Domien Van der Elst

822 posts

Domien Van der Elst

@DomienVdE

Founder and teacher at https://t.co/xRQI8kC7vM, physics and statistics lecturer at University of Antwerp, member of Les Meccs (Belgian Canyoning Expedition Team)

Belgium Katılım Nisan 2012

109 Takip Edilen977 Takipçiler

Every website you’ve ever used is broken in a way you never noticed and it’s been this way for 30 years...

A Midjourney engineer finally just fixed it.

It’s called Pretext:

A tiny library that lets websites lay out text the way magazines and newspapers do, with text flowing around images, wrapping into columns, and fitting perfectly into any shape, all at 120fps.

This has been basically impossible on the web for 30 years. Every website you’ve ever used relies on the same clunky system from the 90s to figure out where text goes on screen. Pretext bypasses it entirely. 500x faster.

The demos look like they shouldn’t be possible in a browser. Go look.

Cheng Lou@_chenglou

My dear front-end developers (and anyone who’s interested in the future of interfaces): I have crawled through depths of hell to bring you, for the foreseeable years, one of the more important foundational pieces of UI engineering (if not in implementation then certainly at least in concept): Fast, accurate and comprehensive userland text measurement algorithm in pure TypeScript, usable for laying out entire web pages without CSS, bypassing DOM measurements and reflow

English

This is a clear example of different types of thinking. “We haven’t seen it yet” is emblematic of people who need to see it to believe it. There’s nothing wrong with that, it’s just a person analyzing the present, without foreseeing the future. As a founder, I can assure you: some things need to be believed to be seen. You have to imagine the future you want, believe it’s possible and then make it come true. Those who don’t see that future will not understand what you are doing.

In Lemonade’s case, you don’t even need a lot of imagination anymore. Just calculating the lifetime value of a customer using current metrics shows the acquisition cost is a profitable investment.

Neil 𝕏@Neil_X10

$LMND reasoning with first principles > reasoning by analogy

English

🚨FLASHBACK FRIDAY

Exactly 5 years ago, after publication of the Q4 2020 results, @PaperBagInvest made a video titled "Lemonade 5 year price target" (youtube.com/watch?v=pxMmw9…). So, it's time to be nostalgic and look back! You can find a summary of his predictions below.

❌Gross Earned Premium:

Full year '20: $159M

PBI projection for Full Year '25: $2,098M

Actual Full Year '25: $1,051M

❌ Net Income:

Full year '20: $-127M

PBI projection for Full Year '25: $235M

Actual Full Year '25: -$166M

❌ Market cap:

5 years ago: $5.58B

PBI projection for end of '25: $11.73B

Actual end of '25: $5.32B

Now: $4.20B

So the market cap dropped 25% in the past 5 years, but the stock price fell even more due to dilution: 41%.

5 years ago: $92.90

Now: $55.04

Clearly, Paper Bag was too optimistic (as was I). But he had the courage to publish his honest thoughts and has continually adjusted his insights and projections ever since, plugging all new developments into his $LMND model. It's the #1 Lemonade resource out there, which you can get access to by supporting him on Patreon.

It's amazing to me how much the business has improved, while the valuation has declined. It's probably because you still have look around the corner, beyond the current financials, to see Lemonade's value. I think we can acknowledge the stock price was inflated 5 years ago and I was too optimistic for the short term. But, as I've said in the past, I'd rather be too early than too late! And I'm happy to have been on this rollercoaster with amazing people.

The Lemonade team is doing great work, reimagining both the way you buy and use insurance, as well as how to run a business in the age of AI. I'm still convinced they will realise the potential I saw in 2020 and this will become increasingly more obvious.

Here's to the next five years! 🍻 And thank you for bringing us all together @daschreiber @shai_wininger

YouTube

English

Thank you for attracting my attention to book value.

