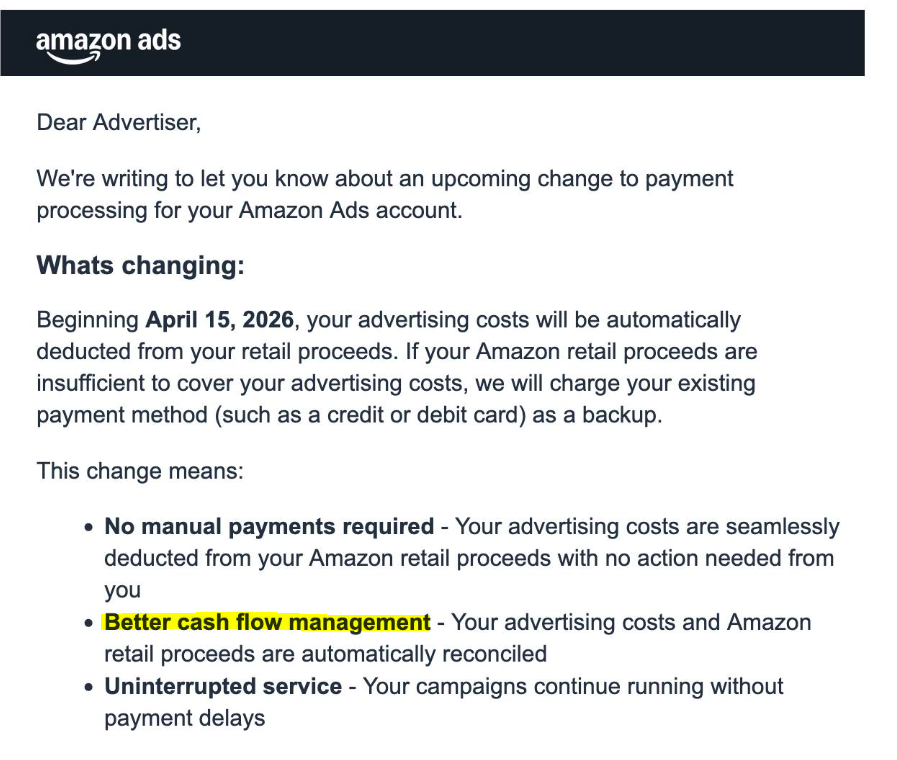

고정된 트윗

Dear @realDonaldTrump Please renegotiate the U.S.-China Tax Treaty which was signed before the advent of e-commerce.

This has unfairly allowed unfettered access to U.S. consumers for Chinese companies (without a $ in tax collected).

Save the American dream for Americans!

Shinghi@ShinghiD

2/ First, the U.S.-China Tax Treaty (signed in 1984, effective 1987) aims to prevent double taxation and encourage cross-border trade. It covers income like business profits, dividends, and royalties—but only taxes foreign entities if they have a “permanent establishment” (PE) in the U.S.

English