@nejatian Will the new Opendoor be resilient to handle any kind of housing backdrop? Is it being built with that goal?

English

Akash Trips

142 posts

@akashtrip03

Your life expands in proportion to your courage | Discerning, decisive and patient Value Investor (at least hopes to be one)

Newswrap: TSMC Earnings, Nvidia I'm 'No Loser' CEO on Dwarkesh Podcast taekim.substack.com/p/newswrap-tsm…

$NUAI is expanding its Texas Critical Data Centers campus with an LOI to acquire 54 additional acres. The strategic corridor strengthens direct power access and supports behind-the-meter infrastructure. 🔗 newerainfra.ai/news/

I just killed my bullish thesis on $IREN and out of every position. In this video I walk through the exact trigger that flipped it into a potential bear cycle, and why I see a possible 40% downside over the next few months. I hope I’m wrong. Here’s the full breakdown 👇

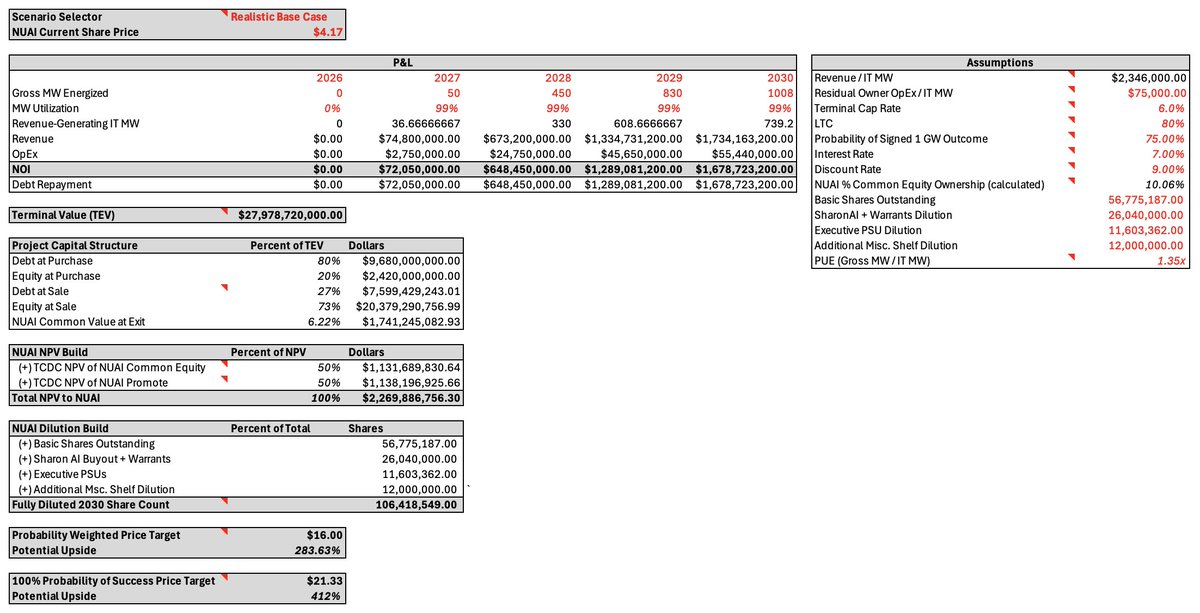

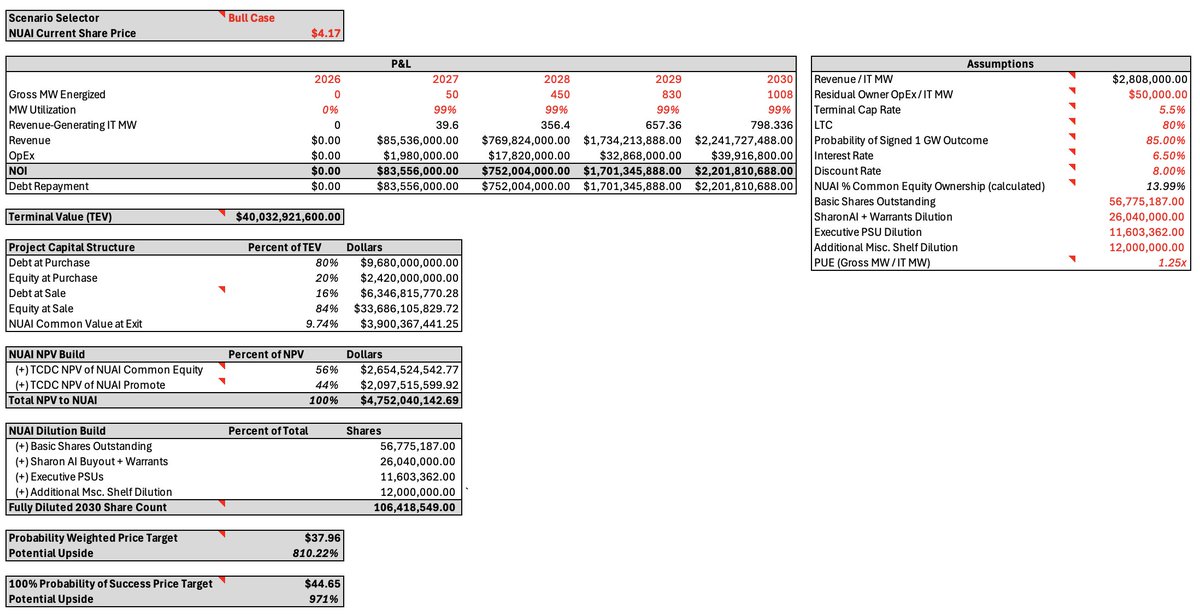

After six months of thorough due diligence on $NUAI—reviewing filings and engaging directly with management—I went all-in on this hidden gem. The company's behind-the-meter strategy is the way forward in today's power- and compute-constrained world. If you believe in management's plan to sign an investment-grade hyperscaler in the coming months, there is little doubt that this company is worth $3–5 billion. Yet it trades as a highly speculative small cap, currently valued at around $255M. Therein lies the opportunity. Most on X know me as a long-time bull on $IREN, a company I've been all-in on for the better part of 2.5 years. So this portfolio shift isn't one I take lightly. For the doubters, $IREN is, pound-for-pound, the best business in the AI HPC space today. In fact, if Mr. Market hadn't given me such a wonderful entry point into $NUAI, I would still be all-in on $IREN. The investment thesis: While both companies provide energy-intensive AI infrastructure, $NUAI's primary thesis is its valuation—materially below peers pursuing comparable opportunities. Few companies, if any, focus exclusively on behind-the-meter power delivery, sourcing directly at generation sites to achieve lower costs, higher efficiency, and independence from grid interconnection delays. This model makes the company highly attractive to prospective tenants amid rising demand for reliable, scalable power in AI compute. Like in most power markets today, the past 18 months in $ERCOT have seen substantial challenges for large-load grid interconnections. Datacenter-driven demand expanded ERCOT's queue from approximately 63 GW at end-2024 to over 230 GW by late 2025. The prior sequential study process resulted in repeated restudies, modeling inconsistencies, extended timelines, and uncertainty. Disguised