You make a clear prediction: Lemonade will need to raise capital if they continue to grow top line 32%+ YoY in the coming years, which is what they project. Management on the other hand has said they might raise capital in the future but they won’t need to.

So could you narrow your prediction down? If they sustain their growth rate, by what date will they need a capital raise?

English

Would reply..but Im exiled from the community. So a quote tweet

A year ago I was told book value was a stupid metric to value LMND. So this post is progress. But the comparison is way off. For an insurance company with an opaque portfolio, book value and book value per share matter even more because it is precisely the book value and its trend that indicate whether the growth can be maintained. This is why you can compare or value an insurance company like, say, a tech company. The scenario provided makes sense for a high-growth company... but for an insurance company, they have a natural governor....the book value. When you push the envelope of regulatory risk-based capital, then the retained earnings need to match the top-line growth. YOU cant just grow top line 20-30% a year while your book value is shrinking. At some point you cry uncle. There is a natural gravity for financial institutions that have opaque portfolios. Risk based capital is the solution to prevent them from growing so big so fast that they cant pay their claims and they go insolvent. Book value per share (and its trend) is the only KPI that provides a snapshot of todays health and an indicator of future potential.

The Andover Companies is a New England holding company for 3 mutuals. They have a net surplus (statutory book value) of over $2 Billion and premiums of just under $1 Billion. This company can grow as fast as they want, when they want, with little concern. LMND is pushing the upper boundary of their growth model because the premium to book value is going to exceed regulatory limits. Can they navigate around it? yup. But not without more capital. Even if they become profitable, I dont see how they can retain enough earning to organically maitaintain their growth rate. They will need to raise capital. Maybe its another equity offering. Maybe its a surplus note. But this current trend cannot be sustained. This is a movie that has played out before...many times. And the ending is always the same.

But this is progress. At least the bulls are finally acknowledging book value matters.

Domien Van der Elst@DomienVdE

So... let's talk about $LMND's book value (assets minus liabilities), which is an important metric for insurance companies. Lemonade's book value is still declining. This point is often made by bears, who don't see/believe how Lemonade will turn this around. Moreover, Lemonade's own guidance for 2026 means book value will decline even further in the coming year. While this is certainly something to keep an eye on, there are some additional factors to consider. First of all: book value doesn't work well for valuing fast-growing companies that spend a lot of money on advertising. The biggest problem is the fact that a customer base is not accounted for as an asset, even though it does have value. For a growth company like Lemonade that will spend $225M(!) on advertising next year, this creates a distorted picture. Take these two examples: A company buys a machine for $1000 that will eventually generate profit before it wears out. Impact on book value at the moment that $1000 is spent? $0, because cash goes -$1000 but in its place comes the asset “machine” worth $1000. A company “buys” a customer by spending $1000 on advertising. That customer will eventually generate profit before he stops being a customer, just like the machine. Impact on book value at the moment that $1000 is spent? -$1000, because the acquired customer is not seen as an asset! To value Lemonade properly, you need to take the value of the customer base into account. A simple way @PaperBagInvest has implemented in his model, is multiplying the current customer count by the LifeTimeValue (LTV) of each customer. This gives an "adjusted book value" that is much larger, and growing! However, you need to be careful when interpreting this, because the current customers have already generated part of their LTV in the past, so the current/future value of those customers is smaller than their LTV. A second thing to consider is the structure of Lemonade's borrowings under their "Synthetic Agent" program. This is currently a $158.1M liability. They have used this money to acquire customers. These loans are structured such that they are paid back by a portion of the premiums paid by these acquired customers. If those premiums are insufficient, the loan doesn't have to be paid back! So what does this mean for the accounting? The acquired customers are valued as $0 on the balance sheet. Yet, if they were truly worth $0, meaning they wouldn't generate income in the future, then the $158.1M liability wouldn't need to be paid back! So the accounting has the worst of both worlds: a $0 asset and a $158.1M liability, which are contradictory to each other. With growth spend ramping up throughout 2026 and beyond, maybe these aspects are worth emphasising on the next Investor Day? @tebixby @daschreiber

English

So... let's talk about $LMND's book value (assets minus liabilities), which is an important metric for insurance companies.

