@burningpremium@kurtsaltrichter been trading vol products since the XIV days and this is exactly right but also the thing nobody wants to hear

backwardation flips the whole game mechanically but everyone's watching spot VIX levels like they matter more than the curve

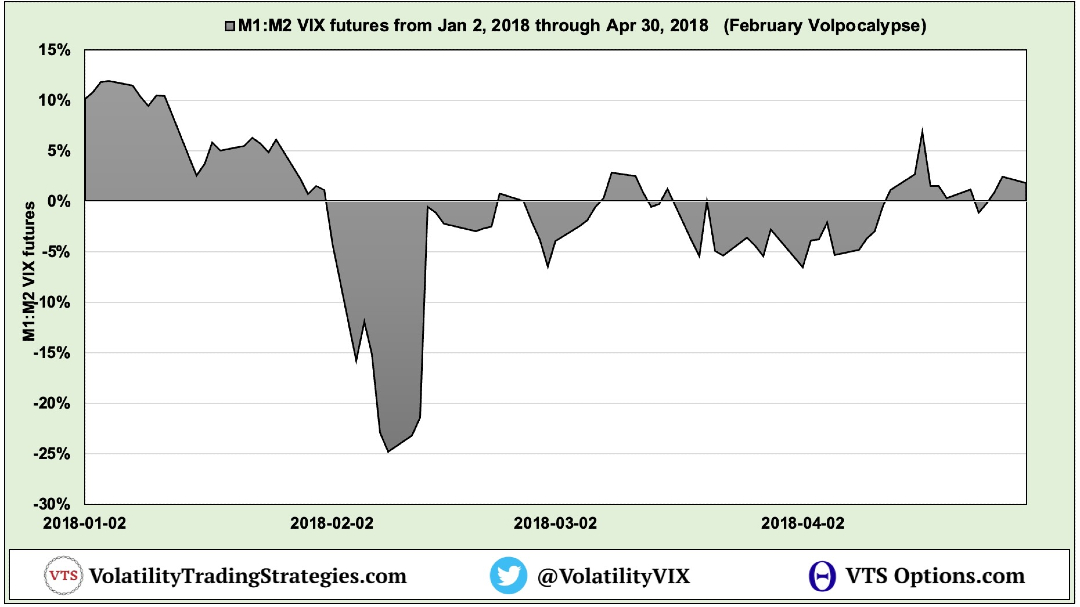

April-May $VIX calendar spread closed at -0.49. Still in backwardation. Primary trend remains lower.

-$1.44 is the key level to watch. Break below it, and another short-vol squeeze is in play, which means more pressure on stocks.

Backwardation doesn't lie. Near-term fear is still priced above long-term fear.

That's not a risk-on signal.

@QuantifiedStrat what's the mechanism? vix lags the panic, so it stays above its 100ma through the recovery leg of every drawdown. the indicator's lag is doing the work instead of the level.

@onlybreakouts what's the mechanism though? in the low vol regime, who's being forced to do what when the breakout happens that isn't happening in the high vol one? if there's no answer, the filter is likely selecting for the moments when vol clustering breaks, which is what you're measuring.

Low volatility produces better breakouts than high volatility.

That surprised me too.

I tested a volatility timing filter across 2,500+ strategies and the data was clear: breakouts during quiet, compressed markets outperform breakouts during volatile ones.

On the Nikkei 225, I split ATR into two bins - high volatility and low volatility - and only traded in the low bin. Average trade jumped from $160 to $306. Drawdown dropped from $7,000 to $1,500. Profit-to-drawdown ratio went from 5 to 20.

Most traders wait for big volatile moves before entering.

The data says that is exactly backwards.

Low volatility means the market is coiling. When a breakout happens during compression, stored energy releases in one direction. High-volatility breakouts compete with noise and whipsaws. The move looks exciting but it chops you up.

In-sample results matched out-of-sample at 100% consistency. The low-volatility edge held on data the model had never seen.

The filter barely has anything to optimize. Two ATR bins. One rule. And it produced the largest single improvement of any technique I tested.

$160 to $306 per trade. Trade the coil, not the chaos.

@burningpremium@SystematicPeter Maybe he for got to say it’s 5 sharpe for the current time he’s been running it? Can’t be may trades - no way does it stay 5 sharpe and you just give it away on the internet surely 😂?

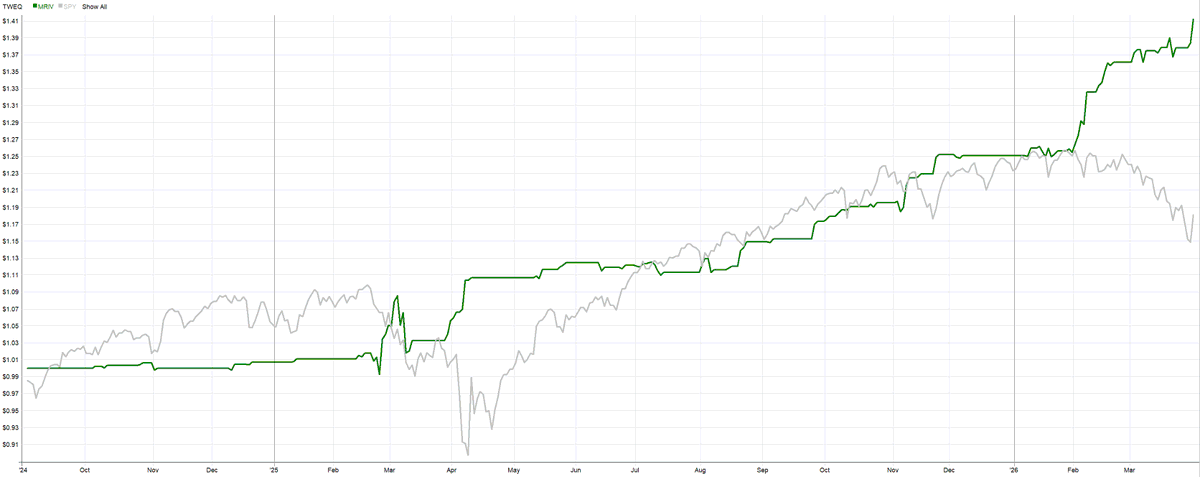

Current market has been very favorable for long mean reversion strategies.

The one standing out most in my account is an implied volatility-timed model I have mentioned many times.

So far this year:

- YTD return 12.6%

- Drawdown -1.6%

- Sharpe 5.05

- Win rate 86%

And here is the part many traders miss:

it achieved that with just 10.78% average capital usage.

That matters because the remaining capital can keep working in other strategies.

The idea is simple:

Every day I download implied volatility from IBKR.

Implied volatility reflects what option sellers expect about future movement, so it carries current market information in a way pure price-based mean reversion does not.

If the market drops more than implied volatility suggests, I buy the next day with a limit order.

Then I exit into the expected rebound defined by IV.

That is the key difference vs classic price-only mean reversion:

this approach adapts to current conditions instead of treating every drop the same.

I published a deep dive in September 2024 (including IBKR IV downloader):

crackingmarkets.com/iv-mean-revers…

Which means the equity shown since publication is pure out-of-sample.