as an attempt to help with those problems, ERCOT’s new batch process plans to group qualifying large loads for coordinated transmission studies to improve efficiency, consistency, and system reliability. For grid-dependent projects, this adds procedural layers and timing considerations during a period of high demand. Some would say this is a major step back for allocating capital to ERCOT. Meanwhile, $NUAI's behind-the-meter approach circumvents these grid-related hurdles—no queue participation, no restudies, no batch constraints. Power is provided directly to tenants through dedicated on-site power plants. $NUAI's first 3 GW will use gas-fired technologies, giving the company and its tenants unparalleled speed to market. $NUAI management expects to announce the first phase of TCDC (Texas Critical Data Centers) within the coming months. From there, the odds of ramping up quickly to 1 GW remain high. Management has stated repeatedly that they are in advanced discussions with multiple hyperscalers. It's worth noting that previously guided timelines have slipped, but the company has announced partnerships that shore up uncertainty around the desired outcome. Assuming management can get $NUAI to the promised land, we should see its market cap shoot up to $3–5 billion in very short order, finally bringing it in line with peers. That's a 12–20x in a matter of months. If management continues to execute on its NM site and others, NUAI could conceivably reach a valuation of $20bn—almost 100x from here—but we'll leave that for another day. The downside: What if the company isn't able to deliver on a hyperscaler tenant? Like any good investor, I am laser-focused on downside protection, and that's where $NUAI is a no-brainer. TCDC is a 438-acre site fit for a 1 GW AI datacenter. Located across the street from two large power plants owned by the likes of $VST and $FANG, and with three different natural gas pipelines serving the site, TCDC is the equivalent of what is called a “powered land” site. These days, powered land is valued at approximately $500,000 per MW, implying roughly $500 million in embedded land/power value for TCDC. With $NUAI's market cap hovering around $255 million, the land value alone exceeds the enterprise value, with the operations, partnerships, and development pipeline—including its 3,500-acre New Mexico site—providing additional upside. I describe the range of outcomes as “heads I win big, tails I still win.” The noise: The past few months have seen the company come under attack on several fronts. The most prominent is a civil complaint from the New Mexico Attorney General involving allegations related to oil-well responsibilities transferred through entities. The company has described the claims as unfounded, with no