Lemonade's book value is still declining. This point is often made by bears, who don't see/believe how Lemonade will turn this around. Moreover, Lemonade's own guidance for 2026 means book value will decline even further in the coming year. While this is certainly something to keep an eye on, there are some additional factors to consider.

First of all: book value doesn't work well for valuing fast-growing companies that spend a lot of money on advertising. The biggest problem is the fact that a customer base is not accounted for as an asset, even though it does have value. For a growth company like Lemonade that will spend $225M(!) on advertising next year, this creates a distorted picture. Take these two examples:

A company buys a machine for $1000 that will eventually generate profit before it wears out. Impact on book value at the moment that $1000 is spent? $0, because cash goes -$1000 but in its place comes the asset “machine” worth $1000.

A company “buys” a customer by spending $1000 on advertising. That customer will eventually generate profit before he stops being a customer, just like the machine. Impact on book value at the moment that $1000 is spent? -$1000, because the acquired customer is not seen as an asset!

To value Lemonade properly, you need to take the value of the customer base into account. A simple way @PaperBagInvest has implemented in his model, is multiplying the current customer count by the LifeTimeValue (LTV) of each customer. This gives an "adjusted book value" that is much larger, and growing! However, you need to be careful when interpreting this, because the current customers have already generated part of their LTV in the past, so the current/future value of those customers is smaller than their LTV.

A second thing to consider is the structure of Lemonade's borrowings under their "Synthetic Agent" program. This is currently a $158.1M liability. They have used this money to acquire customers. These loans are structured such that they are paid back by a portion of the premiums paid by these acquired customers. If those premiums are insufficient, the loan doesn't have to be paid back! So what does this mean for the accounting? The acquired customers are valued as $0 on the balance sheet. Yet, if they were truly worth $0, meaning they wouldn't generate income in the future, then the $158.1M liability wouldn't need to be paid back! So the accounting has the worst of both worlds: a $0 asset and a $158.1M liability, which are contradictory to each other.

With growth spend ramping up throughout 2026 and beyond, maybe these aspects are worth emphasising on the next Investor Day? @tebixby @daschreiber

English

MY THOUGHTS ON LEMONADE'S 2026 GUIDANCE:

In the recent $LMND space with @Neil_X10, I shared my impression that Lemonade's guidance is often incompatible with itself, because they want to give themselves optionality. In particular: if they spend little on acquiring customers, it hurts IFP but it helps Adj. EBITDA (in the short term). Conversely: if they spend a lot on acquiring customers, you get high IFP but bad Adj. EBITDA. So...

When guiding for IFP, they want to be cautious and have the LOW growth scenario in mind, because they don't want to miss their own guidance. But when they guide for Adj. EBITDA, they have the HIGH growth scenario in mind, which has worse Adj. EBITDA. Even then, they often beat both guides... Which is why I have a hard time understanding @daschreiber when he says they guide as accurately as possible. Maybe I just have higher expectations of the Lemonade team than he does 😅

I think they have done this again for 2026. They guide for 32% YoY IFP growth for Full Year 2026 (31.6% in fact). Yet, in the earnings call, @tebixby spoke about 32% IFP growth rate in Q1 '26 AND the goal of increasing that rate quarter over quarter. So let's say 33% YoY IFP growth rate in Q2, 34% in Q3 and 35% in Q4. This hypergrowth scenario might help explain the low Adj. EBITDA guide. But even then, it seems unlikely to me FY Adj. EBITDA would be as low as their guide. Maybe they want to grow even faster? 🤔

@PaperBagInvest: Can you run the numbers? What growth rate would be needed to have -50M Adj. EBITDA (their guide) for FY '26?

