Sabitlenmiş Tweet

Officially sold all my $VRT. 730%+ gain realized in my ROTH IRA. Time to find the next man up! Ideas?

English

Rightsized CapStack Capital

10.6K posts

@CapstackCapital

Master of EBITDA Adjusting ~ Industrials / A&D ~ Semis / AI ~ LMEs / RX ~ Unapologetically Catholic ✝️ ~ #GoBruins 🐻💙💛 ~ #BillsMafia ~ ≠ investment advice

Every investor who bought Cerebras on the hype yesterday is now deeply in the red. Great job, Wall Street. Sold to you, retail. Even insiders were wincing at the ridiculous opening valuation.

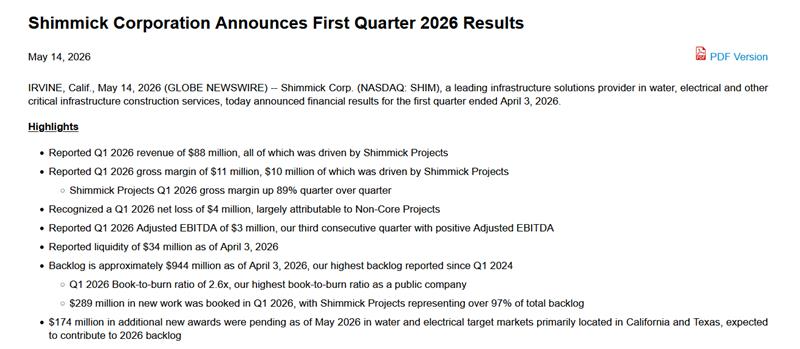

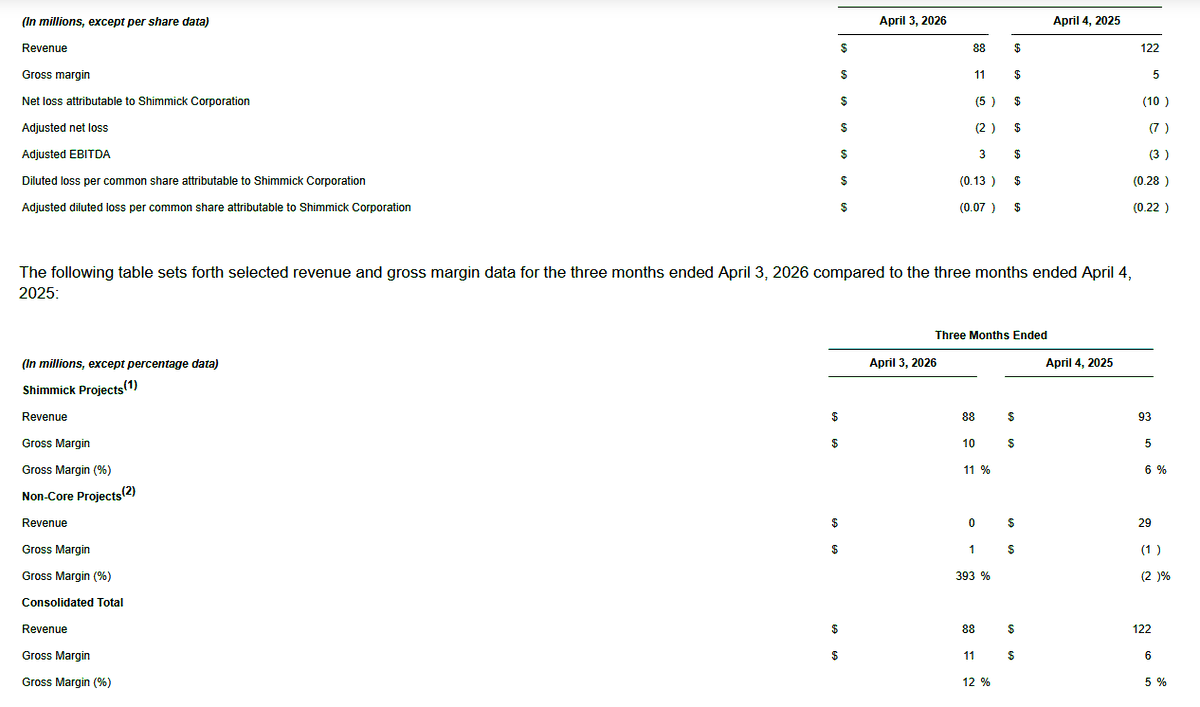

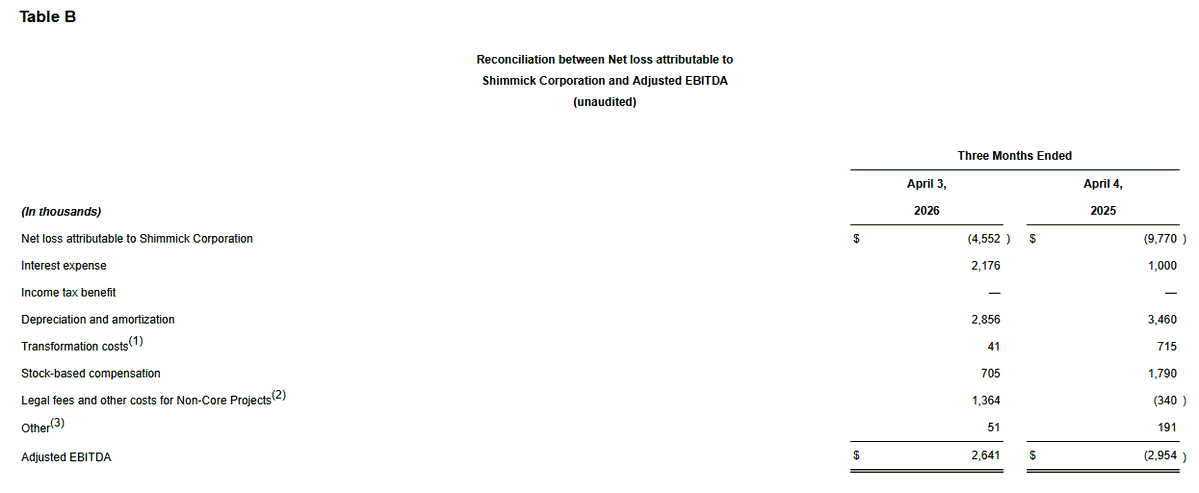

