong, and I didn't... I misunderstood that it is not intended as a substitute for a CTPA or VQ scan but rather additional interpretation from the millions of CT scans that are done every year in any event. It is the first to market with this technology, which is an advantage. On the other hand I was rightly cynical about the technology in that clinical validation is based on just 16 patients. I view it as grossly overvalued at the moment. But remember I was wrong 6 months ago... Briefly 1. $3.5B market cap on $5.85M revenue. ~600x P/S. 2. The 27x surge from $0.24 to $6.50 due to Philips distribution deal (US10M minimum), and 6 elite US hospitals in 7 months -Stanford, Cleveland Clinic, UCSD, Miami, UChicago, and now Mayo Clinic. 3. The valuation is extreme by any standard: a) Trades at 12x the multiple of Pro Medicus, the most expensive medical imaging SaaS on earth, b) 38% above Bell Potter's A$4.50 target (who ran the $150M capital raise - conflicted) - 150% above Jefferies' $2.50 target, c) Ord Minnett independently downgraded to SELL in Feb 2026 4. Key risks the market is ignoring: a) Reimbursement runs on a temporary Category III CPT code (5yr lifespan), b) Mayo deployment is a 90-day trial, explicitly "not financially material", c) Clinical validation based on just 16 patients, no large independent outcome studies, d) H1 FY26 revenue just $2.9M while net loss widened to $154M, e) FDA 510(k) pathway is "substantial equivalence" - not rigorous efficacy proof. 5. The technology is legitimate. FDA cleared, Medicare reimbursed, adopted by America's best hospitals. The addressable market (1M+ VQ scans/year, US$1.1B) is real. But at ~600x trailing revenue and ~86x FY27 consensus, the stock prices in near-flawless execution for years. 6. Analyst fair value range: A$2.50-$4.50. Current price: A6.23. Not financial advice. DYOR.

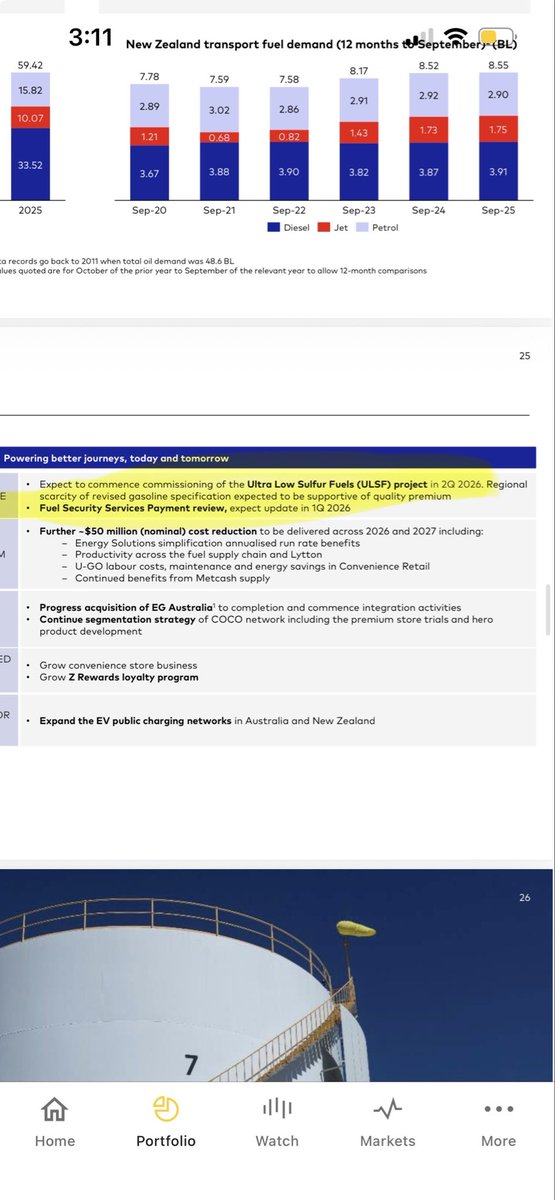

BREAKING: Energy Minister Chris Bowen has ordered the release of high Sulfur-content fuels to ease pressure in the regions.

This is a war that impacts the world 🌎: Australia’s diesel supply chain is showing early signs of strain as tightening Asian fuel markets collide with the country’s heavy reliance on imports and long inland distribution networks. More on @Kpler #OOTT