Goderguy

1.2K posts

Goderguy

@Goderguy

making drugs & havin fun. prev L/S analyst

$LODE second permit received. Now fully permitted. PR also states they are on schedule for commissioning in Q1. Next big derisking will be proving that the tech works as they say it does when scaled up.

Love seeing external teams succeed—Onava just published their Latent-X1 binder results! Using the Latent Labs Platform to design proteins in the web browser, the team around Sharrol Bachas was able to design binders against a particularly challenging immune target. They completed design-lab loops in just 7 days! Key highlight: Nanomolar-strength binders with high target specificity, outperforming that of other approaches in their lab comparison. Of course we just launched Latent-X2 now enabling drug-like antibody design. Reach out if you'd like to explore what that could mean for your pipeline. See their preprint here: biorxiv.org/content/10.648…

preface: 99%+ of my net worth is tied up in the #bittensor ecosystem. I admire and actively support multiple subnet teams, and I am 100% allocated to subnets within the $TAO ecosystem (0% to root). I run a fund dedicated to subnet investment, so I quite obviously believe in the amazing potential the protocol possesses. with that out of the way: I met with the principals of a large ($5B+) multi-family office on Thursday. I passionately pitched them the Bittensor ecosystem. multiple subnets. they loved it. “send me more info. we move quickly.” they are heavily invested in the tech start-up space. what better place to deploy capital than subnets? what space could be more a) interesting from an intellectual perspective and b) attractive from a risk/return standpoint? I am close to rescinding that recommendation. since that meeting (in just the past 48 hours), the $dTAO mechanism is changing *yet again.* apparently taoflows (and associated chain buys) are benefiting the wrong subnets. let’s just say it: nobody wants sn8 to win. I witnessed the founder of the protocol jeet the entirety of his sn8 holdings yesterday, probably in an effort to stop chain buys. cool. your choice. but that didn’t work. so let’s change the protocol, and give validators the power to choose which subnets get chain buys (arguably undermining the purpose of dynamic TAO). the college football playoffs started this weekend, so here’s a metaphor. you’re a football coach (subnet owner). you recruit your team. you expend the right resources in the right places. you come up with the perfect plays based on the (publicly agreed upon and accepted) rules of the game. everything works. your star QB has an amazing drive downfield and you end up in the red zone. you have a play just for this scenario. the O line executes. your WR gets in the perfect spot. the QB connects. TOUCHDOWN!! not so fast. joke’s on you mf’er. the goalposts moved. some football OG’s have been monitoring the situation. the end zone isn’t there anymore. other end of the field papi. would you ever play the game again? of course not. how do you build an organization if the rules are fluid? how do you recruit investment if things constantly shift and change? uncertainty is the death knell for an investment class. I say this reluctantly because somebody has to: if #bittensor wants to be ready for institutional capital, it needs to make a decision. is it a decentralized protocol or not? let us know please. there are certainly *subnets* that are crushing it and ready for institutional capital. they have game plans and they are executing. but they are succeeding in spite of, not because of, the constant changes to the dTAO protocol. if Bittensor is going to be truly decentralized, it needs to decide now. otherwise we are just another extraction L1. #bittensor $TAO $dTAO