English

Gone are the days where $LMND needed to cherry-pick what to put in the shareholder letter. Nowadays, everything is awesome!

Congrats @daschreiber, @shai_wininger and the entire team!

Read the letter here: lemonade.com/investor-relat…

GIF

English

Time to put a number on it. I’m guessing 56% Gross Loss Ratio for Q4 ‘25, which would be insanely low!

We’ll see tomorrow! $LMND

Drop your guess below 👇

Domien Van der Elst@DomienVdE

Consider there must have been quite a big head start for @daschreiber to declare on the last earnings call they were on track to have record low gross loss ratio in Q4. He wouldn’t say that if it were close. I expect Q4 ‘25 Gross Loss to definitely be below 60%. I’m not counting on positive Adj. EBITDA for Q4 ‘25, but I’m counting on positive Adj. EBITDA for Full Year 2026, despite @daschreiber’s statement that would only come in ‘27. For me the next shareholder letter is all about the Adj. EBITDA guidance for Full Year 2026, and I hope they set it at $0! It’s such a beautiful target! 🤩 Having said that, I prefer they spend as much as possible on profitable growth even though that makes Adj. EBITDA worse in the short term.

English

Yeah, meanwhile @elonmusk just said in an interview "short term video" is an invention that made our lives worse...

If I were in charge, I would replace the general "like" heart with two reaction buttons: "fun" and "interesting". And then have a slider in the UI to control how much "fun" stuff and how much "interesting" stuff is in your feed. I want to use X solely for interesting stuff.

English

@DomienVdE I'm not enjoying my feed at the moment either. Seems rather tiktok-y rather than substantive/intellectual. I'm trying to intentional skip past the dumb stuff and spend more time on the better posts to train the algo.

I'm not a fan though, this is annoying.

English

I’m seeing a lot of violent videos in my X feed. Is it just me? I don’t like it but I don’t know how to get rid of them.

English

Great web page by the way!

I love @Lemonade_Inc’s taste!

@audrey_zada @shai_wininger

Anyone else I should tag?

$LMND

Shai Wininger@shai_wininger

And... we're ON. @Lemonade_Inc's Autonomous Car for @Tesla FSD is now live in Oregon. Tesla drivers in Oregon can now get ~50% off their Tesla FSD-driven miles + the best car insurance experience in the US, bar none. lemonade.com/fsd

English

@shai_wininger is motivating the team toddler style 🤪

“You better get ready to ship! I’m gonna count to Oregon!” 😆

Shai Wininger@shai_wininger

E

English

Consider there must have been quite a big head start for @daschreiber to declare on the last earnings call they were on track to have record low gross loss ratio in Q4. He wouldn’t say that if it were close. I expect Q4 ‘25 Gross Loss to definitely be below 60%.

I’m not counting on positive Adj. EBITDA for Q4 ‘25, but I’m counting on positive Adj. EBITDA for Full Year 2026, despite @daschreiber’s statement that would only come in ‘27.

For me the next shareholder letter is all about the Adj. EBITDA guidance for Full Year 2026, and I hope they set it at $0! It’s such a beautiful target! 🤩

Having said that, I prefer they spend as much as possible on profitable growth even though that makes Adj. EBITDA worse in the short term.

Paper Bag Investor@PaperBagInvest

How low could the Q4 loss ratio go? And could it result in breakeven or positive Adjusted EBITDA for Q4?? I'm beginning to think it's more possible than I had previously considered. Progressive, All State and Travellers all had very low CAT loss ratios in Q4 and compared to Q4 2024 they were very similar or even better. $LMND in Q4 2024 only had 1% of CAT. One percent! If Lemonade has 1% of CAT again and Gross loss ratio ex-CAT continues its improvement trajectory and goes to say 54%, then we could have 55% GLR overall for Q4. If that happens ... Adjusted EBITDA will be very close to breakeven or possibly even positive. I'm still not expecting positive Adj. EBITDA in Q4, but the probability is rising. 👀

