InTheTrenches 🙏

4.3K posts

InTheTrenches 🙏

@InTheTrenches2

Biotech investor. Tweets are my opinion, not financial advice.

Katılım Eylül 2010

132 Takip Edilen568 Takipçiler

$XBI

Next Round of Fruity Rapid Fire Takes Coming Up

Taking ticker requests now

English

get a talk show already — call it “Doc Marty” — and leave the FDA alone, please?

Dr. Marty Makary@DrMakaryFDA

Thank you, @AHIPCoverage! Enjoyed discussing FDA’s role in cutting red tape and bringing more affordability to healthcare.

English

InTheTrenches 🙏 retweetledi

Ok, this is all snapping into focus.

And candidly, the picture that's emerging is far more interconnected than anyone assumed re: what's happening to $QURE AMT-130 and the broader rare disease ecosystem.

This also seems to explain Vinay Prasad's abrupt (second) resignation.

If all this adds up — there's a specific law within the Standards of Ethical Conduct that becomes very relevant: 5 CFR § 2635.502, "The Impartiality Rule."

To be clear, this is not an accusation — simply following the paper trail.

Everything here is drawn from public records, sources at the bottom.

Ok, let's start...

Peter Mantas@peter_mantas

Funny little fact pattern. 1.Szarama wrote the Arnold Ventures letter arguing against external controls in December 2023; 2.She was appointed CBER Deputy Director October 8, 2025; 3.FDA rug pulled on AMT-130 22 days later; 4.No public recusal record exists. @adamfeuerstein @LizzyLaw_ @SenRonJohnson @SenBillCassidy @RepJasonSmith @RepAuchincloss @SenateAging

English

@Runki10top Nice! Which platform do you prefer for stock predictions?

English

@RNAiAnalyst They’d probably stack the AdCom with mini-Vinays. (See the vaccine advisory committee)

English

$qure here is a suggestion: let the company submit the BLA, hold an AdComm with leading experts in HD and then decide over the application.

Prasad believes that he knows better about Huntington's Disease and the AMT-130 data than the experts...even before looking into it (there have been cryptic comments by him on the subject in spring 2025 already'). Maybe he should not be called a 'genius' by Quakary all the time as he starts believing it.

English

@medstudentinvst Thanks for all your thoughts on $PRME, $PEPG, $NKTR and others. Will be looking to take a position in $PRME near-term.