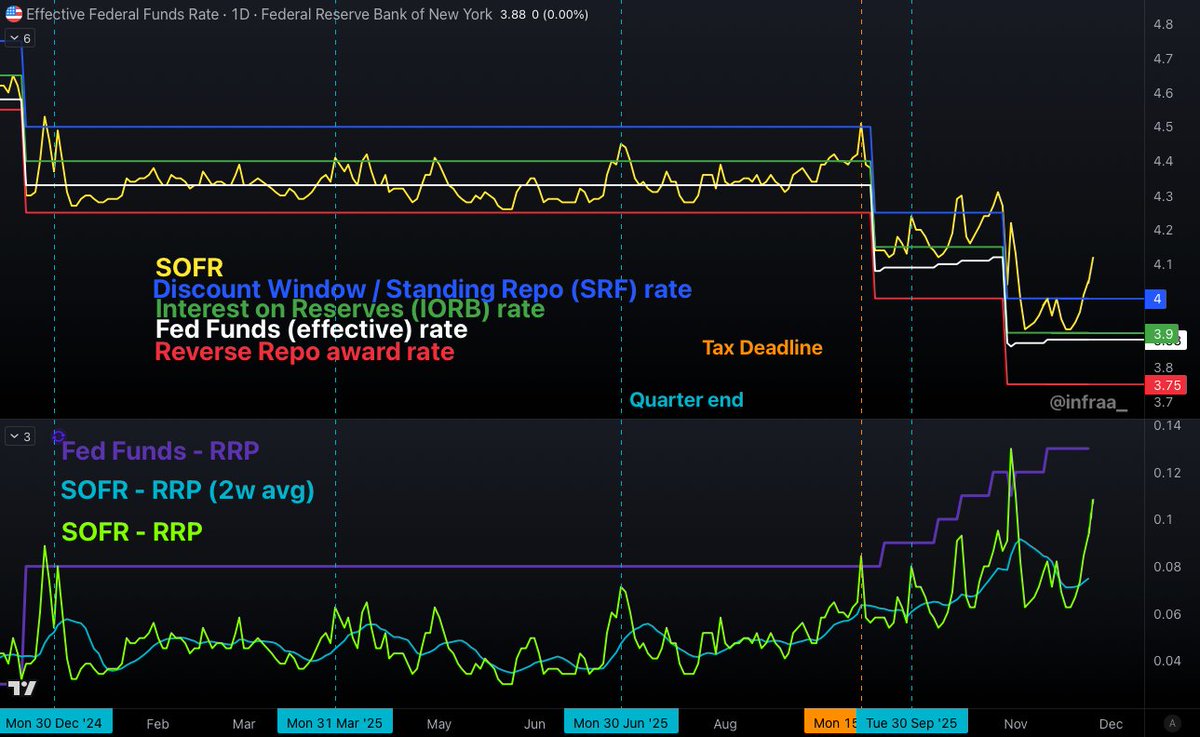

Secured overnight financing rate: 4.12% November 28th vs 4.05% November 26th

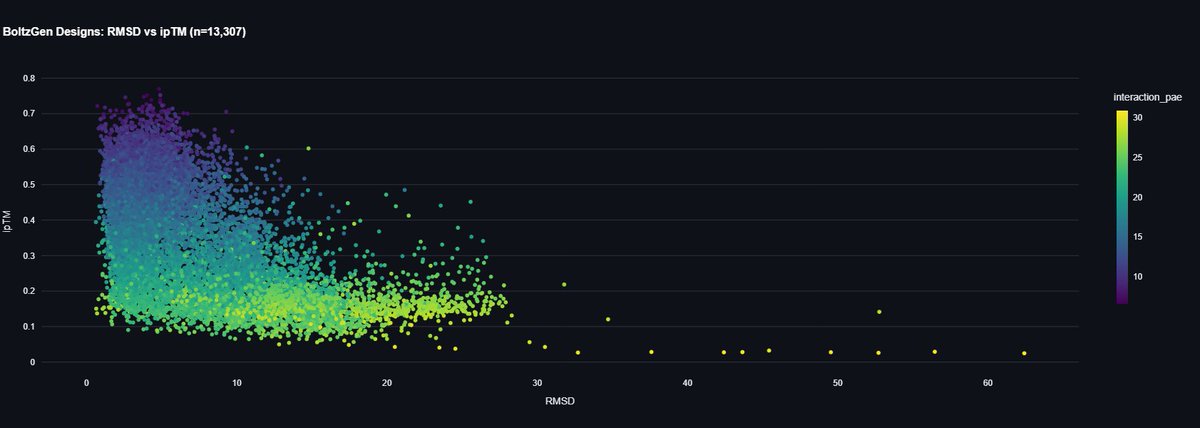

x.com/owl_posting/st… Good catch from @Owl_Posting missed in the initial Chai/JAM comparisons — looks like JAM-2’s affinities are consistently 1-2 OOM better than Chai-2s, which is a big gap and key to whether de novo antibodies are good enough to go directly into animals 🧵…

$TWST $NTRA @standuquesne --- super important commentary that is not priced in. If $TWST competitors are having commercial supply issues to the point where companies like $NTRA are considering very expensive revalidation using $TWST that is a major signal. Wouldn't be surprised if one of the best investors in the world caught this. The question is will you before it is announced?