A.C.

3.7K posts

A.C.

@AC16_1992

Ball security is job security

Boston, MA Katılım Eylül 2016

510 Takip Edilen168 Takipçiler

Jets add two round 1 pass-catchers to go along with G-Wil. Not really a fun spot for either Sadiq or Cooper, who have to compete with each other and Wilson in an offense that isn’t gonna project all that well.

Another disappointing landing spot.

Jordan Schultz@Schultz_Report

No. 30 pick is in: #Jets have selected Indiana WR Omar Cooper Jr, per sources.

English

@ContrarianCurse Casually dropping you're in the 80s without really caring or trying 😂

English

I am a solid 4-5 rounds of golf/year kind of guy. I really don't love it. I'll shoot 87-95 depending on the day with always a chance of a blow up. I find it frustrating generally

Never ceases to amaze me how obsessed someone can be for years while shooting like 130

English

@ScamNetwon @realDave1984 @LeadingReport I'm not sure these cult members are interested in facts. Simply not going to work

English

@realDave1984 @LeadingReport do you think we can’t see people betting billions on the Iran war and the oil markets or something?

English

BBC alleges that the Trump admin may be engaging in insider trading.

English

A.C. retweetledi

The insider trading suspicions looming over Trump's presidency bbc.in/3OzfTQb

English

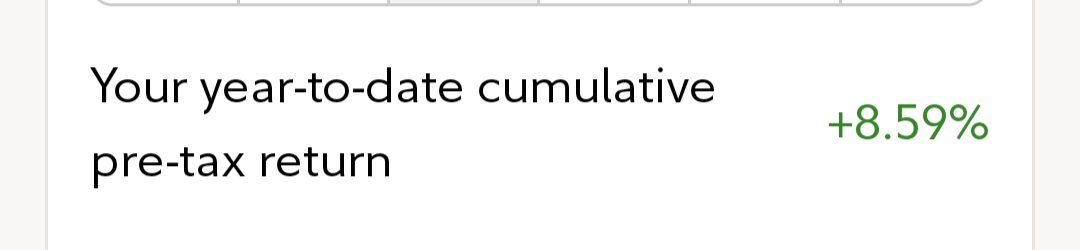

@hannibalspeaks You are right .. YTD 8.5%

Two winners so far RVMD and TERN

Last year CDTX, MRUS, and partials RVMD ABVX NKTR RNA BBIO PTGX

English

@zerohedge Bro what

“Apollo Debt Solutions (ADS), said on Monday it was curbing redemptions at 5% of its shares after investors sought to withdraw approximately 11.2% of the total.”

reuters.com/markets/europe…

English

@TheBroskiUSA @JoeSquawk Joe is the simplest of retarded mouthpieces for this admin. For reasons we'll never know, he's still employed on this network. Should just go spew his propaganda on Fox 🤷🏽

English

@JoeSquawk Joe lying again. Covid inflation was exogenous, and biden successfully brought it down to 2.9%. Remember that biden printed less $ than trump 1st term.

trmp tariffs and war are pure policy choice, additional taxes on Americans.

English

Inflation averaged 5.2% under Biden. Even with a war and tariffs to rebalance global trade March core annual CPI rose 2.6%

Pete Buttigieg@PeteButtigieg

Inflation has tripled from just one month ago, and it’s higher than when he took office. Not only has Trump failed to deliver on his central campaign promise to make life more affordable - he is actively, directly driving prices up.

English

@AdvisorMikeL He often talks about these products in 401k plans but fails to actually contextualize how much is in these plans (very little)

English

I disagree with Nick on the risk posed by Athene’s fixed-index annuity hedge portfolio.

I started to reply in X but I had too much to say about how index annuities work, how insurers hedge, counterparty risk, and where I think the real trouble lies.