English

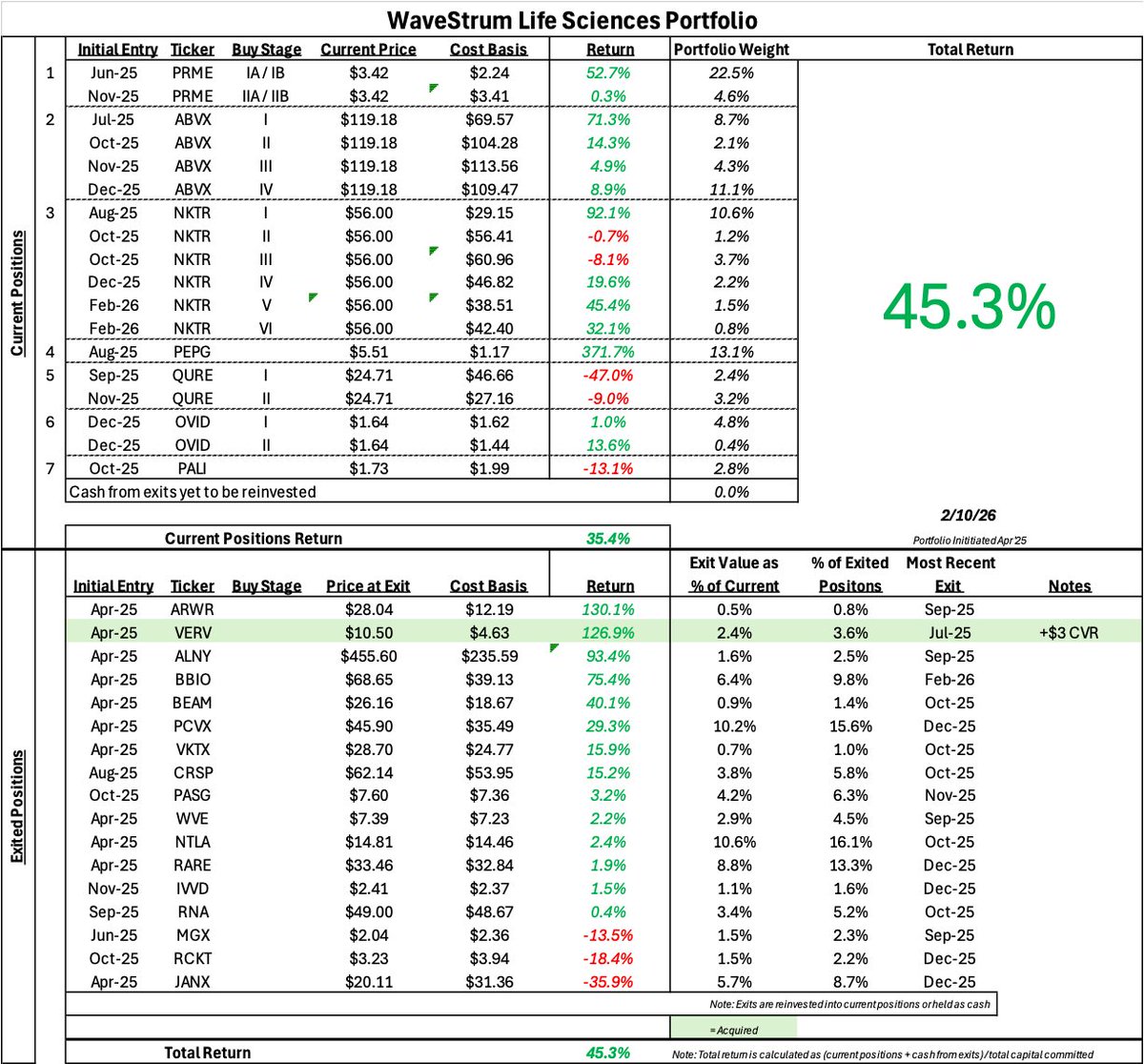

February 10th, 2025 Portfolio Update

Closed out the last small piece of the $BBIO position to allocate towards $NKTR in the pre-market. Though a small upsize (.8% of portfolio), $NKTR is now ~20.0% of the portfolio overall. In many ways, wish I had a bit more capital to allocate. However, I don't want to pull from any of the other positions.

For better of for worse, my strategy has been to try to get a reasonably de-risked exit and a big short to medium-term jump in available capital from an $ABVX acquisition, and then flip that capital into some of my other positions as I feel pretty good about each of them at current pricing.

At the moment, I would basically upsize all my key positions - $NKTR, $QURE, $PEPG, $OVID, $PRME.

$PALI I would probably opt-out of upsizing as there are a few other interesting, though high-risk, names I am tracking.

Near-term Catalysts:

Completed

1. $NKTR Phase 2b Maintenance Data: ✅

Remaining

1. $PEPG Phase 2 5mg / kg MAD Dose Data: Due in Q1 2026

2. $PRME PM359 Approval under the FDA's Plausible Mechanism Pathway: No defined date. However, I believe it will probably happen no later than Q2 2026 if it is going to happen based on the timing of the CNPV voucher awards post announcement of the initiative.

3. $QURE Minutes from Type A Meeting with the FDA: Expect we will receive these in the coming days

4. $ABVX Phase III Maintenance Data: By end of Q2 2026

5. $NKTR Lilly Settlement: Trial to begin this summer

6. $ABVX acquisition: Event / timing unknown

English

InTheTrenches 🙏 retweetledi

Just realized my company turns 15 years old this month. 🤯

Where does the time go. College side hustle trying to make an extra $200/mo ended up becoming the #1 IT company in a major metropolitan area.

Never ended up using the college degree.

English

Took a flyer today on $BCAB @.56

BioValues@BioValues

$BCAB with cash overhang removed/deal out, the story now turns to the huge EpCAM data readout that is forthcoming in q1. $40M market cap, trading at cash value, going into large scale EpCAM readout, things can go crazy here vs. $CTMX $700M market cap.

English

@michaelgmcquaid Nice threads for the young lad. Adding a silver chain & watch, + perhaps a few silver ingots in the pockets would be very apropos.

English

InTheTrenches 🙏 retweetledi

Have a dreamy Sunday...💗

📸 emily_cummings603

#whitemountains #visitnh #artistbluff #cannonmountain #franconianotch

English

@seedy19tron Only concern I see for this particular deal, is talk of annexing Greenland; could cause chills in trade between US and EU. But ABVX is still a great co, so any stall in buyout will only affect options.

