@f8434784752 @BioValues 2. Is also difficult to measure as in Erlangen some patients were in remission but still had proteinuria due to renal damage

English

B boy19

230 posts

The $AMD and $GFS CPO announcement is probably bigger than markets expect for $SIVE. With the news, it's likely $SIVE lasers power $AMD's CPO program. Either through two potential paths: 1. Enosemi (AMD's in-house PIC design post-acquisition). Enosemi's chiplets are fabbed at GF but for the ELS, $AMD could source it from multiple players with $SIVE as the underlying multi-source laser source. 2. Ayar ( $AMD invested in March 2026, Series E). Ayar's SuperNova light source already uses $SIVE DFB laser arrays alongside $LITE. Ayar's SuperNova is the most likely first-gen CPO path for MI500 in 2027 given timelines and the enormous fundraise last month. That path already has $SIVE designed in alongside $LITE and they both appear with $GFS's slide. Enosemi becomes more relevant for 2028+ generations? Regardless, $AMD through Enosemi/Ayar needs lasers for their 2027 MI500 rollout... It seems likely Sivers ends up powering $AMD's CPO program as the light source since they're designed into Ayar. The $AMD / $GFS materiality looks large for Sivers.

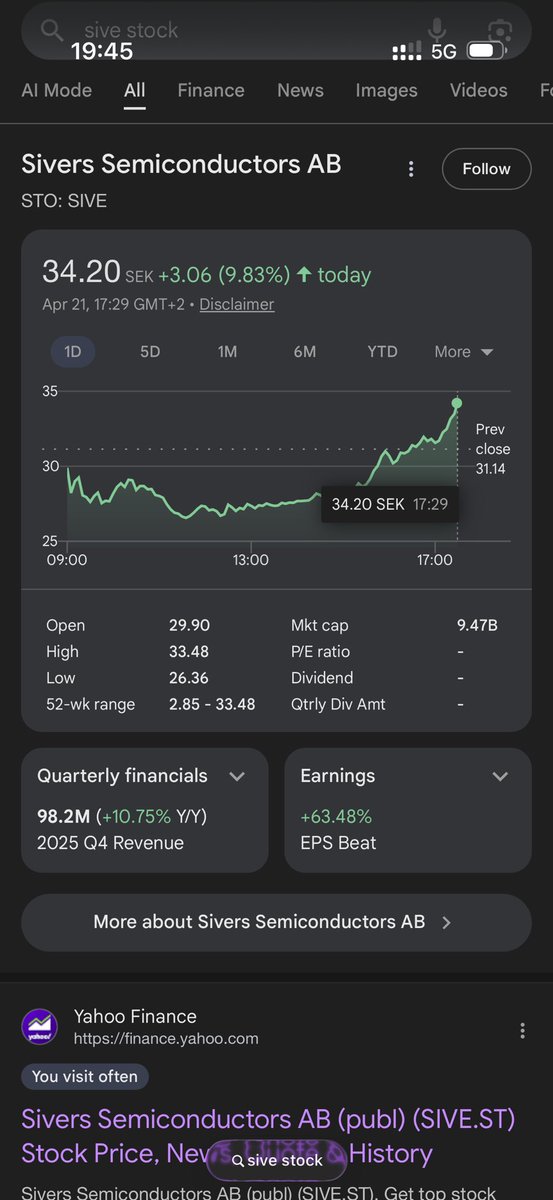

Is $SIVE overpriced ? What we know: Confirmed: • Jabil deal (1.6T LRO, Apr 15) • $POET integration • Win Semi ramp • $GFS CPO slide - only $LITE + $SIVE mentioned for lasers • CW-WDM with $LITE $COHR • NASDAQ dual listing in the works (Reuters) Unconfirmed but likely: • Amazon + Google -> $MRVL photonic fabric • $AMD - Ayar Labs (uses $SIVE lasers) • $NVDA adjacency via ecosystem Jabil alone per @aleabitoreddit model: 2027: $120M ARR 2028: $280M ARR 2029: $480M ARR Current MC: $935M Supply chain: $AXTI $TSEM $AAOI $COHR Catalysts: Apr 23 — Win Semi earnings Apr 30 — $AAOI $AXTI earnings May 7 — $GFS Day May 13 — $SIVE earnings Jun 16 — $JBL earnings Counter arguments: Analyst models are not guidance and could be wrong Execution risk is real. Win Semi qualification is mid-2026 Dilution risk exists. NASDAQ listing and growth capex need funding 2029 is three years away. A lot can change in laser supply chains What are your thoughts ? Sources: @aleabitoreddit @crux_capital_ @damnang2 @ParadisLabs @PhotonCap @StormDirac

