M retweetledi

The Matrix was right about human civilization peaking in 1999

English

M

6K posts

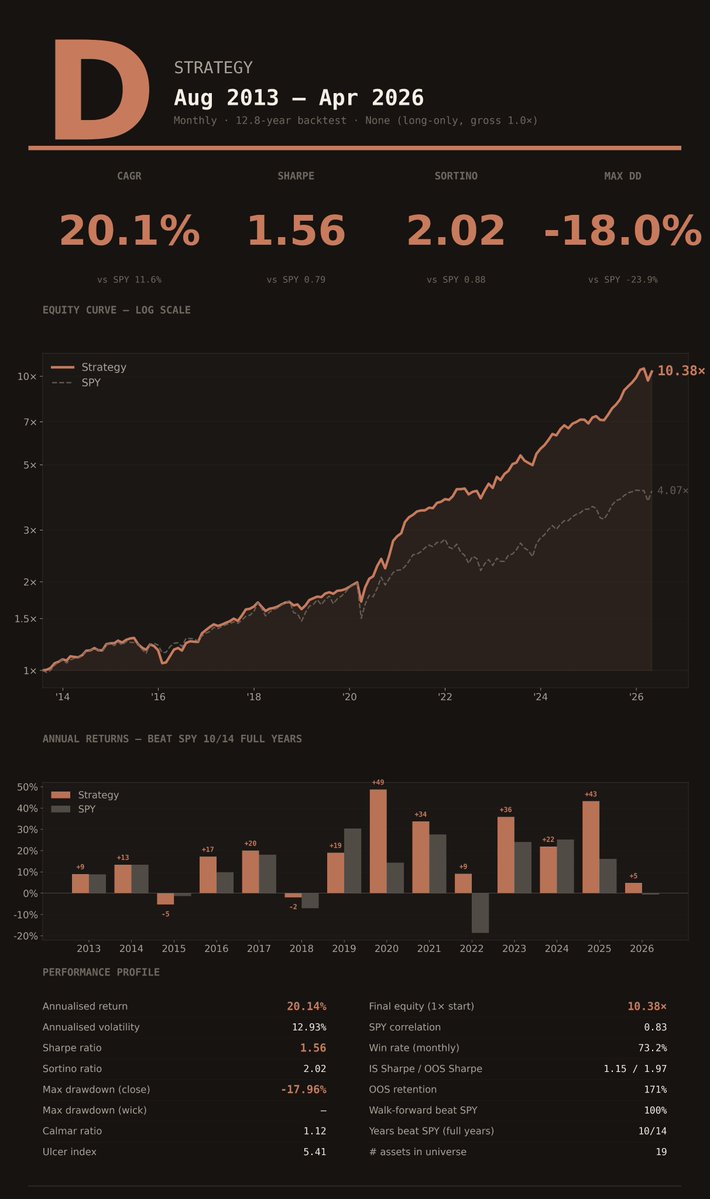

So - would any of you want this strategy for free? (though you are welcome to buy me a Guinness) Beats buy-and-hold SPY with significantly less vol and shallower drawdowns. Unlevered & long-only. I am not offering this purely out of the goodness of my heart but because I am already employing *much* stronger iterations of this and feel like many are paying absurd monthly fees for levered beta (although also a little out of the goodness of my heart) If there is interest, I'll publish allocations/signals wherever is preferable

🔥 "Leverage for the Long Run" Ganador del Charles H. Dow Award 2016, este paper rompe todo lo que pensás sobre apalancamiento Analizan qué pasa si en lugar de hacer buy and hold del S&P 500 desde 1928, usás leverage SOLO cuando el mercado está arriba de la media móvil de 200 días, y te vas a bonos del tesoro cuando está abajo Lo más interesante es que rompe el mito de que los ETFs apalancados se van decayendo con el tiempo por naturaleza. Lo que mata al leverage no es el tiempo, es la volatilidad alta y los mercados en serrucho. Cuando aplicás leverage en zonas de baja volatilidad con rachas de días positivos seguidos, pasa todo lo contrario a lo que la gente cree El número es una locura: $10.000 metidos en 1928 con buy and hold del S&P 500 te quedan en $39 millones. La misma guita con la estrategia 3x leverage rotation te termina en $28 billones, con drawdowns más chicos y mejor Sharpe La clave es simple: arriba de la 200 MA, leverage on. Abajo, cash. Nada más Link al paper en el primer comentario

