KaneCap

35.4K posts

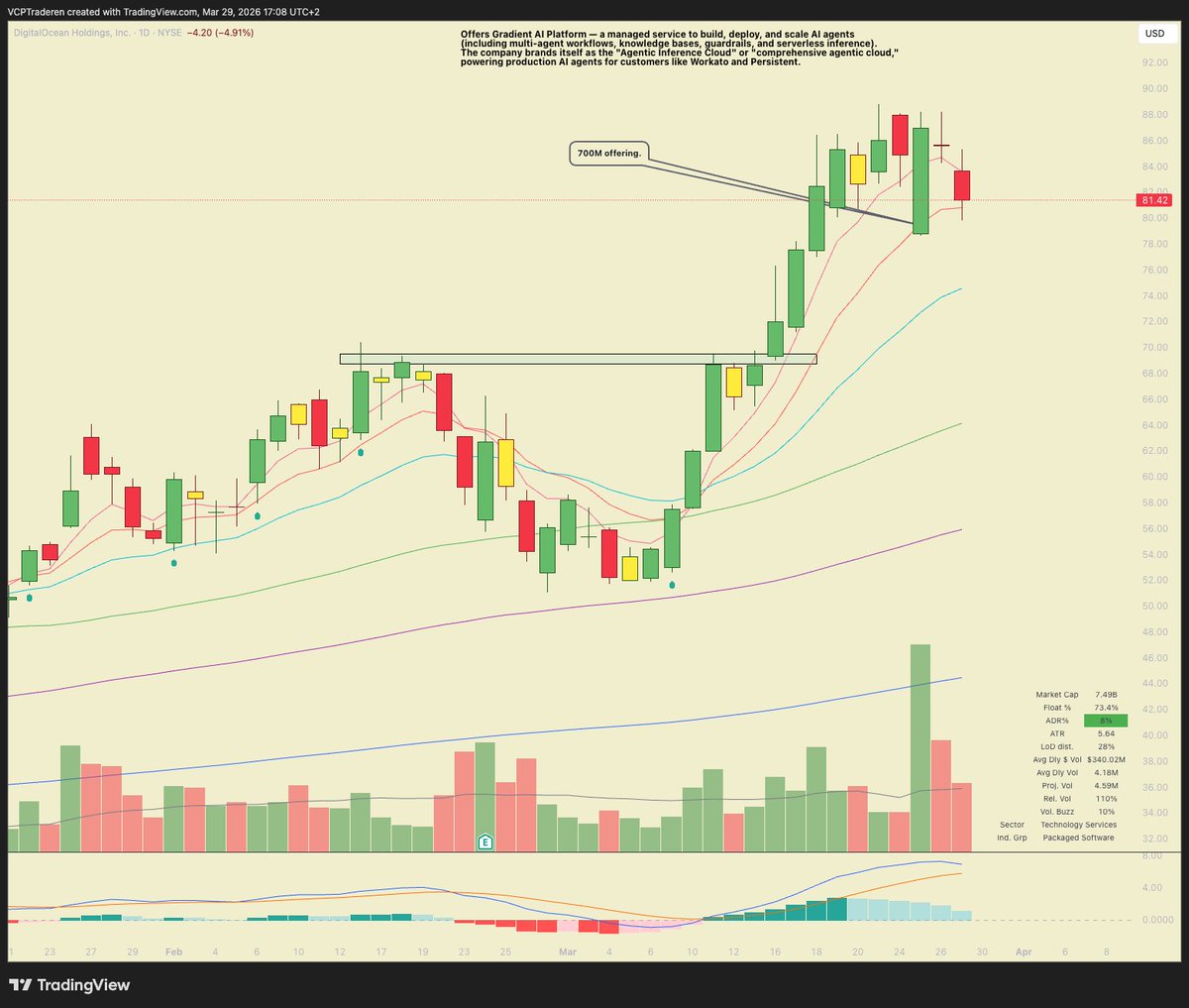

If the market gaps down tomorrow I will be looking for undercut and reclaims of key levels in the leaders. $SATL and $DOCN are my favorites. $SATL would be a five star short pivot in a good market environment.