The "Light Engine" Duel: Why Sivers Semiconductors $SIVE is $AMD’s Indispensable AI Bottleneck As of late April 2026, the AI infrastructure landscape has shifted into a "two-horse race." While the world focuses on the GPUs, the real battle is moving to the light sources that power them. A clear divergence in the supply chain has emerged: NVIDIA has locked in Lumentum, while AMD is consolidating around Sivers Semiconductors. The Strategy: NVIDIA/LITE vs. AMD/SIVE NVIDIA has signaled its dominance by integrating Lumentum (LITE) into its next-gen Rubin architecture. But AMD is taking a more specialized route. By returning to GlobalFoundries for the Instinct MI500's co-packaged optics (CPO), AMD has effectively chosen Sivers (SIVE) as its primary light engine. The "Total Redesign" Moat Why is Sivers likely the only light source for AMD? It comes down to architecture. Sivers’ Indium Phosphide (InP) lasers are natively built into the GlobalFoundries Fotonix process design kits (PDKs). For AMD to replace Sivers with a competitor like Lumentum or Coherent, it wouldn’t just be a simple swap—it would require a total redesign of the Photonic Integrated Circuits (PICs). In the high-stakes race to 2027, a redesign means months of delays that AMD cannot afford. Sivers isn't just a partner; they are "baked into" the silicon. The Massive Valuation Gap When you look at the market caps, the "upside" potential for Sivers is staggering: Lumentum (LITE): Currently valued at approximately $63.84 Billion. As a primary NVIDIA partner, it has seen a massive re-rating. Sivers (SIVE): Currently valued at approximately $925 Million (8.48B SEK). Lumentum is currently valued at nearly 70x the market cap of Sivers. While Lumentum is a massive incumbent, Sivers is the specialized pure-play bottleneck for AMD's AI future. As AMD ramps up the MI500 to challenge NVIDIA’s dominance, the market cap of its primary laser provider is positioned for a major re-rating to close this valuation chasm. Recent Catalysts for Sivers: The 1.6T Revolution: A massive new partnership with Jabil to develop 1.6T optical transceivers that are 2.5x more energy-efficient. Nasdaq New York Listing: Sivers officially announced it is evaluating a dual listing in the U.S. to capture tech-centric capital. Institutional Support: A recent 125 million SEK capital raise specifically to fund production for AI data centers. The Bottom Line If NVIDIA needs Lumentum to stay on top, AMD needs Sivers to even compete. As the market realizes that Sivers is the exclusive, "locked-in" on-ramp for AMD’s light-based compute, that $925 million valuation looks like a rare opportunity in a crowded AI sector. Financial Disclaimer The content provided is for general educational purposes and does not constitute professional financial, investment, or legal advice. #Sivers #AMD #NVIDIA #Lumentum #SiliconPhotonics #AIInvesting #MI500 #LightSpeedAI #GlobalFoundries

Just 1 month ago, journalists and media tried downplaying my $SOI and $RPI thesis. As “meme stocks that were set to crash” citing my WSB tag without analyzing the underlying thesis. They’re both up 100% and held their gains. Same is happening to companies like $SIVE. I never argue from authority… but since they’re going that route: I’m curious why… in their narratives they just leave out the fact I published fundamental AI papers in places like Nature with thousands of citations? Other the fact other analysts on X positive about $SIVE today have Ph.Ds from places like UC Berkeley and publish in the photonics space? It’s always the English or non-technical graduates that go out in the media and have the strongest opinion about CPO hyperscaler qualification cycles and supply chain mapping. It just feels like institutions hate it when a retail investors on X know what they’re talking about. A thesis should live and die based on merit, not the authority of who is comes from.