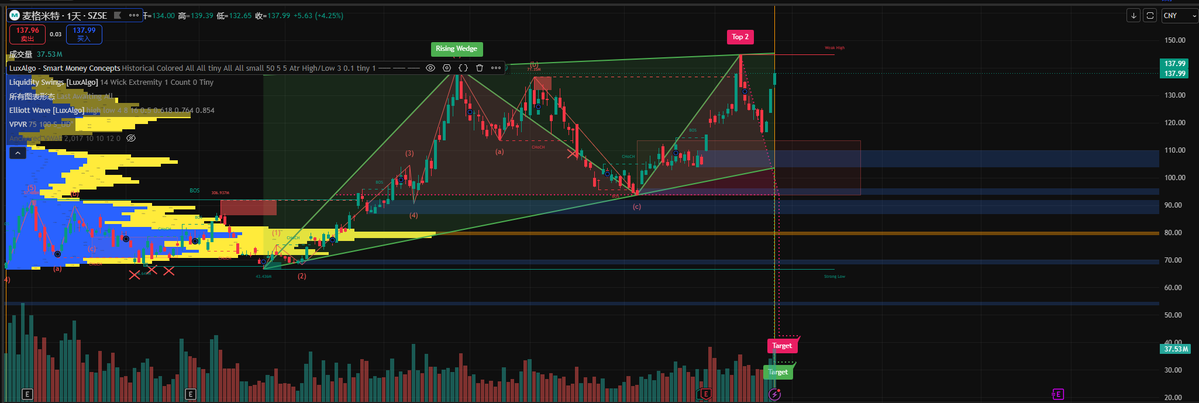

Jupiterdc

59 posts

How did my $NVTS position double already lol?

That aside, I did see a very compelling long out of the list of crowdsourced recs earlier for 800 vdc.

Doing more research now!

Serenity@aleabitoreddit

$NVDA actively pushing to 800V, and today was a pretty big signal. "On April 22, 2026, NVIDIA has initiated discussions with major South Korean power equipment companies to explore designing DC infra based on an approximately 800V direct current (DC) system" Previous named Nvidia partners include: Infineon, $TXN, $STM, $NVTS, Delta, Flex, $ETN, Schneider, and $VRT. It's been known they're been pushing for this but... looks like Nvidia is really driving it. Personally very small exposure to $NVTS since they're they have a high exposure for SiC/GaN ICs for 800V DCs. I know others really liked $VICR for exposure.

