AI/HPC MD

3.6K posts

AI/HPC MD

@BistrainJoseph

AI/HPC, Bitcoin mining, Health and exercise, retired MD $IREN $CIFR, $BITF, $EOSE

$IREN being named the flagship deployment for NVIDIA's DSX architecture at the 2GW Sweetwater campus is a massive deal. This validates IREN's vertically integrated approach across power, land, data centers and GPU operations, exactly what NVIDIA needs in a partner to scale AI infrastructure globally. This gives IREN the credibility to unlock institutional financing, attract hyperscaler deals, and secure priority GPU allocation. It's in NVIDIA's own interest for IREN to succeed, because IREN SW1 site is now expected to be their flagship showcase for DSX architecture.

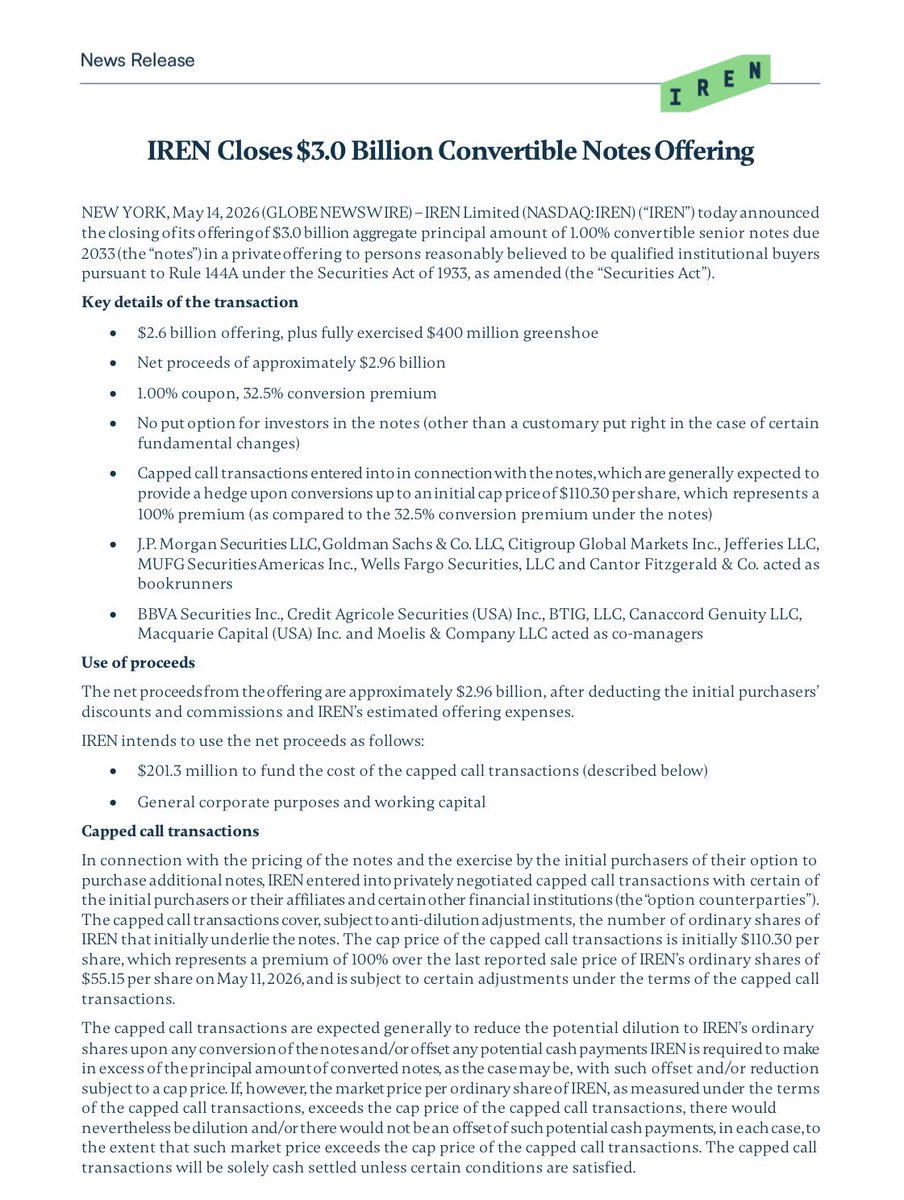

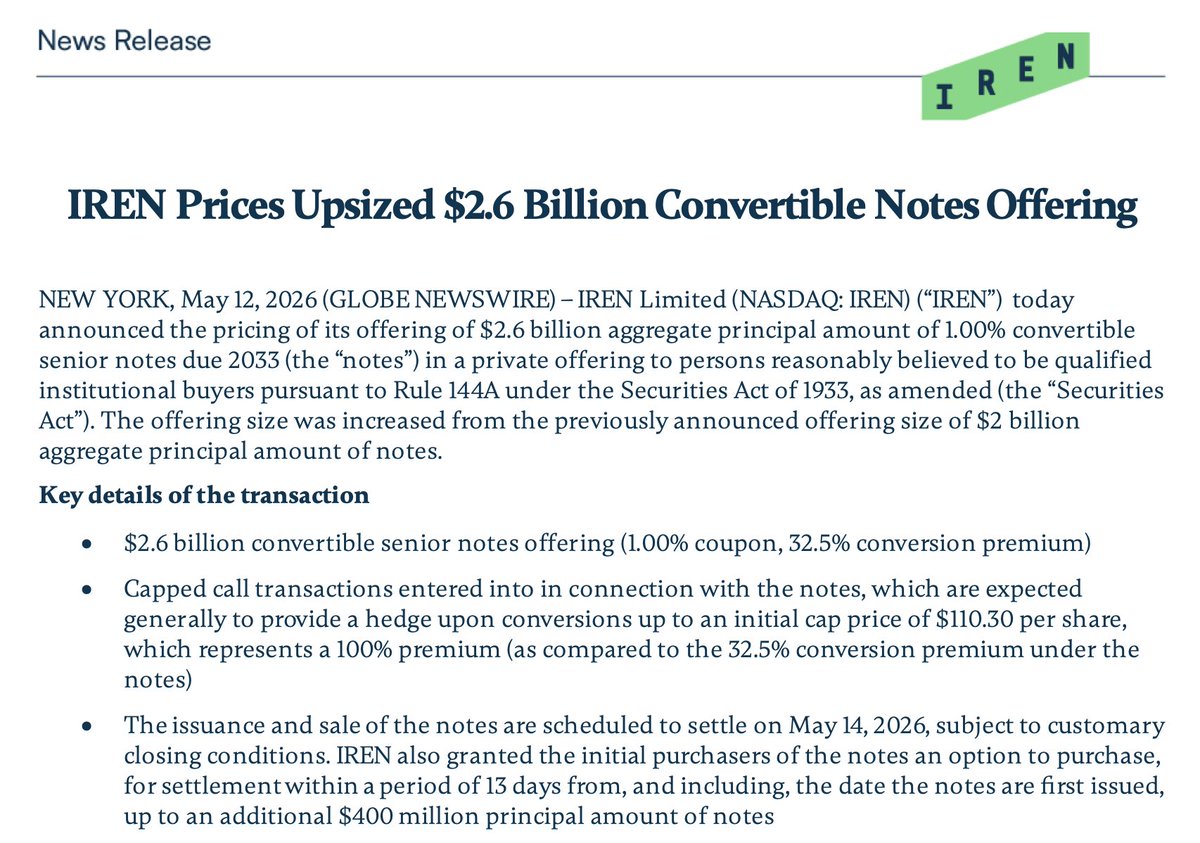

$IREN Prices Upsized $2.6 Billion 1% Convertible Senior Notes Due 2033 @IREN_Ltd announced the pricing of its upsized private offering of $2.6 billion in 1.00% convertible senior notes due 2033 (increased from the previously announced $2 billion). Key Terms: - Coupon: 1.00% (paid semi-annually) - Maturity: December 1, 2033 - Initial Conversion Price: ~$73.07 per share (32.5% premium to the $55.15 closing price on May 11, 2026) - Conversion Rate: 13.6848 ordinary shares per $1,000 principal - Capped Calls: Entered with a cap price of $110.30 (100% premium) to reduce dilution upon conversion Proceeds & Use: - Expected net proceeds: $2.57 billion ($2.96 billion if the $400 million option is fully exercised) - ~$174.5 million to fund capped call transactions - Remainder for general corporate purposes and working capital The notes settle on May 14, 2026. This move provides IREN with significant low-cost capital to support its AI cloud and data center growth.