open.substack.com/pub/investment…

Nick Nemeth (Mispriced Assets)@NickNemo17

Athene sells Fixed Indexed Annuities. The pitch to retirees: "You get some of the S&P 500's upside with none of the downside." To deliver that promise, Athene buys call options on the S&P 500 from investment banks. Market goes up, the option pays, Athene pays the retiree. The retiree thinks she owns a savings product. She owns the other side of a derivatives trade. The numbers: $8.1 billion in fair value derivative assets against $4.1 billion in capital. The derivative book alone is 2x the capital base. 78% is S&P 500 call options. 1-2 year maturities. The annuity liabilities they hedge last decades. Every year the hedges must roll — at whatever the market is charging. In a vol spike, option costs can triple. The cost of keeping the promise can exceed the profit earned on the entire investment portfolio. Two French banks — Societe Generale ($2.04B) and BNP Paribas ($1.69B) — hold $3.7B in fair value derivative exposure. Nearly the entire $4.1B capital surplus is concentrated in two counterparties. Citibank's potential exposure alone is $590 million — 15% of total capital from one name. $655 million in cash collateral posted. Hundreds of millions more in corporate bonds pledged as initial margin. In a liquidity crunch, that collateral is trapped. The NAIC's own "Potential Exposure" metric — what Athene could lose if counterparties default — is $2.1 billion. Half the capital. Estimated total notional: $120-160 billion against $4.1 billion in capital. 30-40x the capital in derivative exposure alone, stacked on top of 69:1 leverage on the invested asset portfolio. This extends beyond Athene. The dealers who sold these calls — SocGen, BNP, Barclays, BofA — delta-hedge by holding S&P 500 stocks and futures. If the economics of rolling break in a vol spike, the dealers unwind those hedges. That is a sell program the equity market does not see coming because it is embedded in the options market. Athene is one insurer. The entire FIA industry runs the same playbook through the same 8-10 dealers. The collateral is pro-cyclical — market stress reduces collateral values, triggers margin calls, forces liquidation, reinforces the decline. The derivative book is not a hedge that makes the company safer. It is a transmission mechanism connecting the S&P 500 options market, the European banking system, and American retirement savings into a single point of failure. Max pain is a simultaneous equity sell-off and vol spike — Q4 2008 conditions. Equities drop, so the call options Athene holds lose value. Vol spikes, so the cost of rolling triples. Credit widens at the same time, impairing the bond and mortgage portfolio. Collateral values fall, triggering margin calls from the same French banks. Margin calls force liquidation of illiquid private credit at distressed prices. Realized losses erode capital. Rating agencies downgrade leading to more capital calls. Headlines hit. Policyholders surrender. Surrenders require cash. More liquidation. More losses. Dealers unwind delta hedges. More equity selling. More vol. The loop feeds itself. The closest analog is AIG. AIG sold credit protection to banks. Athene buys equity protection from banks. The direction is reversed but the mechanic is the same — a massive concentrated derivative position with a handful of counterparties, on a balance sheet with insufficient capital to absorb a tail event, wrapped in an insurance company that the public trusts because the word "insurance" is in the name. AIG needed $182 billion from the Fed. Athene's balance sheet is comparable in size. This structure has never been stress-tested by a real crisis. It did not exist in 2008. This reads to me as lot like Leland O'Brien Rubinstein. Page 9,599 has the verification table. Pages 6,401 through 9,598 have every individual position. The filing is public. I am inviting every derivative structurer, risk manager, and counterparty credit analyst to open Schedule DB and tell me what I am missing. @jam_croissant The filing: athene.com investor relations, AAIA Q4 2025 Annual Statement.

English

Blue Owl told investors that fresh capital exceeded redemptions in its tech BDC. Sounds reassuring until you read the shareholder letter. They count automatic dividend reinvestment as "inflows." Your own dividends - recycled back into the fund you asked to leave - are their definition of new money. 41% of investors asked out. 5% were allowed to. The rest had their distributions reinvested into the position they requested to exit. That's not fresh capital. That's captive capital with a marketing label.

English

@FAKDADDY75 @from1to3000000 Sounds like a bunch of excuses and crying here. Cults = mental illness.. seek help!

English

@from1to3000000 So basically .......

What do you expect - he cant fix anything due to Uniparty.

well ...... then we are hosed regardless

Not much of a #winning deal here

English

@goodalexander $APO and $ARES, a few listed BDCs w/ low software exposure 🤷🏽

English

so private credit is:

A. part software that is automatable via Claude Code

B. part low end consumer that will be destroyed by high oil prices and high rates

C. a bundle of mystery meat facing massive redemptions that cannot be met

D. $3.5 trillion of notional

seems non ideal

English

Distressed debt is disappearing:

• Private credit is keeping zombies alive

• LMEs have taken over public side

• Market is more familiar w/ restructuring

Opportunistic credit and LMEs have taken its place.

English

This man’s got the biggest ears I’ve ever seen but doesn’t even hear himself

AF Post@AFpost

State Sec. Rubio: “Imagine if instead of spending billions on weapons, Iran spent that money on its people. They’d have a much different country.” Follow: @AFpost

English

@adamfeuerstein Surprised a few accounts didn't highlight the big volume candles to prove this out!

English

Why didn't the folks who track $LLY private jets predict the $CNTA deal?

English

@cedricdav @saxena_puru His preferred candidate. The fact he says harris was worse is pure cope. This is your guy, Puru! Enjoy!

English

@saxena_puru I couldn’t agree more. Can you then explain why you were such a big Trump supporter heading into the 24 election?

English

@SpecialSitsNews They should all cap at the 5% that they advertise. This way investors fully understand the meaning of semi-liquid. This is good for these products in the long run

English

All these firms will have no choice but to gate

$APO Apollo Global Management Inc. is curbing redemptions from one of its largest non-traded private credit funds for retail investors, becoming the latest alternative asset manager to grapple with a surge in such requests.

The $25 billion business development company, Apollo Debt Solutions, capped withdrawals at 5% of outstanding shares Monday after clients sought to redeem 11.2%."

English

A.C. retweetledi

Trump's installed leads at the SEC are actively blocking the enforcement division from investigating insider trading tied to the Trump family.

tradfi news@tradfi

*SEC ENFORCEMENT DIRECTOR MARGARET RYAN CLASHED WITH AGENCY BOSSES BEFORE RESIGNING LAST WEEK *RYAN WANTED TO BE MORE AGGRESSIVE IN PURSUING MISCONDUCT, INCLUDING CASES WITH TIES TO TRUMP & HIS FAMILY

English

@tracyalloway These funds advertise liquidity of up to 5%. Do you think investors can capture an illiquidity premium while also demanding more liquidity than a fund advertises?

English

Your daily reminder that the private credit crisis is still unfolding, Apollo is limiting redemptions from one of its biggest BDCs:

English

@saxena_puru @SECGov This was your preferred candidate. He will do nothing about it, and you know it. Enjoy!

English