English

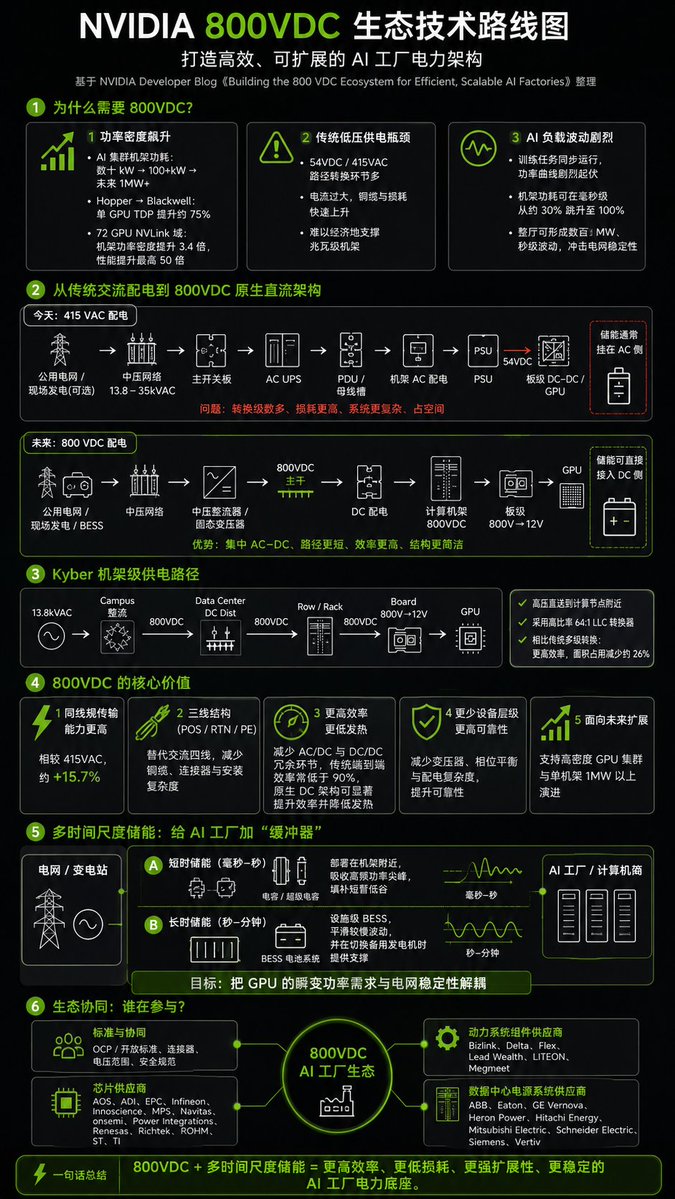

最近看到大家一直在说,800VDC,所以就从NV官网,developer.nvidia.cn/blog/building-… 让GPT总结一份整个产业链的框架。挺有启发的。目前明确的,相关的A股和港股里面有两家,英诺赛科和麦格米特,麦格米特今天涨停。看来后面应该就轮到英诺赛科了。

中文

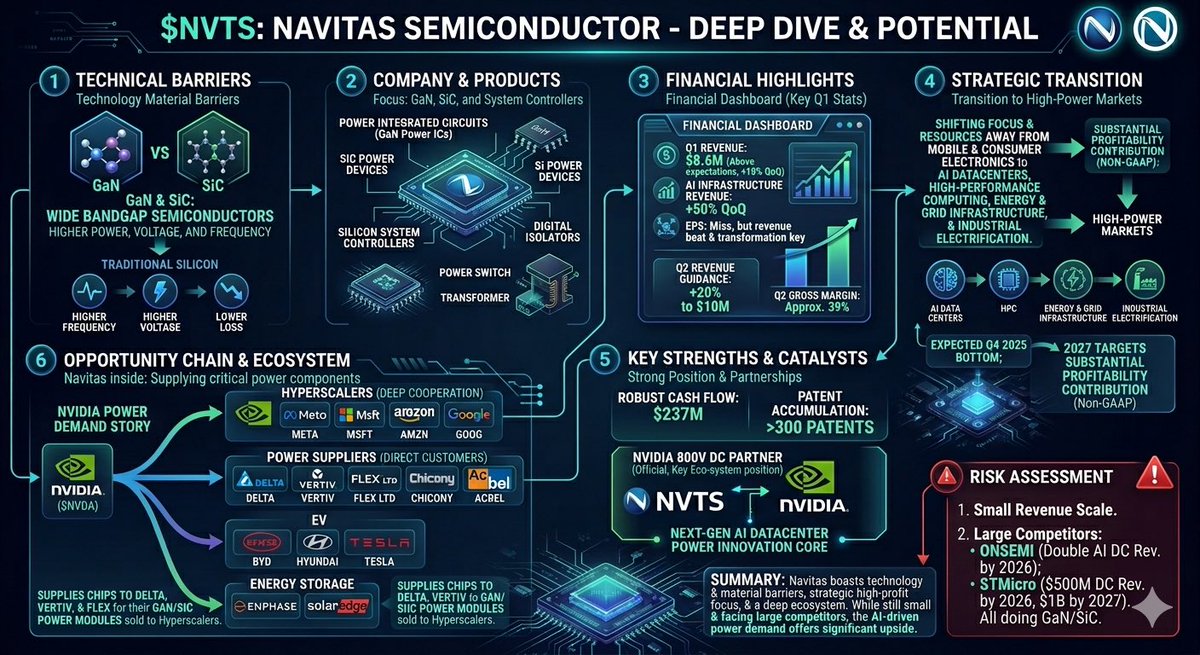

想和大家聊一下 $NVTS ,看看这家公司如何:

先说下最基本的看好点:技术材料壁垒,他在技术材料方面存在一些壁垒,因为GaN 和 SiC 属于宽禁带半导体,物理特性上就比传统硅强更高频、更高压、更低损耗。

先总体聊下这家公司:他们专注于设计、开发和销售功率半导体。然后产品包括氮化镓(GaN)功率集成电路、碳化硅(SiC)功率器件、硅系统控制器和数字隔离器,用于功率转换和充电应用,市场覆盖美国、欧洲、中国及亚洲其他地区。