English

KaneCap retweetledi

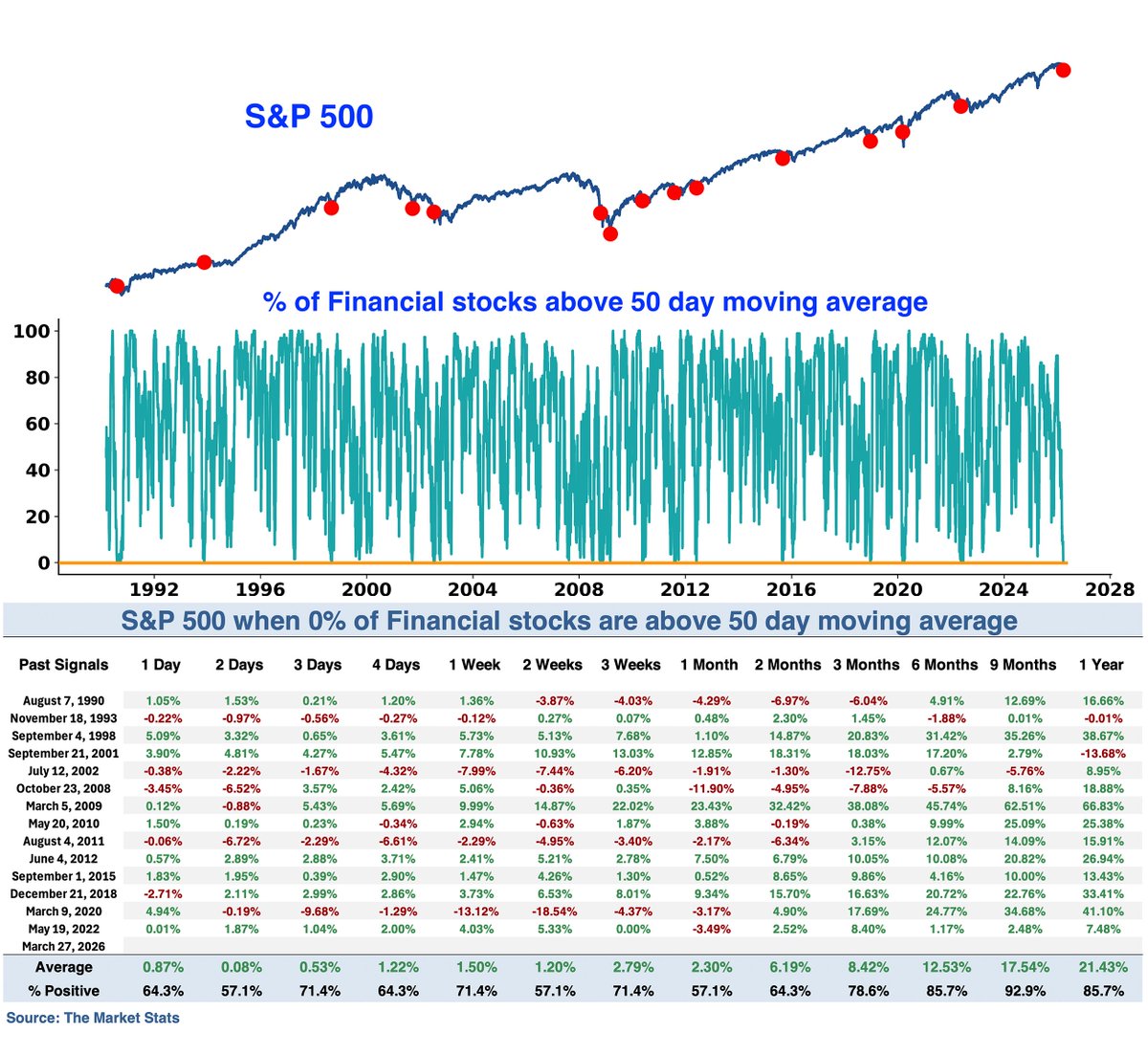

0% of $SPX Financial stocks are above their 50 day moving average

In the short term, S&P 500 forward returns were mixed

But 9 months later saw $SPX higher 13 of 14 times with an average gain of 17.5%

English

Out of curiosity, I calculated the TWIF Index's performance in 2022. At its lowest point, it was down 34% (June 2022). This year, the TWIF Index is already down 29%, and we're only in March.