English

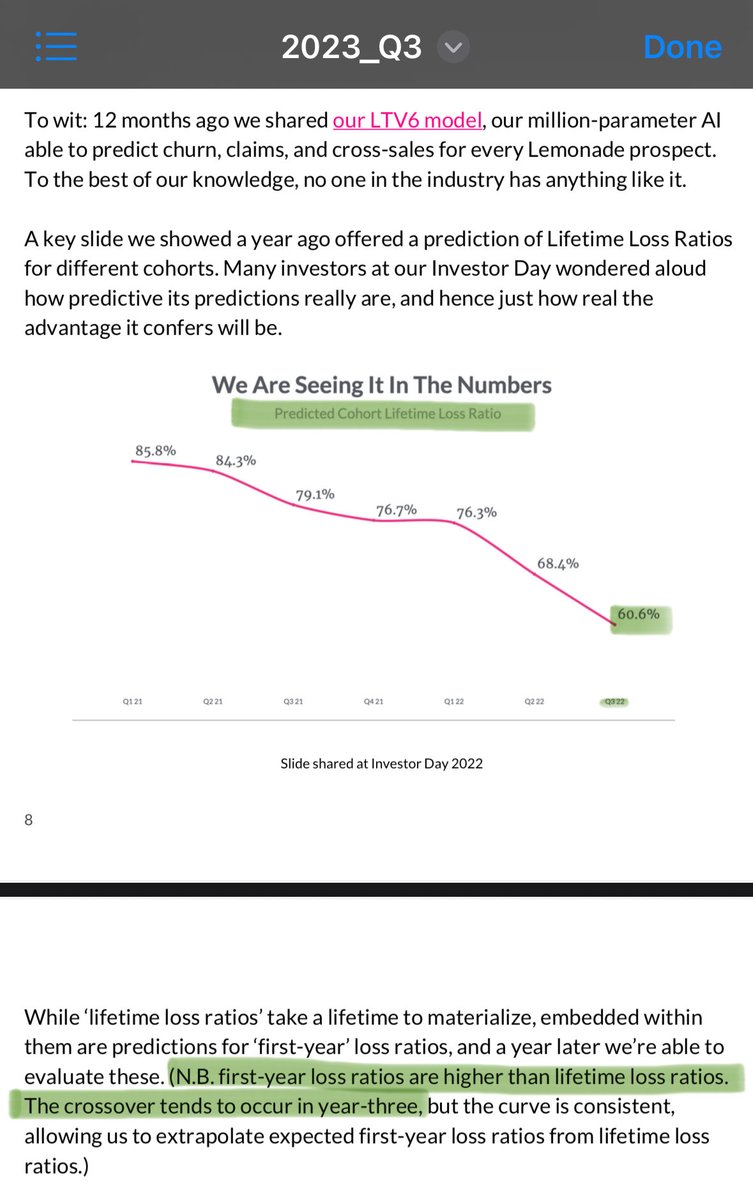

I agree with @PaperBagInvest. Moreover, looking back at the Q3 ‘23 shareholder letter, Lemonade reiterated their prediction of 60% lifetime loss ratios for customers acquired in Q3 ‘22, with initial loss ratios being higher and dropping below 60% in year-three. So a bunch of customers should be at <60% loss ratios by now! 🤩

Paper Bag Investor@PaperBagInvest

REMINDER: $LMND Q4 loss ratio will likely be the lowest it's ever been. Why? Daniel said it will be if nothing unexpected happens... And ... nothing unexpected did happen. We had minimal catastrophic (CAT) events in Q4. $PRG numbers for Q4 CAT are very low. So, how low might it go? Q3 Gross Loss Ratio ex-CAT was 56% and 62% with CAT. If Q4 baseline improve slightly, say to 54% and we have less CAT than Q3, we may see < 60% loss ratio for Q4 ...

English