对于他的产品有太多新名词的话,我们就把他们想象成电力变压和控制的核心零件,只不过层次做到了芯片的等级,很浅显易懂 对吧,类似于电网的开关和变压器,但更高层次,这个有什么用稍后会讲到。

好,然后了解他干什么最后,他的财报是非常亮眼,在Q1营收 $8.6M,超预期,环比增长 18%;AI 基础设施营收环比增长 50%;EPS 虽然miss,但市场更关注营收超预期和战略转型的进展,所以股价反而大涨,并且对于Q2的指引20%的营收增长到1千万,和毛利率稳步改善至39%。

我认为这样的财报来源核心是他们的战略转型,他们正在主动放弃移动和低端消费电子业务的短期营收,将资源、工程重心和渠道全面转向高功率市场——包括 AI 数据中心、高性能计算、能源与电网基础设施、工业电气化。这一些市场代表着更高的利润率和收益,所以管理层预期 Q4 2025 是营收底部,2027 年 AI 数据中心有望实现实质性盈利贡献(非GAAP)。 简而言之转换方向之后25年Q4就是底部。

现在公司由AI 数据中心功率需求叙事驱动,股价表现非常好。

我也很喜欢他们的现金流2.37亿美金 非常充沛,属于纯玩家定位,技术积累深厚(300+ 专利)。

他作为Nvidia 800V DC 生态的官方合作伙伴,其本身也是护城河的表现,因为他正处于下一代 AI 数据中心功率创新的核心位置。

那他还有什么可能性来支撑未来呢?

如果我们跟着 $NVDA 这条线走,再加上Navitas 声称与 hyperscalers、OEM 和 ODM 建立了深度合作关系这一点

1. $meta会成为其潜在客户,因为自建AI数据中心,他们需要大量采购 nvidia gpu,800v 架构跟进着。

2. $MSFT 作为open ai最大算力买家和数据中心的急速扩张

3. $AMZN 最大云厂商+ 自研芯片的同时也需要大量 $NVDA芯片

4. $GOOG 虽然tpu自研但也需要大量gpu,数据中心需求也庞大

所以他是跟着 $NVDA 一路吃到头的 可以看到,

另外我们还有电源供应商作为可能客户,vertiv ,flex ltd,chicony,acbel等

再往下走就是电动车板块:比亚迪,现代,tesla

最终则是储能: enphase,solaredge等

这一条线从上到下是超大规模云厂商,电源供应商,电动车,储能,消费电子。

另外需要说明的是,云厂商是最终买单方,但 Navitas 的直接客户其实是 Delta(台达)、Vertiv、Flex 这类电源供应商他们把 GaN/SiC 芯片做进电源模块,再卖给超大规模云厂商

所以他的潜力是有的,我也很看好他的可能性,风险也是存在着:

1. 营收规模依然很小

2. onsemi 预计 AI 数据中心营收 2026 年再度翻倍;STMicroelectronics 预计数据中心营收 2026 年超 $5亿、2027 年超 $10亿。 这两家体量远超 Navitas,且同样在做 GaN/SiC。

还是那句话,有技术 有壁垒,但也有很强的竞争对手……

$NVTS $NVDA $META $MSFT $AMZN $GOOG

#GaN #SiC #AIDataCenter #PowerSemiconductor #Semiconductors #StockAnalysis

中文

@cherryPayment @datacruiser NVIDIA is leading the transition to 800 VDC data center power infrastructure...To accelerate adoption, NVIDIA is collaborating with key industry partners including:

Silicon providers: ADI, Infineon, Innoscience, MPS, Navitas, OnSemi, Renesas, ROHM, STMicroelectronics, TI

English

▶ AI data centers spark 800V HVDC rush for Taiwan lead frame suppliers

- The shift toward 800V high-voltage direct current (HVDC) power architectures in AI data centers is gathering pace, driving a surge in demand for power semiconductors.

- As a result, shipments at Taiwanese lead frame makers SDI Corporation and Jih Lin Technology are climbing, with both companies expected to deliver double-digit revenue growth in 2026.

- Lead frame suppliers note that demand for AI server power-management systems has risen sharply in recent months, with orders from global IDM customers such as Infineon and STMicroelectronics also expanding.

- Whereas automotive demand had previously been the key growth driver, 2026 is shaping up to be the inflection point at which servers take over that role, marking a structural shift in lead frame demand.

- Lead frame makers explain that the automotive-grade product expertise they have built up over years is proving to be a critical foundation for entering the AI server power-management market, since automotive and AI servers share similar requirements in terms of high-power handling, thermal dissipation, and reliability.