Jevgenijs Kazanins@jevgenijs

My goal with the TWIFT Index was to create a super simple index that helps track how public fintech companies are performing. It consists of just 15 stocks and is price-weighted. The TWIFT Index is doing its job: it captured the strong run fintech had in 2024, showed the stress early in 2025, and clearly shows how ugly 2026 is shaping up so far.

English

Chinese girls went from 6 cm shorter to taller than American girls in one generation. Nutrition policy or genetics?

English

@RepThomasMassie @tztokchad This vision is not compatible with open borders brother

English

Imagine a world where hard work is rewarded, truth and justice prevail in courtrooms, the government doesn’t steal your labor by debasing the currency, bureaucrats aren’t captured by corporations, and our taxes go toward critical infrastructure instead of wars overseas.

English

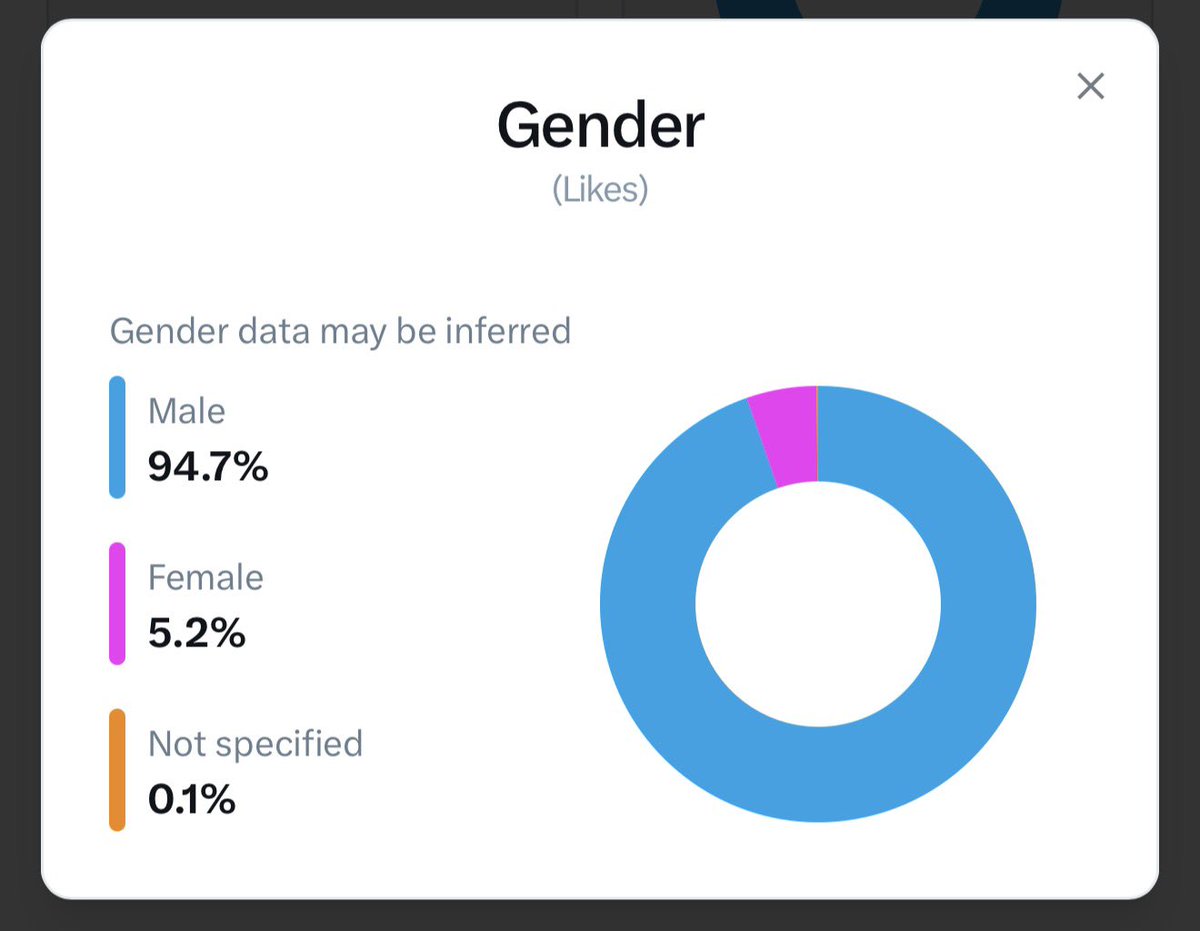

Why is it that very few females are interested in investing?