English

Update: ICYMI - in an interview yesterday to BFM Bourse a very reputable news source in France, a spokesperson for the Economic Ministry acknowledged the existence of the $abvx “situation” and “verifications” were in progress when questioned about the La Letter piece re $lly interest.

1) For those eagerly awaiting next steps, all you have to do is wait. Remember Marc doesn’t have to sell before maint and CD data, it must’ve been a very good proposal definitely higher than where $abvx is trading now for the situation to get to this stage. And MdG is the 🐐 of selling biotechs so all you have to do is wait

2) $rna with the @FT piece when it first broke , all the dips kept getting bought. Similarly $ptgx still higher from the first @WSJ story. So many more examples. The confirmation from the French govt de risks the M&A trade even more.

3) my read is that $lly are eagerly awaiting the greenlight and they would like to lock it in before JPM ( see $loxo $lly case study). Note that we were told yesterday “Bertrand Dumont's (BPI) team is currently analyzing eligibility before Eli Lilly submits a formal request”. And imo as soon as that greenlight comes , an official bid will come with an announcement immediately after as is usually the case. Literally the last stretch.

Seedy19@seedy19tron

French newspaper with some breaking news this morning $abvx “US Giant Eli Lilly Courts Bercy in Move to Acquire Biotech Firm Abivax A delegation from the pharmaceutical group visited the General Directorate of the Treasury in early December. The meeting was intended to subject a potential takeover of Abivax to an initial test of France's foreign investment screening process.” lalettre.fr/fr/entreprises…

English

@Andre_AGTC @seedy19tron Without knowing his full situation, this may not help him. For instance, some of his shares may qualify for long-term capital gains soon or in a few months.

English

@seedy19tron Here is how it works

Feb $70c is $47 mid point

Breakeven 117 vs yesterday close 115

Selling shares at 115 and paying 47 for the call, you got $68 / share free cash

If BO at say 170, your call is 100 (+53)

The same if you had stock (+55)

At expiration buy back or better rollover

English

The Weekly

New: $pali (2%)

Increased: $nktr (10%) , $ovid (5%)

Unchanged: $abvx (60%) , $slno (20%), $nxtc (1%)

Decreased: $cogt (1%), $ibio (1%)

Closed: $rytm , $celc , $nvo , $tern , $cmps , $ptn , $dawn , $asnd , $nams

The last Weekly of 2025, slightly delayed due to how busy things have been. It’s been a life changing year for me, I will look back on 2025 with fond memories. It’s not been easy, the start was a terrible one with $veru losses and $arvn margin call but stuck at it. This X account has grown 10 fold and my port a few further multiples of that. More than the numbers, I am so grateful for the connections and the people I’ve had the pleasure of meeting and learning from. My life and financial goals I set myself for when I would be 30 were met this year.

There is just something about biotech investing where you can’t just take your eyes off it. The difficulty, the surprises, and drama , get me out of bed every morning. It has taken a toll, the huge swings , the high level of expectations I have from myself to deliver and the stress, thus I have made a decision to take a break for a few weeks so I could go explore and travel a little. Starting with Brazil and Uruguay next week. As a result of this decision, I harvested some losses and left only have my highest conviction plays in my port until I can be on my desk fulltime to do justice those who follow me and my portfolio.

Focusing on the commentary, let’s start with $abvx , look the more I see , the more I am convinced that the potential is so great. Abstracts seem like negotiating leverage on the CD multiple which is good. Anti-fibrotic efficacy = holy grail in IBD. If this hits, it’s a Top 5 I&I asset, period. Every other mechanism (JAKs, S1Ps, IL23s) works across indications. Only Entyvio is gut-restricted. so wonder what other indications Obe can be tried in? Including reviving RA.

Even if you take a 1x multiple of peak sales on Crohn’s and we are talking a mid-$200s deal. You see 840k pts x 15% share x $35k price = $4.1B for UC alone , Risk adjusted 85% still $3.75B

Then Crohns 660k pts x 10% share x $35k price = $2.3B , 45% risk adjusted gives you $1B

~$5B conservative numbers 4x Peak Sales (Standard for de-risked late-stage I&I assets) you get a $20b deal price assuming it’s not a super competitive process which would even push the valuation higher.

$slno , the piece that we’ve been working on that will help you understand why it’s so undervalued here is nearly ready. Will share with you soon.