- SDI notes that, in the near term, the pickup in orders for AI power management is running ahead of expectations. In particular, its high-power lead frame products for HVDC applications have moved beyond the R&D stage into volume production, with more than 40 custom projects currently underway.

- SDI's AI-related revenue accounted for only around 1% of the total in 2025, but is set to rise quickly to 6% in the first quarter of 2026. The company also expects the revenue contribution from HVDC-related projects to ramp up in earnest from the second half of 2026.

- Jih Lin notes that, supported by a recovery in the automotive market and expanding AI server demand, utilization has risen to the 70–75% range. It also expects 2026 revenue to grow quarter over quarter, making its full-year target of NT$6 billion achievable.

- Jih Lin's AI-related revenue stood at roughly 5–7% of the total in 2025, and the market expects that share to surpass 10% by 2027.

- The company is expanding into the AI power-management market on the strength of its integrated stamping-and-etching capabilities, and continues to develop 40–50 new products each year.

- It is also applying the double-sided cooling and thermal-dissipation technologies previously used in automotive modules to its AI server products, and says it is receiving a positive response at the customer evaluation stage.

- Overall, Taiwanese lead frame makers emphasize that order visibility is improving significantly, underpinned by expanding AI demand and long-standing partnerships with IDM and OSAT customers.

- Players with high automotive exposure expect the expansion of ADAS and the vehicle electrification trend to likewise drive a recovery in automotive semiconductor demand.

- The industry views the inventory correction phase as effectively complete, and sees a strong likelihood that shipment momentum will build further as 2026 progresses into the second half.

English

forget about $NVTS already up 350% recently ....

picks:

US - $POWI

HKEX - Innoscience

NVDA wants 1MW racks in 2027. GaN does the 800V→1V step down at the GPU. that’s the whole game.

$POWI 10% global GaN share, actually profitable (lol imagine), has their own 1700V platform sitting there. trades like some sleepy analog stock while NVDA is literally rewiring every AI rack to 800V by 2027. nobody’s modeling this.

$2577.HK (Innoscience) — these guys are the only GaN IDM in the world. #1 global share at ~30%, literally 2x Navitas. NVDA picked them as the only Chinese supplier on the 800V list. and here’s the kicker: TSMC is shutting their GaN foundry mid-26, which screws every fabless player. Innoscience owns their fabs. they just keep shipping while everyone else scrambles.

English

All right chat, crowdsourcing your #1 highest conviction (10x only) stock long for the Power Semi trade.

Especially given $NVDA pushing shift to 800 VDC.

Stuff like $NVTS or $WOLF, but high-beta, 10x potential only. Anywhere around the world.

What's your pick?

English

@henghaer123 实际上mlcc在二月炒过一次,但没发酵起来,那会murata在考虑涨价。这波mlcc起来实际上是从4月初有实质涨价预期+战后修复叠加的结果