English

How old were you when you learned the USA hasn’t been the good guy for a very long time

Chris Martenson@chrismartenson

We're not the good guys...

English

Santiago R Santos@santiagoroel

I started looking at Western Union because I thought stablecoins would kill it. Then I realized WU is better positioned than almost anyone to leverage them. Brand, distribution, 200+ countries, $923M in EBITDA. The key risk was management. They had been skeptical of stablecoins. I placed the bet in November. Since then WU has not only outperformed Solana but the broader market: WU +2.14% / SPX -6.76% / Nasdaq -11.66% / SOL -56.15% WU is a $2.8B market cap business trading at 6x earnings with a 10% dividend yield. Remitly trades at 50x on a 2.3% operating margin. Wise at 23x. The discount exists because WU revenue is declining 3.8% while both are growing 25%+. I am not fighting that. But at 6x earnings you are paying for zero recovery, zero tech adoption, zero optionality. That is the margin of safety. I was at the @blockworksDAS this week. The WU CEO was on the same stage. Very different energy from the one I had been following. Clear on the stablecoin strategy, talking about flipping negative float into positive float. They have since announced USDPT, their own stablecoin on Solana. For a 175-year-old company to go from skepticism to launching on Solana in under a year is a meaningful shift. Of course, there is plenty of execution risk. The bear case was always that they would not act. They are acting - and that alone warrants a repricing. The math I ran back in November when I placed the bet was: lose ~20-30%, cushioned by $500M in net income and a 10% dividend. Re-rate to Wise multiples and it is 4 to 5x. I am not betting on convergence. I am betting the market prices zero probability of it, and I will get paid for getting a free option. WU is part of a broader thesis that led me to start @inversion_cap: acquiring businesses with distribution at attractive prices. There is a lot of embedded optionality in those businesses. Not all will act in time. Some will die. But the ones that do will meaningfully outperform, and those gains will more than outweigh the losses. You reduce that risk meaningfully when you control that business. The greatest beneficiaries of cost-reducing technology like AI and crypto are not the startups building it. They are the incumbents with distribution that adopt it. WU is one of many. Full piece on Substack: open.substack.com/pub/obviously/… @HadickM double or nothing? Market settles November 1, 2026. DISCL: Long WU. Long SOL. NFA.

ZXX

KaneCap retweetledi

They don’t even mock me for bearposting w/ Hindenburg Omens anymore

They just look at me like this

Mandelbrot@Wild_Randomness

Can’t stop, won’t stop

English

Celebrating 23 years as an independent professional trader. Splurged for bbg 3.5 yrs in. Yes i’m old, but still got that dog in me.

English

@StonkChris Think they had the first part right but like you said it's the US economy. It's coming back, even if it drops a lot.

English

@aleabitoreddit @BitcoinAIGuy It’s a red flag they announced the atm with no deal imo

English

If $PL, the $11B company filed for a $6,000,000,000 dilution, I'm pretty sure everyone would leave their positions.

The reason why $IREN filed for a $6B ATM is because the cult "diamond hands", "buy the dip" community are happy to tank the dilution as long as the company succeeds over their equity appreciating.

English

My thoughts on $NBIS, $IREN, $CRWV and the current Neocloud market.

One of them ends up as the next AWS in 5 years:

My guess it’s Nebius.

It's not winner takes all (DigitalOcean is there with Amazon), but there's clearly superior structures and likely winners.

The downside:

-> Low chance of rate cuts from Iran conflict.

->Broader market doesn't appear to want to fund the CapEx cycle. But want to reap the benefits

With $IREN:

We get it, 4.5GW = X revenue. But who is funding the GPUs?

Whoever is buying into the $6,000,000,000 ATM right now.

The winners will be whoever enters after holders get fully diluted.

The reality is, they don't have enough funding to monetize their capacity through GPUs without colo models.

And they didn't find other financing methods, so they went through ATMs because of a cult community that will buy into anything they sell.

However, I agree it will be accretive long term. Just not as much for the retail buying in now.

With $CRWV:

They did everything right... $NVDA backing. Hyperscaler clients...

But they financed completely wrong. Now, $1.5B+ yearly debt interest is eating Coreweave alive and cuts into FCF.

