goldenlabubuwatch@pandawatch88

Extremely clear from the QFIN FINV XYF calls that management has no idea what's coming in 2026.

Beyond volumes and provisioning for Q4 Q1, the big question to me is what's the new normal (you hate that word too yes? good, I want to make this reading extra painful) for loan book size, take rates, and profit 2Q26 onwards (once the 1H25 vintages lap).

Because remember, the spirit of the regulation is twofold:

1-"stop pushing loans with hidden pricing to people that can't afford them" and

2-"for those that can afford it, lower the cost, we want them to consume"

Other things being equal, the above points to lower TAM (so smaller loan books) and lower profit (so lower ROA).

Offsets? You can sell yourself many stories:

-Gain market share from people exiting

-Expand TAM as you lower price (getting into ANT territory, so good luck)

-Get into ecommerce loans like LX

-Benefit from lower CAC due to less competition

-International (SEA for FINV and UK for QFIN)

etc

So, who knows. Let's look at a couple of scenarios, and how much money we make from here, to see if it's worth the punt:

The upside case (25% chance):

-everything goes back to normal in 2H26, loan book size and ROA recover, QFIN is back to usd1bn profit and FINV to usd450m, and from there grow loan book at 10%, few points above consumption. No need to make numbers here because you will make a lot of money.

The downside case (10% chance):

-this regulation is step 1 into managing the banning of the industry a year for now, making consumer loans purely a bank business. This would be painful for the banks too, who right now sit back and rely on these guys as origination partners (try to teach a Yunnan rural bank how to sell loans on Douyin). No need to do numbers either.

And the rest, somewhere in the middle.

I have looked at a conservative case with a "new normal" as follows:

-PF loan book 20% smaller for QFIN and 15% smaller for FINV

---4Q YoY volume guide is down 15-20% QoQ for both QFIN and FINV, which is 25% down YoY

---part of that is risk control part of that is the loss of TAM

---what does it mean for loan book size in a couple of quarters once risk is stable and it is just a TAM issue, no idea. So I say it is 80% of what it was before for QFIN and 85% for FINV.

-3% new ROA for both going fwd

---(defined as EBIT over avg loan book, because thats my historical series calculation)

---QFIN went from 6% at the 2021 peak to 2.5% at the 2023 bottom, combination of adjusting loan pricing and delinquencies at first, to expanding loan book into lower take rates areas later on. From there it rose to 6.2% as of 1Q25 benefiting from lower funding costs release of provisions and probably loan mix too.

---FINV went from 8% in the good old days to 3.5% in 2023 to mid 4% latest. Many drivers here and also keep in mind they are investing in SEA

---LX is at 2% and XYF at 4%, historical range from zero to 4% for LX and 6% for XYF

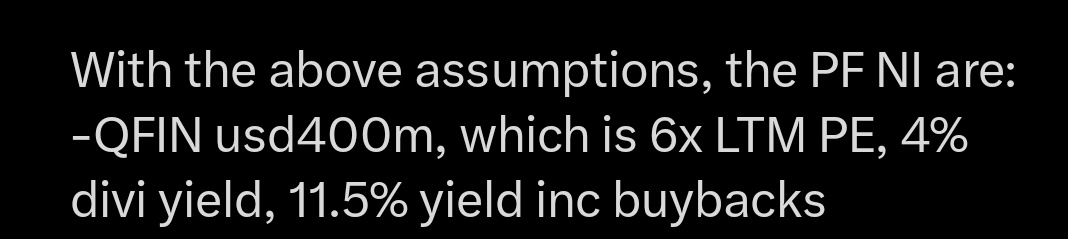

With the above assumptions, the PF NI are:

-QFIN usd400m, which is 6x LTM PE, 4% divi yield, 11.5% yield inc buybacks

-FINV is usd230m, which is also around 6x LTM PE, 4.5% divi yield, 12% yield inc buybacks

(they dont look that cheap now eh)

And from there, we grow the loan book at a 5 year CAGR of 8%, assume ROA trends up from 3% to 3.5% as it scales, and multiple stays at 6x, this means:

-11% IRR for QFIN, inc shareholder returns 23% or 3x money

-similar for FINV (bit more)

So that's how it looks to me at the moment.

Management will say the conservative case is bulsit, not a chance loan book goes from usd20bn to 16bn, and ROA from 6% to 3%, sure, I'm open, then tell me where it is going to go. The reality is they don't know, it is not up to them.

I'm going to spend some time digesting it this week, probably i missed stuff, or some numbers are off, feel free to raise it. But at the 5Y 3x payouts above vs what's available out there, and with doughnut a distant but possible scenario, I think my size will come down by half, would be a pity on the roundtrip, we made the money on divis tho.