中文

$NVTS Innoscience

qinbafrank@qinbafrank

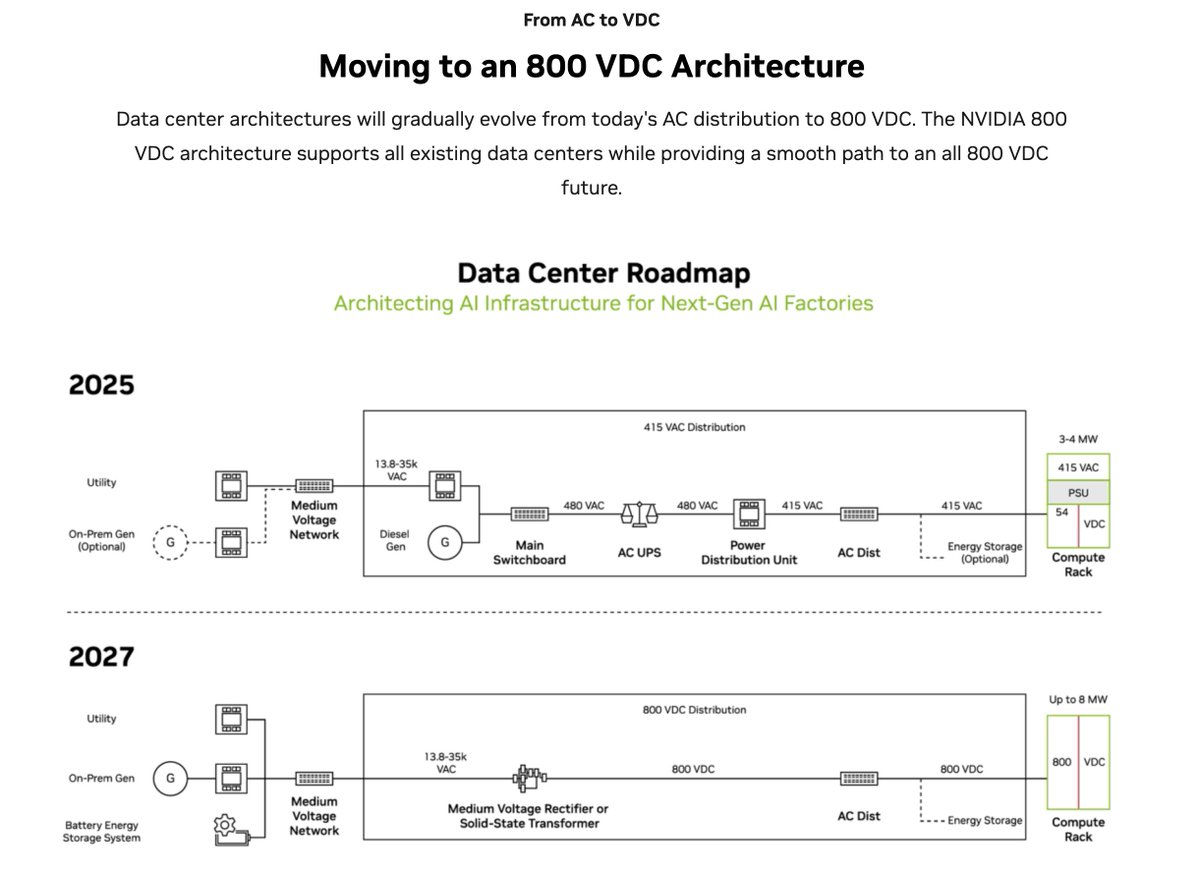

AI数据中心电力上的关键环节:800VHDC,今天在这里x.com/qinbafrank/sta…聊到大摩拆解VR200NVL72提到,大摩预计800V直流电将在2027年下半年推出的Rubin Ultra平台上得到大规模采用。其实800VHDC并不是全新概念,自从英伟达去年说要推直流供电架构后,市场对此的关注度其实挺高的,这个板块的相关的标的已经炒过一博预期了。但实际上800V直流电在下半年才真正大规模采用,值得关注。聊下几方面的问题: 1、800V HVDC架构是什么? 传统高密度AI rack的路径大致是:电网中压AC → 变压器/UPS/PDU → 415/480VAC到机架 → 机架内PSU转54VDC/12VDC → GPU核心电压。 达子的800VDC愿景则是:在数据中心边界/电力室把中压AC集中转换成800VDC,用800V DC busway送到IT rack,再在靠近GPU的位置用高比率DC/DC转换。NVIDIA称,54V架构在200kW以上开始撞上物理限制;1MW rack如果继续用54V,单rack铜排最高可能需要约200kg铜,而800V架构通过减少电流、减少转换级数、减少机架内PSU,目标是提升效率、降低铜耗、释放机架空间。 它不是简单的电压升级,也不是“发明了直流供电”,而是AI数据中心供电架构的一次平台级切换,是对整个电力交付架构的系统性重构,旨在解决传统48V/54V机架电源的瓶颈(空间受限、铜缆过载、多级转换损耗高),支持单机架功率从数百kW跃升至1MW+,并为未来GW级AI工厂铺路。 2、800V HVDC的意义和革命性是什么? 1)首先自然是效率和空间布局 效率提升:从电网到GPU的转换环节大幅减少,整体能效可提升从以前90%能大幅度提高到98.5%以上传输损耗显著降低,TCO(总拥有成本)降低可达30% 空间与密度优化:减少铜缆用量和电源单元体积,机架内计算空间利用率提升超80%,支持更高密度GPU集群 2)800V不是单一器件升级,而是生态重构:中央整流、800V DC busway、固态断路器、热插拔保护、sidecar/power rack、BBU/CBU、超容/电池储能、DC/DC、GaN/SiC、液冷都要协同。NVIDIA也明确说需要OCP等组织推动电压范围、连接器、安全标准。 如果大家有关注过新能源汽车产业链,应该有影响这两年国内电动车厂商都在推的“快充”基本上就是800V高压直流充电。现在达子正在把800VDC变成下一代AI rack标准化路线的一部分,所以一部分原来给新能源汽车充电产业链上的关键环节,又开始外溢到AI数据中心上了。 3、800V HVDC空间有多大? 要看大背景,AI数据中心整体市场从2025年约3440亿美元增长至2032年超2万亿美元(CAGR 27.5%)。 功率基础设施将成为AI建设的核心瓶颈与增长点,NVIDIA的标准将加速 hyperscaler采用,带动固态变压器、GaN/SiC功率器件等子市场爆发。 2027年后,>300kW/rack、尤其是400kW-1MW rack的AI zones中,800VDC或类似HVDC架构渗透率快速提升。若未来新增AI容量中有30%-60%采用高压DC架构,并且每MW对应的核心800V电力链价值量在几十万到数百万美元区间,累计空间就会进入百亿美元到千亿美元级。 当然这个预测区间也很宽,因为真实取决于Kyber/Rubin Ultra出货节奏、超大云厂接受NVIDIA 800V的程度。 4、800V HVDC产业链构成 完全是英伟达参考设计主导资格认证,之前英伟达也公开列出的核心合作伙伴分为三类,竞争激烈,份额将取决于认证进度、量产能力和 hyperscaler合同。 