Almost like credit card debt, Coreweave gets a job to pay off that debt, but eventually, the debt interest is too high that working doesn't really cover that and expansion too.

If any company goes down, $CRWV is the first to go the massive debt load and interest.

With $NBIS:

They're doing as much as they can right... $NVDA funding $2B to fund capex.

Convertible note offerings (convertible note short hedging is annoying for short term price appreciation).

But this is the best way to do financing structures with much lower interest than Coreweave.

They now have ~$46B+ in backlog from $META and $MSFT, two of the most profitable hyperscalers out there, without direct OpenAI linked contagion like Coreweave.

And unlike others; there’s appreciation from their other companies (Clickhouse equity appreciation: avride robotaxi scale up; toloka triple digit growth)

From my take: Nebius is the clear winner.

However, current macro environments does not favor short term holders across the board with indexes dropping 7%.

Especially so if they're buying into active ATMs.

Long term, the benefits when they scale up eg. $NBIS Q4 2026 (yes, even $IREN), will be immense.

English

$SMH Biggest two day decline since April 3/4, 2025.

TSDR Trading@TSDR_Trading

I shorted $SMH Let the bull market begin!

English

This is what everyone in their 20s and 30s has dreamed about.

Brew Markets@brewmarkets

The S&P 500 is on track for its worst month since 2022.

English

English

@OrsonPratt65 @JoshuaSteinman A whole lot of us Californians are aware that our ancestors lucked into this paradise on Earth and that if we rewrote the zoning codes to allow everybody on Earth a fair chance to live here, we'd soon be living in Paraguay or Belarus or Inner Mongolia or Chad where we belong.

English

Here’s the thing: if California had even somewhat competent leadership, every smart, high agency person in America would live here within 12 months.

Mitt@MittCPA

the california propaganda will continue

English

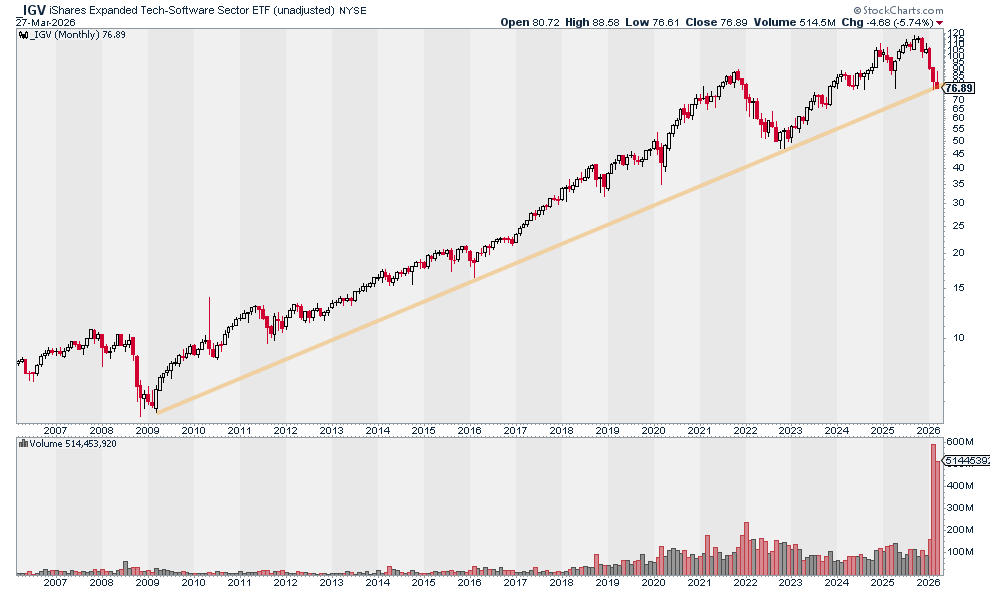

Software got major issues

$IGV breaking uptrend that's been in place in 2009 on volume👀

English

- I talk about my 700% gains on $PLTR

- you say I can't just pick one random outlier example

- you then pick $LMND entirely at random to "call me out on"

- I show you that I locked in 500% realized gains in addition to my long term bag which is deep green

- you continue to act like you know better

- but what you don't do is show proof of remotely comparable gains

- because all you have is talk

- always the case. sad man. clowns on here always give themselves away. how pathetic to try and call out strangers on the internet to make yourself feel better 🤦♂️

English