Ankit Kamboj

137 posts

Ankit Kamboj

@AnkitKambojTO

Private Equity investor at KCM Holdings focused on SMBs and LMM PE. Here to learn and meet other investors, operators and deal makers.

Toronto, Ontario Katılım Kasım 2023

158 Takip Edilen90 Takipçiler

A few months ago, we had $0 of sales from Meta Ads.

After hiring someone in Brazil to start and manage it, we did $100k this month and quickly growing

English

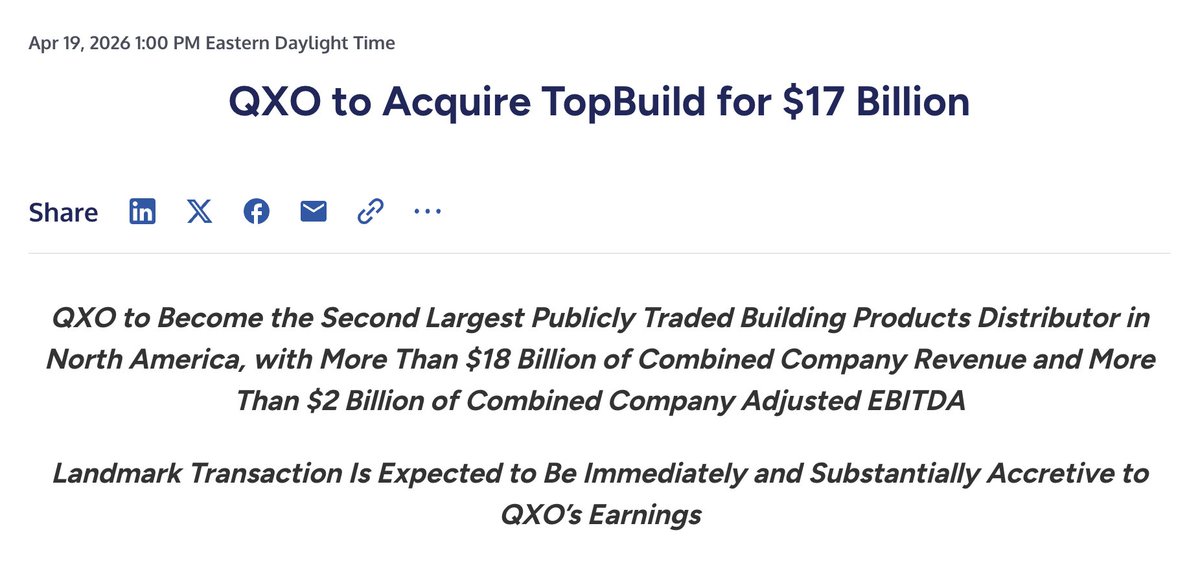

QXO buying TopBuild for $17B (55% stock) at 14.9x EBITDA (pre-synergies)

Public consolidators paying premium multiples while PE-owned peers trade distressed

Winners consolidate. Losers restructure.

English

@_PE_Charles I’d be interested to get access and provide any feedback.

English

Playing around with something that's been in my head for a while on value creation...

Every client I talk to wants real, industry specific examples for how value is generated, typically tailored to their specific problem.

I'm (very slowly) building a reference library for value creation case studies. Focused on public and private companies.

Eventually, would be great to get real stories from real people, relevant to LMM PE.

Thoughts and feedback welcome. Useful or dumb?

English

@Will_Schryver Do some research into the business, it’s more diversified than just a lumberyard.

English

What part of the cycle are we in when lumberyards trade for 10.7x

$QXO is acquiring Kodiak Building Partners for $2.25B

Kodiak generated ~$2.4B revenue / ~$211M EBITDA

Few years ago I was on the sell side for a lumberyard and we were lucky to get 6x

PE-backed consolidating platforms targeted 8x upon exit so Kodiak trading for 10x+ is extraordinary

English

@PEoperator One of the best capital allocators out there, amazing how small they started and what they’ve become.

English

This book is absolutely mind blowing.

One of the greatest operators you've never heard of (I hadn't either).

Must read and added to the list at: peoperator.co

Alain Bouchard built Couche-Tard / Circle K into a compounding machine… in about the least glamorous industry on earth: convenience stores.

From its IPO, he beat Warren Buffett.

The numbers are staggering:

$100 invested at Couche-Tard’s 1986 IPO became $60,000 by spring 2016

That’s ~600x.

For context, over that period, the S&P500 did ~22x and Buffett did ~99x.

Alain was not a passive investor. He was a hands on operator, involved in every facet of the business and obsessed with customers and execution.

He founded Couche-Tard in Quebec after having been an employee in the industry for several years.

He and his team (he convinced three partners to join him) acquired 11 stores and two buildings for just $20k down up front.

He was relentless - driven by a chip on his shoulder having watched his dad go bankrupt in his own venture.

While was an operator through and through, he had some serious financial savvy too.

How did he do it? Here are my key takeaways from the book:

1) Humility

“At Couche-Tard… we are egoless.”

Even with immense wealth (talking about mgmt)

“After all these years… you still feel that they are ordinary people… They listen.”

2) No bureaucracy

Bouchard despised headquarters arrogance:

“He wanted Couche-Tard to avoid that culture completely… it all started with having no head office… the base of operations would be a ‘service centre.’”