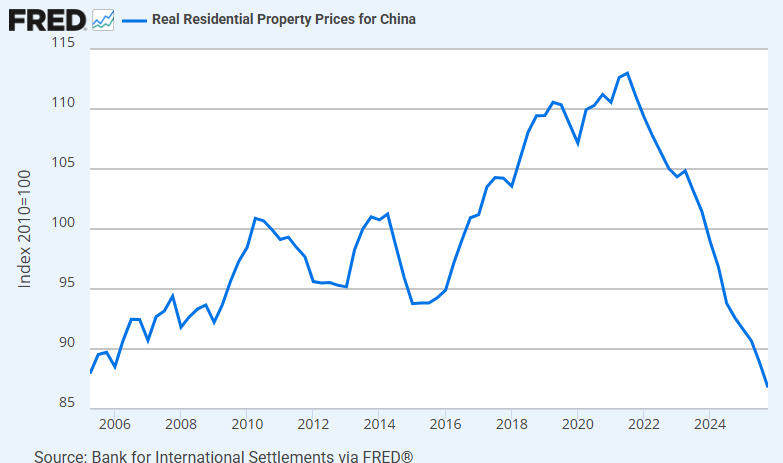

🚨 China's Real Estate Market has erased all gains from the last 20 years

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time. He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100% of his returns are alpha. He says today's market has so many similarities to 2000, "the easiest bear market I've ever seen in my whole life." He makes the case for going long dollar-yen, why Bitcoin beats gold as an inflation hedge, and why he was wrong about Warren Buffett. But what I'll remember most from this conversation is Paul's zest for life. He's 71 and still wakes at 2:30 every morning to trade the London open. He works out for two hours a day. He walks with his wife every evening. He travels the country chasing peak spring and peak fall. He's so excited about the songs picked for his funeral that he wishes he could be there to hear them. Paul has lived five lifetimes in one. He's one of the most entertaining and interesting people I've met, and the conversation will leave you searching to be as passionate about what you do as he is about what he does. Enjoy! Timestamps: 0:00 Intro 1:00 The Kindest Thing 13:19 Trading vs. Investing 17:33 Lessons from Warren Buffet 22:24 The Existential Risks of AI 29:54 The Nature of Trading 31:46 Bitcoin 35:55 Bubbles 42:08 A Day in the Life of PTJ 46:00 Information Overload 47:07 Passion for Markets 50:49 The Robin Hood Foundation 54:18 The Workless World 56:03 Journalism 1:00:00 Principal Components of a Great Life 1:05:06 Kill Them With Kindness

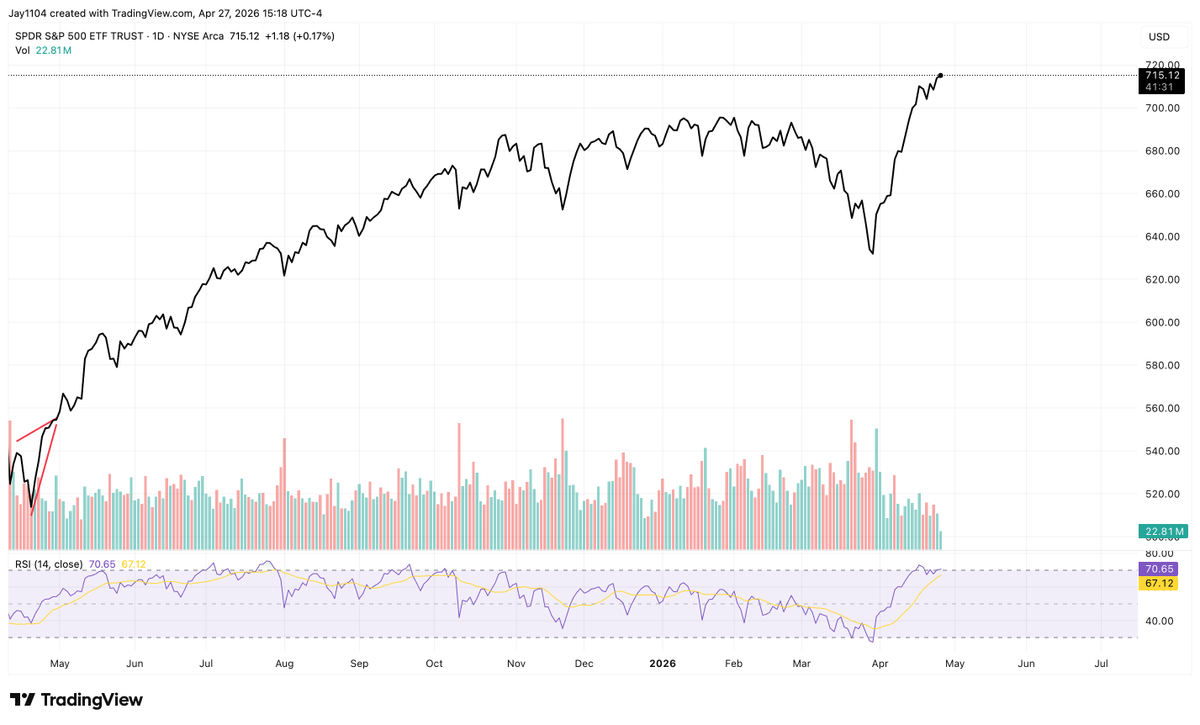

S&P 500 IS NOT AS STRONG AS IT LOOKS The price keeps going up - awesome! BUT The RSI is in a downtrend, as well as the OBV And this gap between the price and the actual state of affairs is exactly what distribution looks like before a significant peak forms From here I expect distribution with a possible bounce to $7,300 to trap the last buyers Either way, the final result is flush crash just like in October 2025