$SHIM Q1'26 Earnings are out. Backlog of ~$944mm, highest since Q1'24. Adj. EBITDA of $3mm, continues to improve. Gross Margin increased significantly, despite lower YoY revenue. 2.6x Book-to-Burn, its highest ever as a PubCo. +$289mm of new awards in Q1'26 +$174mm of additional awards pending as of May 2026 in Water & Electrical target markets. Really great development. FY26 guidance was reaffirmed: Revenue: $550mm - $600mm (+17% YoY @ mdpt) Adj. EBITDA: $15mm - $30mm (+350% YoY @ mdpt)

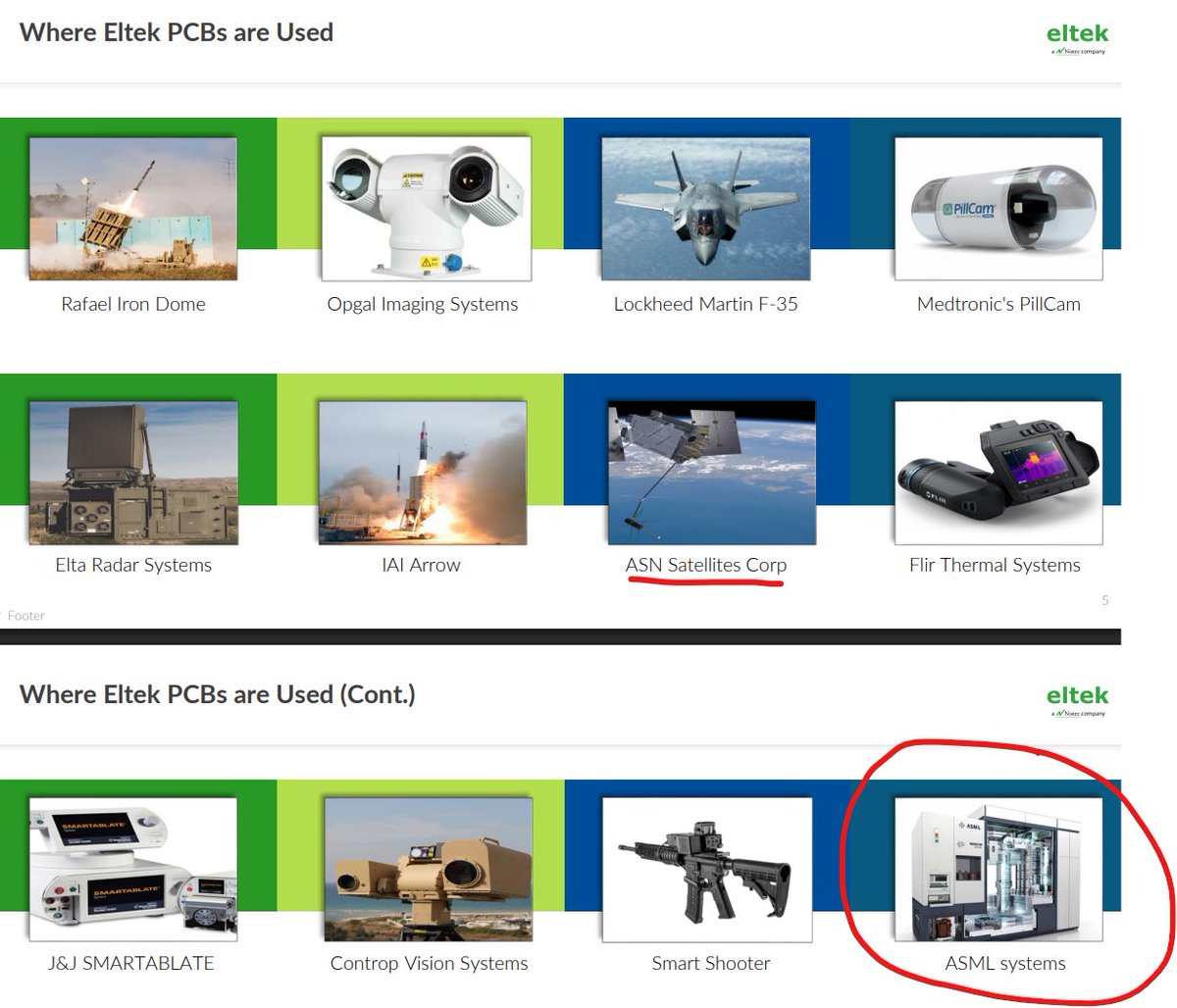

Big week of earnings on deck for me this coming week. $AP - Pre-Market Tues, 5/12; Call @ 8:30am $SHIM - AH Thursday, 5/14; Call @ 4:30pm $SPCB - Pre-Market Thursday, 5/14; Call @ 10:00am