Next up, I’ve been super quiet on $nktr , and whilst I added, it’s important for you all the understand that with $nktr you’ve got a promotional management team with a graveyard of failures until recently. The lack the specialist funds guiding them and TCGx exiting doesn’t help. Settlement isn’t a catalyst I would want to hold the stock as it’s a lottery ticket.

The other problem is we got the AA data. It was good. It should’ve gotten us paid. It didn’t, and it’s been a theme with this name, but I do think eventually folk will come around but if you take the lawsuit off the table, you are staring down the barrel of an execution slog on two massive Phase 3 programs. They need to raise a boatload of cash to cross the finish line. M&A? Unlikely given the baggage although would make sense for all parties.

I don’t love the setup. This could be dead money unless you’re willing to underwrite a 3-year horizon and eat the dilution.

But let’s not forget Rezpeg is actually a real drug. Solid in 2nd-line AD and a legitimate shot in AA as a safer post-JAK alternative.

I added $pali again, most of the buying on Friday was me as I think in the 1s irrespective of $abvx it is undervalued.

$ovid I was so happy to see Affinity and RA filings, think $1.3 is the floor here and upside still multifold with another catalyst albeit not huge in Q1.

1/2

English

Quite a move for $JSPR early Q1 data. Might just be tax loss selling is over

Not Warren Buffett@YieldCurveBalI

$JSPR Excellent analysis that accurately describes JSPR's current reality. So if you want to update your JSPR understanding or learn about JSPR for the first time, this is a must read. beyondspx.com/quote/JSPR/ana…

English

@Biohazard3737 I think she meant to buy “Bambi: The Reckoning”

English

@michaelgmcquaid If only all stocks would trade like this, we’d all be in the land of milk and honey:

English

$IFRX insights

3in5saved@3in5saved

$IFRX Here’s my favorite slide from today’s presentation (available here inflarx.de/Home/Investors…). People can jump and down all they want about open label vs placebo controlled, but in the brilliance of HiSCR, which only cares about reduction of lesions that spontaneously heal (nodules and abscesses) and considers draining tunnel reduction to be irrelevant, no wonder placebo response is so high with this efficacy measure. In fact, there’s so much fluctuation in HS placebo response that one has to wonder about drug efficacy even if it hits favorable HiSCR territory. Therefore best to look at the highest QoL HS lesion impact, draining tunnels, which do not come and go on their own and therefore a low placebo response is to be expected. Neutrophil hyperactivity is the cause of tunnels, the effector cells of HS which originate in the bloodstream, primarily dependent on C5a-C5aR1 signaling to move to tunnels to begin with. So says decades of independent research that’s documented in over 6000 publications about this vital axis of inflammatory disease.

English

@Quick2smile Exchange rate of CNY to US Dollar is about .14.

Market cap of Staidson is ~$2.5B in US dollars.

English

@medstudentinvst @StreetCred2017 @3in5saved Last one tonight (safety); review this @3in5saved post (the post it is replying to has good overview/safety):

x.com/3in5saved/stat…

3in5saved@3in5saved

Endpoints on the INF904 HS/CSU p2a study are important to note.

Primary: Frequency, severity, and relatedness of treatment-emergent adverse events (TEAEs) and serious adverse events (SAEs) using MedDRA classification.

Secondary:

English

@StreetCred2017 @InTheTrenches2 @3in5saved Thanks Street, will dive in this week / weekend