And he was relentless about language:

“There is no head office in this company, and there never will be… We are a service centre and a training centre - that’s it.”

3) Radical decentralization

“The decision… still applies today… We took a decentralized approach.”

Fortin (CT's CFO) called it the key:

“To delegate power to the regions… It’s the model that would end up allowing us to buy convenience stores around the world.’”

4) Customer obsession

“The clearest insights can sometimes come from the bottom rather than the top.”

Bouchard didn’t tour stores for optics - he wanted to see the tip of the spear:

“I don’t do these tours to inspect buildings.

I do them to talk to people… to learn about their reality.”

And when he visits stores:

“He isn’t talking to us. He’s talking to the store managers, the store employees… He connects and gives them attention.”

5) Operational excellence

Couche-Tard viewed itself as a compounding network:

“They were part of a network in which the most profitable contribute to those still developing.”

Story after story about how they pursued excellence in their stores and their ability there gave them conviction to lean in on larger and larger acquisitions...

6) Aggressive M&A + artful dealmaking

They engineered operator-driven acquisitions early:

“They acquired 11 depanneurs (convenience stores) and two buildings - with only $20,000 down… ‘we came back with cash.’”

They bought a competitor twice their size:

“The deal wouldn’t cost a cent… Metro-Richelieu would effectively hand over all its depanneurs for shares.”

And they showed up as operators, not financiers:

“The founders… with our noses in the books, while the other groups had sent lawyers and accountants.”

7) Tolerance for failure

Bouchard encouraged entrepreneurial action everywhere: “He encourages risk-taking… prefers trust… even when it sometimes backfires.”

Every store was a lab:

“Each store should be considered a laboratory where the best ideas can germinate… harvest them and disseminate them.”

“The indispensable corollary is tolerance for error.”

--

Couche-Tard is proof that the greatest compounding machines are often built far from Wall Street…

One store, one manager, one deal at a time.

Again, check it out here: peoperator.co

And thanks to @sidecarcap for the recommendation!

English

You can buy $V at its cheapest multiple of the year (close enough) 👀

How do we feel about a fwd P/E of 25x?

English

If you’ve got $2.8 million sitting around, a 9.25% savings rate pays you ~$259k a year.

No stress. No risk. Just passive income.

Why aren’t more people doing this?

English

Buddy of mine got an offer from private equity for his home services company

“High single digits” EBITDA multiple

90% cash at close / 10% earnout

Would you take this offer?

English

@ACapitalLP It’s definitely interesting at these levels, especially based on the guide of $330M to $360M FY EBITDA

English

Ankit Kamboj retweetledi

Ankit Kamboj retweetledi

Warren Buffett Checklist

The Only 3 Ways to Improve a Business:

The Icahnist@TheIcahnist

Young Buffett was Ruthless Buffett played private equity in public markets Here’s his early strategy⬇️

English

Bill Ackman strikes $2.1bn deal for insurer in bid to build ‘modern Berkshire Hathaway’ ft.trib.al/hab9sRA

English

My local golf course (member's only) just ditched their course management software in favor of an in-house solution. Apparently it was entirely vibe coded by a 17 year-old caddie in exchange for 5 green fees, a 30 rack of beer and a Zyn pack. $CSU is in deep trouble guys

English

Ankit Kamboj retweetledi

Stanford lecturer show how to trigger growth in your life...

English

Another McGuireWoods independent sponsor conference in the bag !

One observation I’ve had over the past few years (and strongly reinforced the past few days) is there are many supposed “truisms” espoused in the independent sponsor market that are just not quite right in the real world…

If you’ve been an investor for more than 5 mins, you realize that EVERYTHING is actually a shade of gray and that there are very few absolutes in the world…

To provide but one example, there are some capital providers that are obsessed with trying to find sponsors who specialize in one sector…

Is this inherently bad? - absolutely not. Is the natural corollary that more generalist investors present less compelling opportunities accurate? Not at all. There are many extremely successful generalist sponsors who have completed many deals and who continue to be active in today’s market. How can those who espouse the supposed superiority of specialization explain away the prodigious performance of these “lesser” generalists…? I’m generally curious because the individuals I’m referring to have completed many deals - they did not simply get “lucky”…

What’s worse is that calls for industry specialization often come from those capital providers who are themselves generalists…! It’s upside down…

What can we learn from this? Well just because something is conventional wisdom doesn’t make it correct or accurate…In fact, the money is made in the nuance, not in conventional wisdom

Stay curious. Question everything. Most importantly, think for yourself and do not accept on face value what you are told…

See everyone next year !

Dino@DinoSawaya

If you’re at the McGuireWoods Independent Sponsor Conference, come say hi ! It’s easy to find me. Probably the only one with an Aussie accent !

English

Recommend reading…

Akin to The Outsiders or Intelligent Fanatics.

Great chapter on Constellation Software. My favorite was Lifco.

Overall theme, summarized:

These acquisition-driven compounders operate with a simple and profoundly effective philosophy: decentralization. Push daily decision-making as close to the customer as possible, give extraordinary customer service, empower people with responsibility, accountability, and shareholder-friendly incentives, and give them ample room to grow. Pair this with an obsession and passion for delivering exceptional customer value and rewarding great performance, and people go the extra mile.

English