$IREN Q3 FY26 Direction right, timing off. ═══ The Good ═══ 1. NVIDIA 5-year $3.4B contracted revenue - Childress 60MW air-cooled Blackwell + managed GPU cloud - $11.3M/MW unit pricing = +16% premium vs MSFT's $9.7M/MW - Not an option but 5-year locked-in revenue ($0.7B annual ARR) - Revenue recognition starting 2027 2. Elevated to NVIDIA's top 3 Neocloud picks - NVIDIA's chosen 3 to commoditize hyperscalers - CRWV, NBIS, and now IREN - "Selected partner" status, beyond mere customer - AI Factory design + DSX standard validation + ecosystem coordination 3. Commanding financing cost advantage - 95% of MSFT capex funded at ~3% blended rate ($1.9B zero-interest prepayment + GPU debt 6% weighted avg) - 1.5% convertibles, 6% GPU debt - Compare: CRWV 9% corporate. NBIS also pricier than IREN - Self-built datacenters = capital efficiency vs outsourced peers 4. 5GW global platform materialized - US 4.5GW + Spain Nostrum (490MW + GW+ pipeline) - Australia entry accelerating (APAC 4.8B population market) - 2026 480MW → 2027 1,210MW → 2030 5GW buildout - ERCOT batch 0 priority secured 5. Mirantis acquisition = full-stack AI Factory evolution - 650 engineers, 1,500 enterprise customers track record - Founding ISV partner of NVIDIA AI Cloud Ready - Cordon AI platform: bare-metal/VM/Kubernetes integration - From GPU rental → comprehensive cloud services - Direct support for NVIDIA contract delivery 6. Sophisticated NVIDIA $2.1B option structure - Fully vests only upon 600k GPU deployment - No immediate capital inflow = no immediate dilution - NVIDIA only benefits if IREN succeeds - $70 strike = +17% premium to current - Effectively option ↔ GPU delivery priority barter ═══ Real Bad ═══ 1. The real magnitude of the revenue miss - Street consensus $220M missed by -34% (actual $144.8M) - But the real shock vs company's own guidance: - Last year: "ARR $500M by now" guide - Actual quarterly AI revenue $33.6M = ~$120-150M ARR - About 1/4 of own promise (-75% miss vs own guide) 2. Horizon 1 delivery timeline pushed - Microsoft handoff slipped to Q3 CY2026 - Clear delay vs street consensus - Surface explanation: HBM/storage industry shortage - But mgmt didn't clearly address the why on the call - First tranche = IREN's first liquid-cooled trial, learning curve start - Risk: contract clauses if cure period also missed 3. Management language pivot - Previously: emphasized "ARR" - Now: emphasized "contracted revenue" + 2027/2028 plans - Signal that mgmt is aware of ARR guidance miss - ARR definition specifies "delivered, commissioned, and in service" - But 2026 $3.7B ARR target definition omits "in service" - Intentional wording difference = potential ARR-to-revenue gap 4. Time-to-compute moat in question - IREN's core competitive edge = converting compute to revenue fast - Missing own targets puts the moat itself in doubt - Even bull-side analysts called it "huge disappointment" - H2 2026 revenue recovery = moat existence test 5. ARR-to-revenue recognition gap - Three stages: delivered → commissioned → in service - Revenue recognition starts at in-service - Hyperscalers like Microsoft have lengthy acceptance protocols - Security, network, monitoring, performance criteria gates - Achieving $3.7B ARR ≠ $3.7B revenue in 2027 ═══ The Question ═══ If "time to compute" is the moat, missing your own targets puts the moat itself in question. H2 2026 AI revenue recovery is the real test. Direction (NVIDIA elevation, 5GW global, AI Factory standardization) is right. Tempo (-75% vs own guide, Horizon 1 delay) is off. NFA. Personal analysis log.

@mcF_dan Yeah that’s the same number I got for 2028 between $500-$750 a share… should be $150 by November December and $250-$300 next year

No, I actually don't think that is too optimistic. $IREN's SW1 can be a the first large scale 1GW+ deployment of the new Vera Rubin CPX designed for 800VDC from the ground up. developer.nvidia.com/blog/nvidia-80… Why does Jensen keep talking about 1GW+ AI factories? How many 1GW+ sites are there that will be energized by the time Vera Rubin CPX is release around end of 2026? nvidia.com/gtc/dc/keynote… This rendering doesn't have the wind turbines in the background that SW1 would have, but it is definitely from a Southwestern US climate. 🤔😂