Appreciate you sharing

English

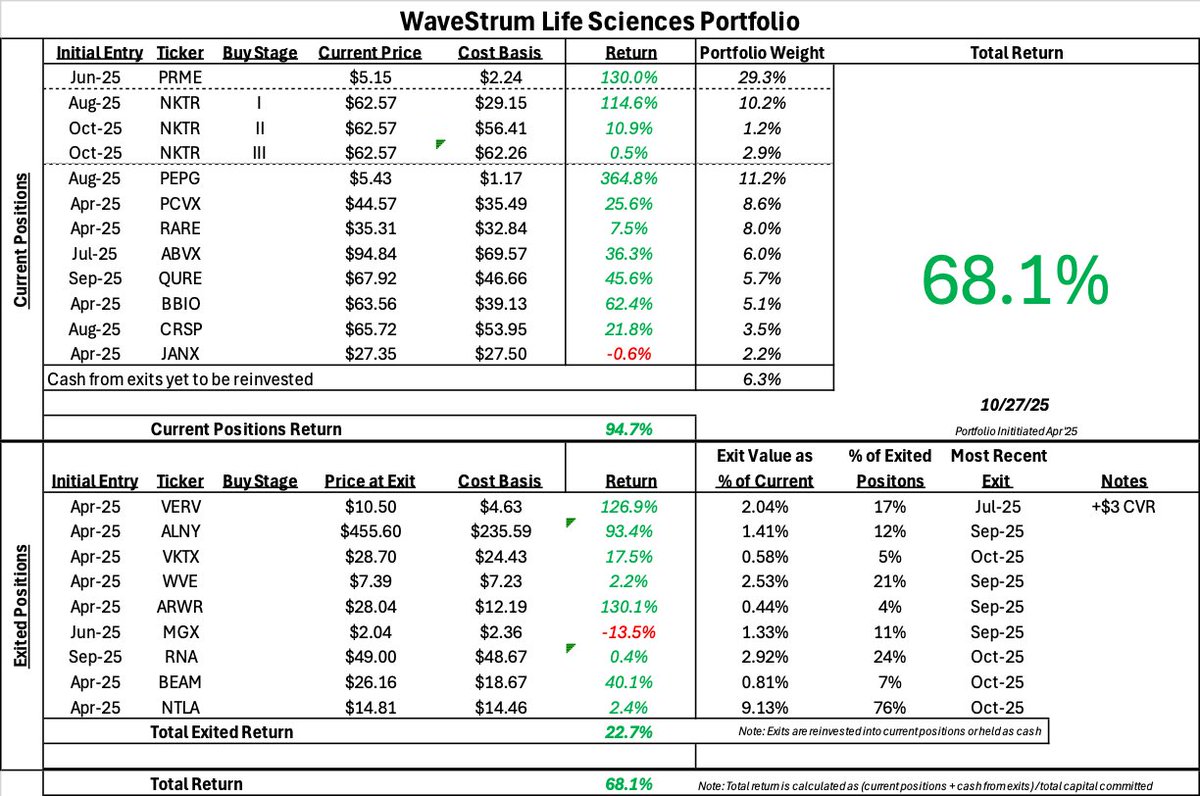

October 27th, 2025 Daily Update

I posted my thoughts on the disappointing $NTLA news, my original thesis, why that thesis changed post safety event, and a hypothesis for what happened mechanistically earlier today. That is a more complete breakdown. However, at the portfolio level wrt $NTLA, today was a good example of entry price playing an important role in the risk-reward profile of an investment. Despite a potential program threatening safety event, was able to close the position with a 2.2% gain and the portfolio as a whole was only down about 5% from Friday. Believe upside was worth such a downside risk

$BBIO up on the LGMD 2I / R9 data

$PEPG up to old levels on the $RNA buyout news, though we will see how durable this is. If $PEPG delivers strong functional data at the 10mg / kg and 15mg / kg doses (5mg / kg would be a bonus) to align with the unprecedented splicing improvements, I will continue to upsize this position and will likely lean pretty heavy on the weighting. The $RNA buyout shows what is possible with this company.

$QURE up as well.

$RARE continues to move up. Again, think this presents a highly compelling risk-reward opportunity at the entry price. Though if price continues to progress, the risk-reward for new entries will shift as it did for $NTLA.

I bought more $NKTR with some of the $NTLA proceeds.

I am in the market for biotech companies to deploy capital towards with the $NTLA proceeds. Particularly interested in companies with a $PEPG - esque profile.

- Bad history and negative events amongst therapies in pipeline has depressed stock and kept it somewhat depressed through the latest biotech run

- Nevertheless, an asset in pipeline has legitimate chance of best in class efficacy based on pre-clinical / early clinical data

Oncology companies have a high bar for me. Interested in neuro, but nothing that is alpha-synuclein or beta-amyloid targeted. Nothing psychiatry, except maybe addiction or PTSD.

Lastly, when I began my biotech portfolio in April 2025 (took me through August to be fully invested), I had a very small single stock position in $NTLA (<1% of portfolio) from October 2024 which I rolled into the portfolio. For presentation simplicity, now that I am exited from $NTLA, I have marked on my excel output April 2025 as my initial entry date without the rollover notes (virtually all of $NTLA position was built after April 2025). If anyone thinks that's not correct or unfair, feel free to chime in.

As one can see with $NKTR, I have also started to mark buy stages for each position in the portfolio, rather than just having one position marked with the total dollar cost average as I have done for most of my portfolio to date. Found myself really not liking to bring the overall DCA up lol, but believe it makes sense to invest in a strong company on the way up, so solved for it that way.

Easier to track the performance of each individual decision too

English