1)硅片/功率半导体供应商(核心器件,如SiC/GaN MOSFET、控制器,用于高效转换): 主要玩家:Texas Instruments(TI,已发布完整800V解决方案)、STMicroelectronics(ST,6-18kW功率板)、Infineon、ROHM(SiC器件)、Navitas(GaN/SiC)、Analog Devices、onsemi、Renesas、Innoscience、MPS、AOS、EPC等。 这些是NVIDIA“硅供应商”名单核心,TI/ST等已演示参考设 2)电源系统组件/模块供应商(电源架、Sidecar、DC-DC转换器等): 主要玩家:Delta Electronics(与NVIDIA深度合作,发布800V解决方案)、Flex、LITEON、Megmeet、Lead Wealth、Bizlink等。 Delta等中国厂商优势明显,已有白皮书和技术落地;LITEON等股价因800V预期已经显著上涨。 3)数据中心电源系统/基础设施供应商(机架级配电、Sidecar、SST、母线等): 主要玩家:Vertiv(Hopewind为其800V系统关键子供应商)、Schneider Electric(开发1.2MW Sidecar)、Eaton、ABB、GE Vernova、Siemens、Hitachi Energy、Mitsubishi Electric等。 这里面Vertiv、Schneider、Eaton等是传统强者。 个人角度看 1)Vertiv、IFFNY、Schneider、Eaton、Delta、ABB是最可能在早期800VDC相关收入中占到显著份额的几家公司; 2)LITEON、TI、ST、Infineon、onsemi是第二组确定性较强的受益者; 3)Navitas、Power Integrations、MPS、BizLink、Megmeet、Innoscience(英诺赛科)属于弹性更大但验证/量产/竞争风险也更高的一组。 个人角度当下比较看好的则是,当然这个还要动态迭代: nvts、IFNNY、英诺赛科、vicr 5、后续跟踪落地节奏的几个重要节点 1)NVIDIA Kyber / Rubin Ultra 2027节奏:是否明确把800VDC作为默认/主推rack电力架构,而且出货节奏也带动800V的落地节奏 2)OCP标准进展:800V连接器、安全、保护、PDB、BBU/CBU是否标准化。 3)看点电源管理系统组件,功率半导体供应商的点单披露,谁真正进入了进入backlog和量产socket;这个最关键决定了哪家供应商能吃到多大的份额 4)超大云厂路线:800V vs 400V/±400V vs 50V HPR是否分裂。决定了市场对800V hvdc的预期和想象空间。 5)单MW成本下降曲线:如果800VDC使每MW可部署GPU数量、能效和维护成本明显改善,它会从NVIDIA专用架构变成行业事实标准。

English

$NVTS $02577 innoscience

TrendForce@trendforce

The #AI race is now an energy race. In our latest deep dive, we explain why wide-bandgap power semiconductors like #SiC and #GaN play an essential role in enabling the future 800V AI data center architecture. More: pse.is/94f2lj 🔗 #Semiconductors #DataCenter #HVDC

English