prior state engagement, and intends to defend vigorously. Maximum potential settlement exposure, based on disclosures and precedents, remains below $10 million. Having diligenced this with my own network of seasoned litigation attorneys, this is a nothingburger. Portfolio sizing: Concentrated sizing suits my investment approach: when extensive research identifies strong fundamentals, a clear competitive advantage, and attractive risk-adjusted upside, I allocate accordingly. I’ve taken over a decade to get here, so this is not a good idea for the vast majority of investors. To be clear, I don't go all-in often, but I do run a concentrated portfolio of 2–4 stocks. The past few years have been very different because the big winners have been sitting in plain sight. The first all-in idea in the past few years was $VST, a power production play, followed by $IREN, a power-meets-AI compute play. At their core, both are infrastructure companies within my circle of competence. $NUAI is just the next evolution of this very same AI infrastructure thesis. It's not every day you see 10-to-100 baggers sitting there in plain sight. And yet, here we are. $NUAI presents a highly asymmetric opportunity in energy-constrained AI infrastructure, with the valuation deeply disconnected from the company's intrinsic value. Do your own research—this involves risks inherent to early-stage development and sector dynamics. Not investment advice; simply outlining my allocation rationale.

Some of you know that I launched a hedge fund several months ago (early November). We run a long/short strategy, focused on owning the 20-40 growth stocks that we believe have the most upside over the next 2-3 years... this means they need to have great fundamentals, strong management teams, compelling valuations, and multiple catalysts that we can identify and track accordingly. It's been a rough few months for many growth investors (we also took some pain)... thankfully we were averaging down into our core positions but we've still seen some red months and it has not been enjoyable. I'm not a fan of losing money. Stepping back... I've never had more conviction in my process or my portfolio than I do right now... especially with some of my favorite stocks down 20-40% from their September/October/November highs despite strong Q4 earnings reports, strong CY2026 guidance and extremely compelling valuations. With that said, here are our top 10 positions in alphabetical order: $APP $CPNG $CRDO $HIMS $HROW $SKHYNIX $IREN $NBIS $RDDT $TMDX I believe all of these stocks are trading at meaningfully higher prices in 2-3 years which remains my focus for generating outsized long-term returns. Enjoy the rest of your day 😊 NFA. DYOR. ** @FirstWaveFund owns all of the stocks mentioned in this post.